.png)

Stocks’ Details

Kogan.com Limited

Acquisition of Matt Blatt: Kogan.com Limited (ASX: KGN) operates a portfolio of retail and services business. The market capitalisation of the company stood at $810.52 Mn as on 15th May 2020. Recently, the company announced that it has acquired Australia’s premier furniture and homewares retailers “Matt Blatt” at the consideration of $4.4 million. The company stated that the acquisition has been financed from its from cash reserves. This acquisition will help the company in expanding its reach in the furniture and homewares market. During April 2020, the gross sales of the company witnessed a rise of over 100% against April 2019 and gross profit for the month went up by over 150%.

.png)

Financial Performance (Source: Company Reports)

Future Aspects: Kogan continues to make investments in building its brand and growing Active Customers. The company is likely to work on the development and improvement of Kogan Marketplace.

Valuation Methodology:Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company reported active customers to 1,948,000 as at 30 April 2020, with an incremental 139,000 Active Customers in the month of April 2020. Gross margin and EBITDA margin of KGN stood at 22.7% and 8.1% in 1H FY20, reflecting YoY growth of 3.2% and 2.3%, respectively. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers like Temple & Webster Group Ltd (ASX: TPW), GUD Holdings Ltd (ASX: GUD) and Myer Holdings Ltd (ASX: MYR). Hence, considering growth in active customer base, improvement in key margins and acquisition of Matt Blatt, we give a “Hold” recommendation on the stock at the current market price of $8.760 per share, up by 2.456% on 15th May 2020.

Treasury Wine Estates Limited

Demerger of Penfolds Business: Treasury Wine Estates Limited (ASX: TWE) is an international wine business having a portfolio of luxury, premium and commercial wines. The market capitalisation of the company stood at $7.01 Bn as on 15th May 2020. The company has recently appointed Stuart Boxer to the newly created role of Chief Strategy and Corporate Development Officer. Mr Boxer possesses strong financial, strategy and M&A expertise. In another update, the company announced that it is planning to demerge its Penfolds business and associated assets into a separate ASX-listed company by the end of the CY21. This demerger would improve TWE’s and Penfolds’ ability to pursue their own strategic priorities and deliver a stronger long-term growth profile. During 1H FY20, the company reported a rise of 2% in net sales revenue to $1,536.1 million; this was fueled by improvement in NSR per case as the company continues its journey of premiumisation in all regions.

.png)

Revenue by Region (Source: Company Reports)

Suspension of Previous Guidance: Due to disruptions in the operating markets, the company no longer believes that it will achieve its FY20 EBITS growth guidance of 5% - 10%. TWE would continue to work on premiumisation strategy. It is planning to take several initiatives to decrease the size and scale of its Commercial wine business, mainly in the United States.

Valuation Methodology: P/BV Multiple Based Relative Valuation (Illustrative)

.png)

P/BV Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of TWE is inclined towards its 52-week low levels of $8.400, proffering decent opportunity to accumulate. During 1HFY20, the company declared fully franked interim dividend amounting to 20.0 cps, reflecting growth of 11% over 1H FY19, and a pay-out ratio of 62.7%.We have valued the stock using Price to Book Value multiple based illustrative relative valuation method, and for the purpose, we have taken peers such as Coca-Cola Amatil Ltd (ASX: CCL), United Malt Group Ltd (ASX: UMG), and Metcash Ltd (ASX: MTS). As a result, we have arrived at a target with an upside of lower double-digit (in percentage terms). Thus, considering the growth in dividend, current trading levels and valuation, we give a “Buy” recommendation on the stock at the current market price of $9.820 per share, up by 1.029% on 15th May 2020.

BWX Limited

Steps to Increase Working Capital Facilities: BWX Limited (ASX: BWX) is a vertically integrated beauty and personal care production and distribution company. The market capitalisation of the company stood at $433.63 Mn as on 15th May 2020. The company has undertaken steps in order to increase its working capital facilities to further support the business as well as a rephasing of activity to keep tight control on costs. BWX has placed additional resources for new product development in natural, efficacious hand sanitiser to further benefit and support its retail partners and Australian consumers during an unprecedented time.

The company has recorded growth of 23% net revenue to $84.1 million due to strong sales momentum spread in the engine markets of Australia, North America, and International markets.

.png)

Net Revenue (Source: Company Reports)

Expected Revenue and EBITDA Growth: The company would continue to make investments in brand building, process improvement, capability, and innovation. This would assist BWX to generate deeper consumer penetration and basket size to support 20-25% revenue and 25-35% EBITDA growth for the full year FY20.

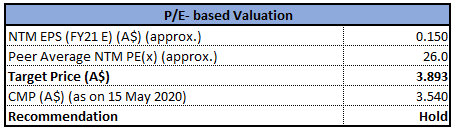

Valuation Methodology:Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company closed the half-year with a strong balance sheet and healthy cash position. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers like Lovisa Holdings Ltd (ASX: LOV), Johns Lyng Group Ltd (ASX: JLG), Asaleo Care Ltd (ASX: AHY) etc. Hence, considering the strong balance sheet and healthy cash position, expected revenue and EBITDA growth and steps to increase working capital facilities, we give a “Hold” recommendation on the stock at the current market price of $3.540 per share, up by 1.433% on 15th May 2020.

Metcash Limited

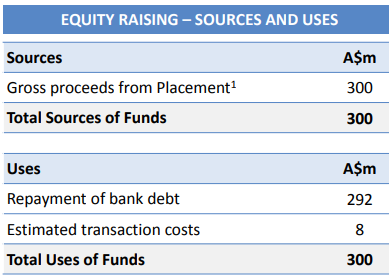

Capital Raising to Improve Liquidity: Metcash Limited (ASX: MTS) is a wholesaler to independent retailer in food, grocery, liquor, hardware, and automotive industries. The market capitalisation of the company stood at $2.39 Bn as on 15th May 2020. MTS has recently opened its share purchase plan for an eligible shareholder to raise up to A$30 million. The SPP follows the completion of fully underwritten institutional placement for A$300 million. MTS experienced significant demand from existing shareholders and another institutional investor in the institutional placement. The company would use the proceeds to cement its balance sheet and improve liquidity.

Use of Funds (Source: Company Reports)

Impact on Sales: The company stated that the trade sales for FY21 are likely to be impacted by a slowdown in construction activity. MTS continues to have a strong focus on costs in order to offset the impact of any reduction in sales volumes.

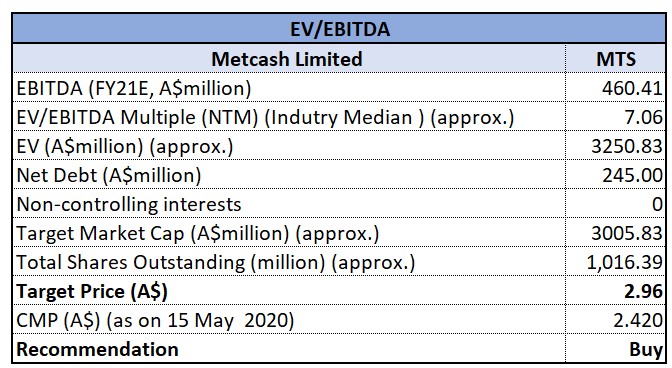

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The recent capital raising places the business to capitalise on potential opportunities which align with its strategic direction. Over the span of the five-year (2015-2019), the company has maintained positive free cash flow, which implies that it is effectively managing its working capital. We have valued the stock using EV to EBITDA based relative valuation approachand arrived at a target price with an upside of lower double-digit (in percentage terms). Thus, in light of effective use of working capital and recent capital raising, we give a “Buy” recommendation on the stock at the current market price of $2.420 per share, up by 2.979% on 15th May 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...