.png)

Syrah Resources Limited

Q1 2019 Graphite Production Beats the Guidance: Syrah Resources Limited (ASX: SYR) recorded graphite production numbers from the Balama Graphite Operation (“Balama”) for Q1 2019 at 48kt beating the given guidance of ~45kt by the company. The company stated that higher recovery, availability of plant and utilisation in 2nd half of March resulted in a record month of production of ~19kt. Graphite sales volume came in at 48kt, which was at the upper end of its guidance range at 45kt-50kt. With regards to sales and pricing, weighted average price achieved stood at US$469 per tonne (CIF).

SYR completed the period with cash of US$62 million, beyond the given guidance of between US$55 million and US$57 million.

.png)

Balama Graphite Operation - Q1 2019 Preliminary Update (Source: Company Reports)

Stock Recommendation: On this news (released on 04 April 2019), stock zoomed 13.03% from its previous day closing price. Looking the annual price performance, the company’s stock has delivered the return of -63.54%. Stock soared ~33% during 01-04 April 2019 (estimated from the closing price).

After a sharp run up, stock has seen short built up of 16.5% (as per the ASIC report of 09 April 2019).Currently, the stock is trading close to 52-week lower level of $0.975, proffering a decent opportunity for accumulation.Its current ratio stood at 5.02x in FY18 which is better than the industry median of 1.51x. Its D/E ratio stood at 0.01x in FY18 which is below the industry median of 0.14x, which implies better debt servicing by the company. Based on the foregoing, we maintain our “Speculative Buy” recommendation on the stock at the current market price of $1.135 per share (down 0.873% on 15 April 2019).

Galaxy Resources Limited

Trading at Lower level: Galaxy Resources Limited (ASX: GXY), an Australian Miner, on 11 April 2019, informed that company will release its 1Q FY19 results pre-market open on 18 April 2019 following by an investor conference call on same day.

Earlier, the company has announced Mr. Simon Hay as its new Chief Executive Officer with effect from 1 July 2019.

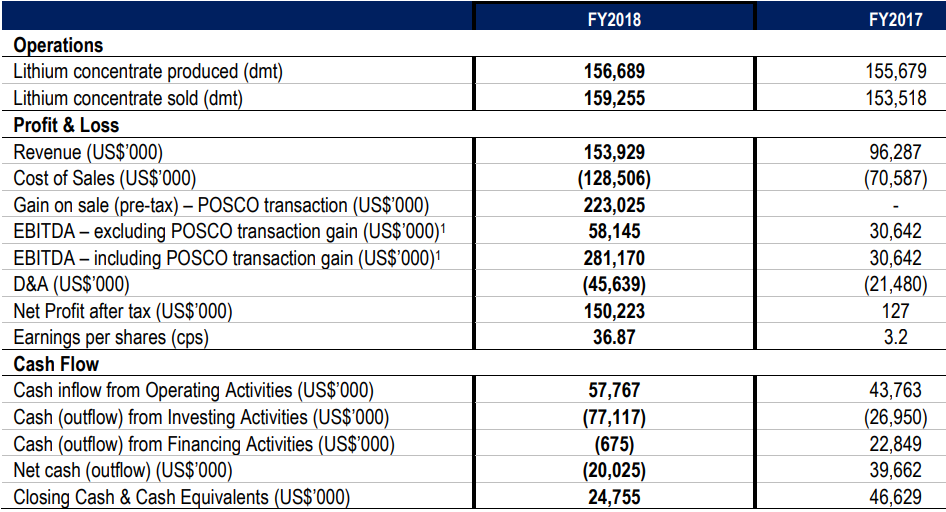

Financial Performance in FY18: TheCompany sold 159,255 dmt in FY18 resulting in cash receipts of US$154.9 million in the same period. The revenues witnessed a strong growth of 60% to US$153.9 million compared to FY17, mainly on the back of higher realized selling prices. Higher payments to suppliers, contractors and employees including higher operational costs partially offset the revenues.

The Group EBITDA for the same period came in at US$281.2 million (including a pre-tax gain on sale of US$223.0 million from POSCO transaction).The group net profit after tax (excluding the POSCO gain) was US$3.5 million, 26 times increase compared to FY17.

Financial and Operations Summary (Source: Company Reports)

Galaxy happens to be in the strong financial position with an operating assetwhich produces robust free cash flow and with zero debt balance sheet and a substantial cash balance.These reflects Galaxy’s organic growth strategy and its commitment to the advancement of its tier-one assets, Sal de Vida and James Bay.

Stock Recommendation: At the current market price of $1.820 per share, stock is trading at price to earning multiples of 3.510x with market capitalization of $747.81 million. Currently, the stock is trading close to 52-week lower level of $1.805, providing a good opportunity for accumulation. The stock experienced a short interest of more than 17.17% (as per the ASIC report of 09 April 2019).

The successful completion of POSCO transaction and strong results posted in FY18 might attract the attention of market players. However, in the past 6 months, returns were -22.57% and in the past three months, it was -18.08%. Hence considering the above factors and current trading level, we maintain our “Speculative Buy” recommendation on the stock at the current market price of A$1.820 per share (down 0.817% on 15 April 2019).

JB Hi-Fi Limited

Healthy ROE at 16.0% in 1H FY19: JB Hi-Fi Limited (ASX: JBH) recently announced that one of its substantial holder Ellerston Capital Limited and its associates reduced its stake from 8.31% to 7.12%. Moreover, Airlie Funds Management Pty Ltd on its own behalf and on behalf of Magellan Financial Group Ltd and its related bodies corporate in Annexure A has reduced its voting rights to 5.54% from 6.65%.

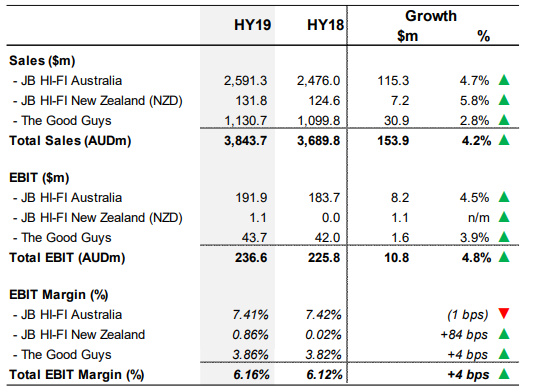

Financial Performance for 1H FY19: JBH reported NPAT at $160.1 million (up 5.5%) in 1H FY19 as compared to 1H FY18 at $151.7 million. The group EBIT saw a pcp growth of 4.8% to $236.6 million with EPS at 139.4 cps, up 5.4%. JBH reported solid numbers for 1H FY19, largely attributed to improved JB Hi-Fi New Zealand business performance.

Let’s have a look at the guidance for FY 2019. Going forward, the management expects to open five JB HI-FI Australia stores (1HY19: four, 2HY19: one) and two The Good Guys stores (1HY19: two, 2HY19: nil). Under the business strategy, the company plans to close two JB HI-FI Australia stores (1HY19: nil, 2HY19: two) and one JB HI-FI New Zealand store (1HY19: one, 2HY19: nil). The management expects group sales to be circa $7.1 billion and group NPAT between $237 million - $245 million.

Group Performance Overview (Source: Reports)

Stock Recommendation: At CMP of $24.990 per share, the stock is trading at price to earnings multiple of 11.930x with market cap of $2.88 billion. Annual dividend yield for the stock stands at 5.46%. Looking at the price performance, stock has gone down 2.79% on annual basis whereas on YTD and 3-months basis, stock has gained 16.11% and 17.97%, respectively. The stock experienced a short interest of ~15.5% (as per the ASIC report of 09 April 2019).

Considering the above-mentioned factors, we keep our watch stance intact on the stock at current market price of $24.990 per share.

NEXTDC Limited

ROE in negative territory since 2HFY18:NEXTDC Limited (ASX: NXT), independent data centre operator, updated about the change in substantial holding of Challenger Limited which was increased to 6.36% from 5.04% earlier.

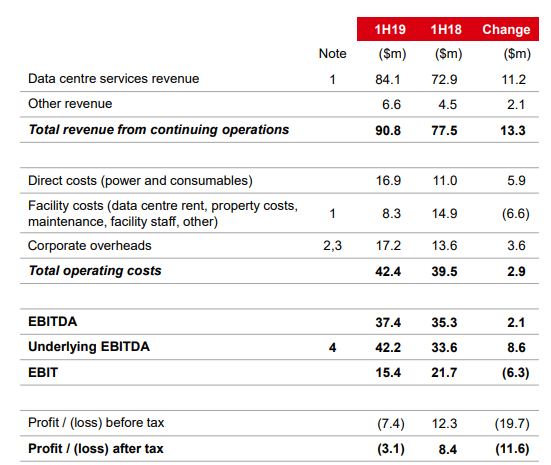

Looking at the key ratios for the company, net profit margins is negative in 1H FY 2019 as the figure stood at -3.5%, largely below the industry median of 24.7%. ROE also remained in negative territory at -0.4% in 1H FY19 depicting no value generation for its shareholders as compared to its industry median ROE at 9.4%.

1H FY 2019 Key Metrics (Source: Company Reports)

Stock Recommendation: At CMP of $5.930, market capitalization for the stock stands at $2.06 billion. Stock has not rewarded its investors as its returns stood at 8.70% for last one-year. 52-week high and low range for the stock is at $8.190-$5.610. The stock experienced a short interest of ~14.5% (as per the ASIC report of 09 April 2019).

Considering the aforesaid factors, we retain our avoid stance on the stock at the current market price of $5.930 per share (down 0.836% on 15 April 2019).

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...