Stocks’ Details

Woolworths Group Limited

FIRB approval of Woolworths Petrol Sales: Woolworths Group Limited (ASX: WOW) had recently announced that EG has received confirmation from the Foreign Investment Review Board (FIRB) that the Commonwealth has no objection to EG acquiring Woolworths Group’s 540 fuel convenience sites.This was the only condition which was necessary for the transaction to take place. Hence, now the transaction is expected to complete in early April 2019. Management intends to return up to $1.7bn of capital to the shareholders.

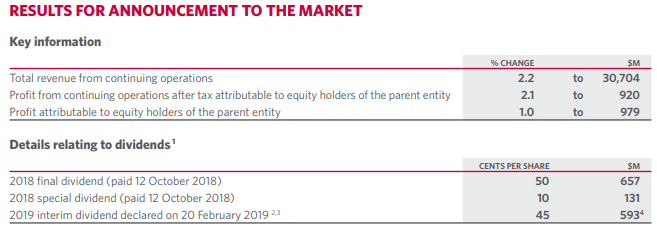

Key Information (Source: Company Reports)

For 1H FY19, the company’s revenue from continuing operations grew by 2.20% and stood at $ 30,704 Mn. This growth was witnessed predominantly on the back of improved sales momentum in Australian Food in Q2’19 compared to Q1’19.However, this was offset with a more subdued demand in November and December.

What to Expect From WOW: As regards the outlook, the management expects the Australian food markets to remain challenging including ongoing input cost pressure.The New Zealand Food division remain focused on building on the new brand platform, improving our fresh and affordable Health offer, innovating the digital experience for customers and realising the financial benefits of these investments.

Regarding the Endeavour Drinks, the management has strong plans in place to ramp-up digital, deliver more localised ranges, better service and greater convenience for customers

On the financial metrics front, the company is maintaining a robust EBITDA margins @6.7% which is higher than the industry median of 6.3%.

Thus, considering above parameters and current trading level, we maintain our “Hold” recommendation on the stock at the current market price of A$30.230 per share (up 0.066% on 14 March 19).

Coles Group Limited

A Look at Coles’ Strength: Coles Group Limited (ASX: COL) had earlier made an announcement that director of the company named Mr. James Philip Graham has sold 800 shares via off-market transfer at a price of $11.42 per share as at 8 March 2019. Hence, post this development, the shares held by Mr Graham stood at 460,188 shares.

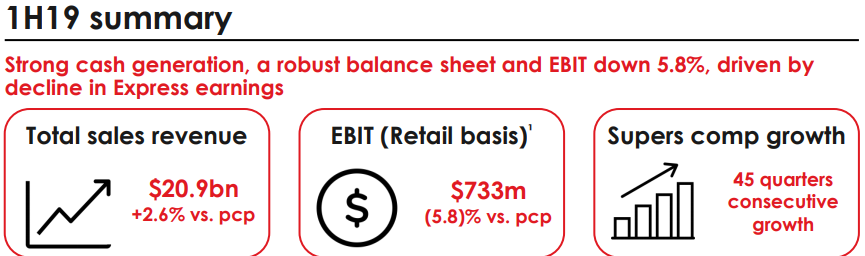

As per the results for the 1H FY 2019, the total sales revenue grew by 2.6% on the pcp to come in at $20.9billion. This modest growth was witnessed on the back of higher revenue garnered from supermarket sales. However, the EBIT (Retail basis) came in at $733 Mn a fall of 5.8% on pcp. EBIT fell on the back of a decline witnessed in the Coles Express earnings.

1H19 Financial Highlights (Source: Company Reports)

What to Expect From COL: As regards the outlook for 2H FY 19, the company’s management is committed to making life easier for customers with an increasing focus on convenience.The cost headwinds from the new store EBA, energy & drought impacts on input costs are expected to continue. The management expects to pay its first dividend in September 2019, which will be a final dividend for the year ending 30 June 2019, reflecting seven months of earnings post demerger. Moving forward, the company will be facing challenging times due to intense competition prevailing in the Australian retail sector.The stock of the company has fallen by 7.18% in the past one month.

Hence, due to the above stated factors, we maintain our watch stance on the stock at the current market price of $11.250 per share (down 1.142% on 14 March 2019).

Myer Holdings Limited

Enhancing the Portfolio: Myer Holdings Limited (ASX: MYR) has lately disclosed the results for the half year ended 26 January 2019. As per the same, the total sales from ordinary activities came in at $1,671.4 million, down 2.8% on pcp. The NPAT came in at $41.3 Mn, up 3.1% on pcp. This was on the back of Improved operating gross profit margin and continued disciplined cost management which had the impact of offsetting the higher depreciation and interest expenses.

1H19 Financial Highlights (Source: Company Reports)

What to Expect From MYR: As regards the outlook for 2H 2019, the business will continue to focus on the execution of its Customer First Plan including an ongoing focus on costs, profitability and cash management. The company will continue its investment in two key areas Merchandise to establish the new brands and Online business in order to further improve both the customer experience and the efficiency.

Also, the company has a robust dividend yield of 13.70%, which is much higher than the peer median of 8.60% which highlights that the company has been focusing towards generating returns to the shareholders.

Hence considering certain performance related improvements and decent outlook while the dividend yield looks a bit high, we maintain our “Hold” recommendation on the stock at the current market price of A$0.560 per share (up 7.692% on 14 March 2019).

Metcash limited

Decent Guidance: Metcash Limited (ASX: MTS) has disclosed that one of its substantial holders, Pendal Group limited (PDL) has cut down its stake in the company from an earlier 12.94% which comprised of 117,633,773 votes to 104,710,736 votes, which ultimately resulted into 11.52%.

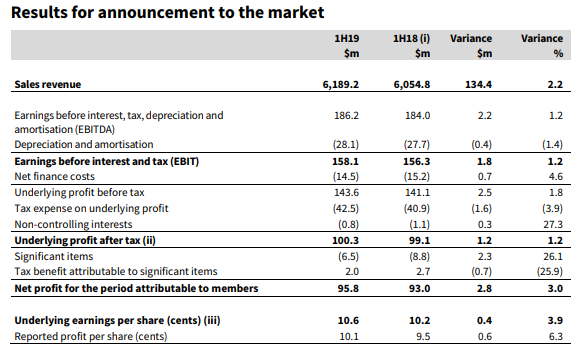

MTS’s 1H19 Financial Highlights (Source: Company Reports)

As per its 2019 half year results for the period ended 31 October 2018, the group sales rose by 2.20% & came in at ~$6.2 billion. This marginal growth was witnessed on account of the sales expansion seen across all the pillars of the business offset by the subdued performance in the supermarkets pillar due to challenging retail business environment. The Underlying profit after tax was up 1.2% to $100.3m.

What to Expect From MTS: Going forth, the company expects their food business to witness the highly challenging environment for the rest of the year. The company expects 2H FY 2019 EBIT to be impacted by approximately $8 million of incremental investment by Supermarkets business in growth opportunities. This deployment might deliver earnings benefits beyond FY19. Meanwhile, the stock price has fallen by 4.06% in the past six months and is trading close to 52-week lower level, posing an attractive opportunity for accumulation at the current juncture. Thus, considering the decent outlook, respectable annual dividend yield of 5.19%, we have a “Buy” recommendation on the stock at the current market price of $2.650 per share (up 1.923% on 14 March 2019).

.PNG)

Stock Price Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...