Stocks’ Details

Rio Tinto Limited

Rio Tinto Approves Investment in Pilbara Mines:Rio Tinto Limited (ASX: RIO) is primarily engaged in the business of minerals and metals exploration, development and marketing. The market capitalisation of the company stood at $35.63 billion as on 27th November 2019.Rio Tinto has approved an investment of $749 million or A$1 billion in its 100% owned Greater Tom Price operations to help maintain the production capacity of its world-class iron ore business in the Pilbara of WA.Investment in the WTS2 (Western Turner Syncline Phase 2) mine will enable mining of new and existing deposits. It includes the construction of a new crusher as well as a 13-kilometre conveyor.The construction will start in Q1FY20, and the first ore from the crusher is expected in 2021. The project is expected to report an attractive IRR with the capital intensity of about $25 per tonne of production capacity.

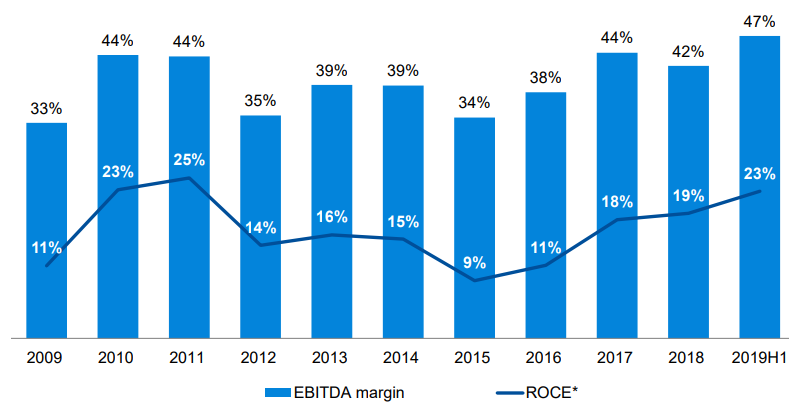

Company’s Margins and Return (Source: Company Reports)

Guidance for FY19 and FY20: PilbaraShipment guidance for 2019 remains unchanged at 320 to 330 million tonnes, and cash unit cost in the range of $14 to $15 per tonne.Sustaining capital expenditure is projected to be between $1 billion to $1.5 billion/year from 2020, as compared to the previous guidance of around $1 billion.360 Mtpa of annualised system capacity is expected once the Koodaideri phase 1 is fully commissioned, with first ore still expected late in 2021.

Stock Recommendation: As per ASX, Rio’s stock is currently trading above the average of 52-week high low and has risen by 15.95% in the last three months. Looking at the valuation multiple, the stock is trading at a price to book value multiple of 2.4x on TTM basis, which is above the industry (basic materials) median of 1.5x on TTM basis. Considering its current trading position and higher price to book value, we have an “Expensive” rating on the stock at the current market price of A$97.000 per share, up by 1.063% on 27th November 2019.

Fortescue Metals Group Limited

Fortescue Files an Application for Special Leave:Fortescue Metals Group Limited (ASX: FMG) is engaged in the business of exploration, development, production, processing and sale of iron ore. The market capitalisation of the company stood at $30.2 billion as on 27th November 2019. The company has filed an application for special leave as an appeal to the decision of the Full Federal Court in the matter of Fortescue Metals Group v Warrie.The company reassures that the decision of the Full Federal Court has no impact on its current or future operations or mining tenure at the Solomon Hub. Also, the company does not expect any material financial impact on the business as a result of the decision of the Full Federal Court.

Update on the Simandou Blocks 1 and 2 Tender: The Government of the Republic of Guinea has notified the company that it is not the preferred bidder in the recent tender for mining rights on mineral deposits on Simandou Blocks 1 and 2. The Guinean Government has instructed that it will continue with detailed negotiations with the preferred bidder over the coming months.

Guidance for FY20: The company issued a shipment guidance of 170 to 175mt for FY20, which includes 17-20mt of West Pilbara Fines products. C1 costs are expected to be in the range of US$13.25/wmt to US$13.75/wmt.Total capital expenditure is expected to be US$2.4 billion, with an average strip ratio of 1.5. Total dividend payout ratio is expected to be between 50% and 80% of full-year net profit after tax.

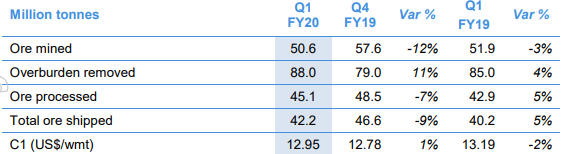

Production Summary (Source: Company Reports)

Stock Recommendation: The company has registered a CAGR growth of 78.07% in bottom-line over the previous five years (FY15 to FY19). Looking at the margins of the company, FMG has improved its net margin from 12.7% in FY18 to 32.0% in FY19. Its ROE has improved from 9.0% in FY18 to 31.4% in FY19. As per ASX, the stock has gained 16.09% in the last six months. Based on the increase in RoE and net margin, decent guidance for FY20, we give a “Hold” recommendation on the stock at the current market price of $9.790 per share, down by 0.204% on 27th November 2019.

BHP Group Limited

Mike Henry to Become CEO of the Company:BHP Group Limited (ASX: BHP) is among the world’s top producers of major commodities, like iron ore, metallurgical coal and copper. The company also has a substantial interest in oil, gas and energy coal. The market capitalisation of the company stood at $111.65 billion as on 27th November 2019.

After a detailed succession process, the Board of BHP has decided to appoint Mike Henry as the Chief Executive Officer (CEO) of the company, with effective from 1st January 2020.He was appointed in place of Andrew Mackenzie, the former CEO, who will retire on 31st December 2019.

Briefing of the Company’s Petroleum Operations: Geraldine Slattery, BHP’s President of Petroleum Operations, has announced that the petroleum segment is set to deliver strong returns and contribute significant value for BHP in the coming future due to its foundation of quality assets and attractive growth options.As per Ms Slattery, petroleum is a terrific business with competitive growth capability and is aligned with the company’s plan of being in the best commodities, with the best assets, supported by the best culture and capabilities.

She outlined a scenario that could possibly generate strong EBITDA margins of more than 60% and an average ROCE of more than 15% over the next decade.The scenario also displays the potential to deliver an average IRR of about 25% for major projects, which are resilient through cycles.

Petroleum Guidance (Source: Company Reports)

Outlook for FY20: The company remains cautious in the short-termbut is positive about the long-term outlook.It has a strong balance sheet and a portfolio of world-class assets.It has six major projects in iron ore, copper, oil and potash, on-track and in-line with the budget.

Stock Recommendation:The company has achieved a decent CAGR growth of 44.41% in its bottom-line over the past five years (FY15 to FY19). Its EBITDA margins stood at 50.8% in FY19, which is above the industry median of 29.1%. The company has improved its return on equity from 11.4% in FY17 to 16.8% in FY19. Based on its positive long-term outlook, improvement in its return ratios and good future of its petroleum business, we give a “Hold” recommendation on the stock at the current market price of $38.350 per share, up by 1.187% on 27th November 2019.

South32 Limited

Appointment of New Director:South32 Limited (ASX: S32) is a diversified mining and metals company, with a market capitalisation of A$13.05 billion as on 27th November 2019.

South32 Limited has appointed Guy Lansdown as an independent non-executive director of the company.He will join the company’s Board on 2nd December 2019 and seeks election by shareholders at next year’s AGM. He is a civil engineer with over 35 years of experience.

Company Signs an Agreement to Sell SAEC: The company has entered into a binding conditional agreement to sell 91.835% shareholding in South32 SA Coal Holdings Proprietary Limited (South Africa Energy Coal, SAEC) to a wholly-owned subsidiary of Seriti Resources Holdings Proprietary Limited and two trusts.

Outlook Remains Positive for the Company: The company expects to see an increase in production as Illawarra Metallurgical Coal returns to a three-longwall configuration and Worsley Alumina mayachieve nameplate capacity. Lower raw material costs, weaker currencies and efforts to mitigate inflation mainly in energy, labour and materials, may result in lower operating costs in many of its operations.

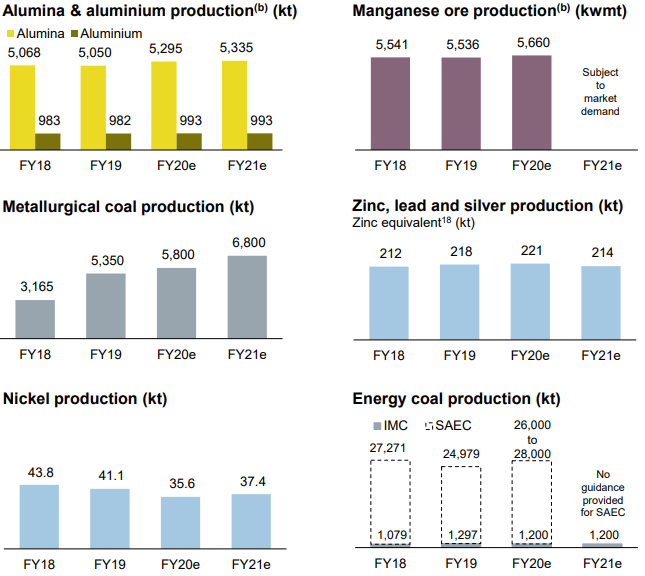

Production Overview (Source: Company Reports)

Stock Recommendation: As per ASX, the stock is trading below the average of 52-week high and low. The stock has corrected 23.70% in the last six months. The stock is trading at a price to cash flow multiple of 5.7x, which is below the industry (basic materials) average of 16.6x on a TTM basis. The company’s gross margins stood at 67.3% in FY19, which is above the industry median of 41.1%. Based on its current trading levels, lower valuation multiple and decent gross margins, we give a “Buy” recommendation on the stock at the current market price of $2.670 per share, up by 1.136% on 27th November 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...