.png)

Stocks’ Details

Nufarm Limited

H1FY19 NPAT Declined by 9%:Nufarm Limited (ASX: NUF) is involved in the manufacturing and sale of crop protection products with operations in Australasia, Africa, the Americas and Europe regions. Recently, Schroder Investment Management Australia Limited, became a substantial holder of the company with a stake of 5.25%, effective from December 27, 2019.

In another update, the company informed the market that it has identified additional sales rebate claims from customers that relate to Nufarm’s FY2019, while reconciling accounts with German customers for the CY2019. Following the completion of investigation and negotiation with customers, impact on EBITDA has been estimated at ~A$9 million. The company also stated that trading conditions have been difficult for FY20 to date, which resulted in lower earnings in all regions for the first quarter compared to the prior year. This can be attributed to high channel inventories and substantially lower demand in North America resulting in first quarter EBITDA of ~A$20 million below the corresponding period for this region. With this, the company expects first half EBITDA to be lower than prior year. Additionally, completion of the proposed sale of the South American business, is expected to occur in the second half of FY20, subject to shareholder approval on 5 December 2019.

.png)

Key Financial Metrics for FY19 (Source: Company Reports)

FY19 Key Financial Highlights for the period ended July 31, 2019:Revenue for the period increased by 14% to $3,758 million with growth in all regions except Australia and New Zealand. Underlying EBITDA for the period increased by 9% to $420 million, driven by a full-year contribution from the European portfolio acquisitions and growth in the North America, Seed Technologies and Asia business segments. Underlying net profit after tax decreased by 9% primarily due to the impact of a full year of depreciation and amortisation relating to the acquired European portfolios.

Stock Recommendation:NUF’s share generated a positive six months return of 45.59%. Considering the company’s FY19 financial performance, profitability margins, weak business environment, etc., we have a watch stance on the stock at the current market price of $5.810, down 2.189% on December 30, 2019.

Altium Limited

FY19 Subscriber Base Improved by 13%:Altium Limited (ASX: ALU) is engaged in the development and sales of computer software for the design of electronic products. Recently, the company concluded its annual general meeting where the management the shareholders stating that the company has delivered industry-leading results, both in technology and engineering as well as in financial returns for shareholders.

FY19 Key Highlights for the period ended June 30, 2019:Outstanding revenue growth across all business units and all key regions, improved by 23% to US$171.8 million. Subscription base grew by 13% to more than 43,600. Revenue from the Chinese market improved by 37%, and the US and EMEA delivered revenue growth of 14% and 20%, respectively. Board and Systems revenue grew by 17% to US$126.8 million. Operating cash flow increased by 42% to US$69.1 million. The Board of Directors declared a final dividend of AUD 18 cents per share, with record date and payment dates on 4 September 2019 and 25 September 2019, respectively.

.png)

FY19 Key Financial Metrics (Source: Company Reports)

What to Expect: The company is focusing on becoming the dominant provider of PCB design software by scaling up the transactional sales capacity and expanding the market reach in all geographies, and by driving adoption of its new cloud platform Altium 365. Altium Limited has also committed to achieve revenue of $500 million by 2025 with 100,000 subscribers.

The company expects to exceed the set long-term strategic revenue targets of US$200 million for the FY20 and also anticipates it to be in the range of US$205 million to US$215 million. The company expects EBITDA margin to be between 37% to 38%. Altium Limited anticipates to reach its halfway mark of 50,000 subscribers as early as 2020.

Stock Recommendation:The stock generated a positive YTD return of 66.27% and is currently trading close to its 52-week high of $38.490. The company delivered outstanding performance for FY19 and aims to continue the momentum across all its key regions and business segments by investing on accelerating future growth. Moreover, it is focusing on many initiatives with an aim to achieve its revenue targets by 2025. Considering the above-mentioned facts and current trading levels, we have a watch stance on the stock at the current market price of $36.140, up 0.584% on December 30, 2019 and suggest investors to wait for the better entry level.

Appen Limited

Revenue from Speech and Image Improved by 85% on PCP:Appen Limited (ASX: APX) is engaged in the provision of quality data solutions and services for machine learning and artificial intelligence applications for global technology companies, auto manufacturers and government agencies. On December 23, 2019, the company informed the market that it will release its earnings information for FY19 on 25 February 2020.

H1FY19 Key Financial Highlights for the period ended June 30, 2019: The company reported strong core performance with Speech and Image revenue increasing at a rate of 85% on pcp. Overall revenue of the business went up by 60% to $245.1 million. Underlying NPAT for the period improved by 67% to $29.6 Mn.

.png)

H1FY19 Key Metrics (Source: Company Reports)

Valuation Methodologies:

Method 1:Price to Earnings (PE) Multiple Approach

.png)

Price to Earnings (PE) Multiple Approach (Source: Thomson Reuters)

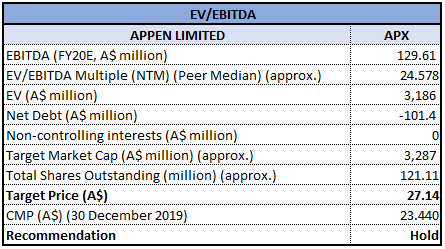

Method 2:EV/EBITDA Multiple Approach

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

What to expect:Underlying EBITDA for the FY19 has been estimated in the range of $96 million - $99 million, at an exchange rate of A$1 = US$0.74 for performance in November and December. At the current translation levels, underlying EBITDA is expected to be $1.0 million - $1.5 million more than the above specified range. The above forecast replaces the previous guidance range of $85 million - $90 million. The improvement in earnings guidance came in as a result of increase in monthly relevance revenues and margins, mainly from existing projects with existing customers. FY19 ARR is expected to be in the range of $30 million - $35 million.

Stock Recommendation:The stock generated a positive YTD return of 85.00%. The company has diversified its revenue and expanded into its existing market with remarkable results from Figure Eight execution. Considering company’s strong customer relationships, contribution from Figure Eight’s acquisition, FY19 first half performance and increase in earnings guidance, we have valued the company using two relative valuation methods, i.e., PE and EV/EBITDA multiples approach and arrived at a target price with lower double-digit upside (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $23.440, down 1.014% on 30 December 2019.

Marley Spoon AG

Annualised Revenue Run-Rate Improved by 55% on pcp:Marley Spoon AG (ASX: MMM) provides subscription-based weekly meal kit service, catering to customers in three primary regions, including Australia, United States and Europe.

Recently, the company announced proposed Supervisory Board changes, wherein it stated that Robin Low would be joining the Supervisory Board of the Company as an Independent, Non-Executive Director, subject to shareholders’ approval at an extraordinary general meeting.

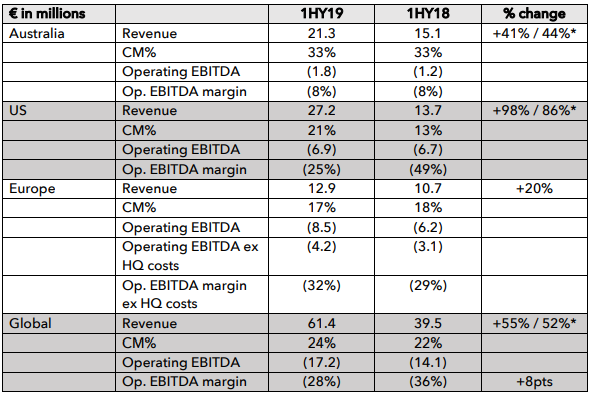

H1FY19 Key Financial Highlights for the period ended June 30, 2019:Annualised revenue run-rate increased by 55% to over A$200 million, as compared to the previous corresponding period. This can be attributed to major revenue gain in the second quarter. The number of active customers increased by 38% (y-o-y) to 172,000, while customer acquisition costs remained flat for the period.

H1FY19 Key Metrics for Segments (Source: Company Reports)

What to expect:As per the release, the company rolled out new manufacturing technology in Europe and Australia to provide the foundation for future scalability, increased menu choices and customer personalisation. Moreover, the company anticipates achieving a global contribution margin in the mid to high 20s for CY 2019 and to reach profitability on an operating EBITDA basis by 2020.

Stock Recommendation:The stock generated a negative YTD return of 37.50% and is currently trading close to its 52-week low of $0.180, proffering opportunity for accumulation. Company’s strategy is designed to support sustainable long-term revenue growth by attracting new customers along with retaining loyal high-value customers. On the valuation front, EV/Sales multiple on TTM basis stands at 0.4x, lower than the industry median of 0.6x, indicating an under-valued position at the current juncture.Considering the company’s business model, half yearly performance, decent outlook and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.250 on December 30, 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...