.png)

Stocks’ Details

Iluka Resources Limited

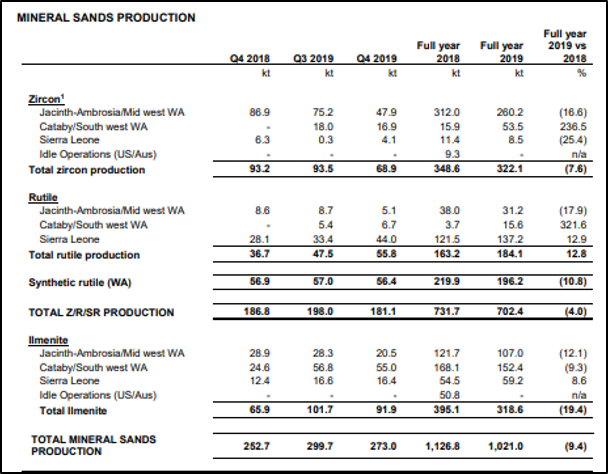

Signing of Sales Agreement with Kronos Worldwide Inc: Iluka Resources Limited (ASX: ILU) is engaged in the production of mineral sand. The market capitalisation of the company stood at A$3.77 Bn as on 29th January 2020. Recently, the company notified the market with the quarterly activities (period ended 31st December 2019) and reported that production of zircon, rutile and synthetic rutile for the full-year 2019 stood at 702,000 tonnes, reflecting a fall of 4% as compared to 2018. Moreover, zircon, rutile and synthetic rutile 2019 sales stood at 681,000 tonnes, which include full-year zircon sales of 274,000 tonnes, in line with the guidance provided.

During the quarter, Iluka and Kronos Worldwide Inc have inked a sales take-or-pay offtake agreement for 75% of standard grade rutile (SGR) produced from the Sierra Rutile operation, which will be effective through to December 2022. The agreement between Iluka and Kronos Worldwide Inc provides certainty as well as security for both the parties with respect to the Siierra Rutile operation.

Mineral Sand Production (Source: Company Reports)

Anticipation of Strong Demand: The company stated that the business and consumer confidence in the zircon market has continued to be affected by a soft outlook for global economic growth. With respect to the titanium dioxide feedstock market, the company is expecting welding and sponge market demand to remain strong with multiple inquiries for additional supply.

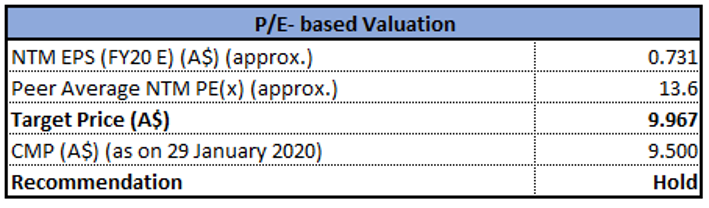

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: During the quarter, the company continues to progress work on its pipeline of projects. As at 31st December 2019, cash balance of the company stood at $43 million, reflecting free cash flow of $140 million in 2019 while investment of $198 million in capital expenditure. Current ratio of the company stood at 2.28x in 1H FY19 as compared to the industry median of 1.87x. This reflects that the company is in a decent position to address its short-term obligations. We have valued the stock using P/E based relative valuation approach, and for the purpose, we have taken peers such as Whitehaven Coal Ltd (ASX: WHC), South32 Ltd (ASX: S32) and BHP Group Ltd (ASX: BHP), and arrived at a target price offering an upside of single-digit (in percentage terms). Therefore, considering the decent liquidity position and favourable valuation, we maintain a “Hold” rating on the stock at the current market price of A$9.500 per share, up by 6.383% on 29th January 2020. The movement in share price was largely due to the release of quarterly results.

Sandfire Resources Limited

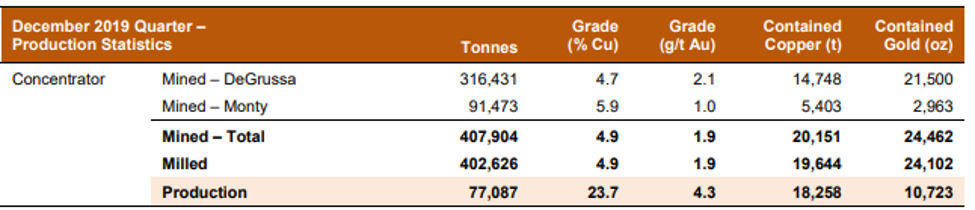

A quick look at Q2 FY20:Sandfire Resources Limited (ASX: SFR) is engaged in the exploration of gold and base metal. The market capitalisation of the company stood at A$996.96 million as on 29th January 2020. The company has updated the market with December 2019 quarterly activities (Q2 FY20) and outlined that the total recordable injury frequency rate (TRIFR) for the quarter stood at 6.0 as compared to 4.7 for the September 2019 quarter. When it comes to operations, copper production for the period stood at 18,258 tonnes of contained copper. Moreover, optimisation of the Feasibility Study for the T3 Copper-Silver Project in Botswana is underway, which is focusing on open pit optimisation, plant scale as well as operating costs.

Production Statistics (Source: Company Reports)

Production Guidance:For FY20, the company is expecting production in the range of 70,000 tonnes – 72,000 tonnes of contained copper. The production of gold is forecasted between 38,000 ounces – 40,000 ounces of contained gold. The company is anticipating C1 cash operating costs to be around US$0.90/lb.

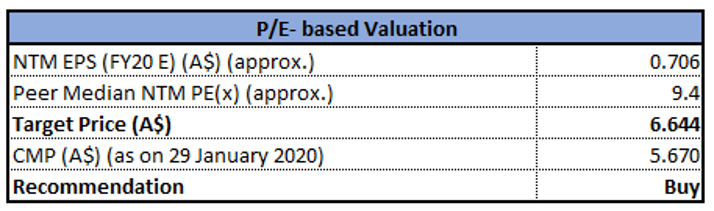

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Net margin of the company stood at 17.6% in FY19 against the industry median of 10.9%. This reflects that the company has decent capabilities to convert its top-line into bottom-line. Return on equity of the company stood at 18.8% in FY19 as compared to the industry median of 12.0%, demonstrating decent returns provided to shareholders. We have valued the stock using P/E based relative valuation approach, and for the purpose, we have taken peers such as IGO Ltd (ASX: IGO), Western Areas Ltd (ASX: WSA) and Fortescue Metals Group Ltd (ASX: FMG), and arrived at a target price offering an upside of lower double-digit (in percentage terms). Thus, in the light of decent profitability margin and returns provided to shareholders, we give a “Buy” recommendation on the stock at the current market price of A$5.670 per share, up by 1.25% on 29th January 2020.

Evolution Mining Limited

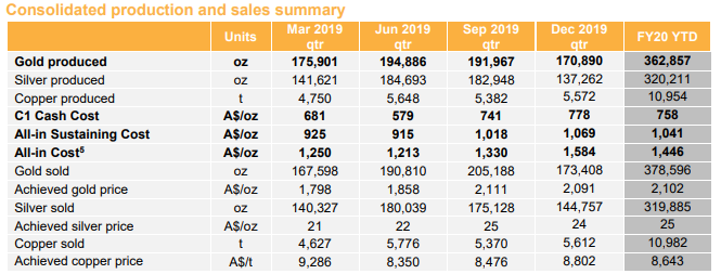

Acquisition of Red Lake Gold Complex: Evolution Mining Limited (ASX: EVN) is engaged in the exploration, mine development, mine operations as well as the sale of gold and gold/copper concentrate in Australia. The market capitalisation of the company stood at A$6.58 Bn as on 29th January 2020. Gold production for the December 2019 quarter stood at 170,890 ounces with All-in Sustaining Cost (AISC) of A$1,069/oz. During the quarter, the company made significant progress in decreasing reliance on surface fresh water at Cowal. EVN also announced the acquisition of the high grade, long life Red Lake gold complex in Ontario, Canada from Newmont, for a consideration of US$375 million in cash and up to an additional US$100 million, which is payable upon new resource discovery.

Production and Sales Summary (Source: Company Reports)

What to Expect: The company is anticipating gold production to be approximately 725,000 ounces for FY20. Also, for FY20, the company is expecting AISC in the ambit of A$940 – A$990 per ounce. The acquisition of Red Lake gold complex is anticipated to close at the end of March 2020.

Valuation Methodology: P/CF Multiple Approach

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Net mine cash flow for the quarter stood at A$144.4 million, with group free cash flow amounting to A$83.8 million. During the quarter, the company paid outstanding debt amounting to A$275.0 million. It witnessed a rise in net cash position by A$78.6 million to A$170.3 million. We have valued the stock using P/CF based relative valuation approach, and for the purpose, we have taken peers such as Newcrest Mining Ltd (ASX: NCM), Northern Star Resources Ltd (ASX: NST), IGO Ltd (ASX: IGO), etc., and arrived at a target price offering an upside of higher single-digit (in percentage terms). Thus, considering the decent cash flows, valuations, and value-accretive growth via M&A, we give a “Buy” recommendation on the stock at the current market price of A$3.780 per share, down by 2.073% on 29th January 2020.

OZ Minerals Limited

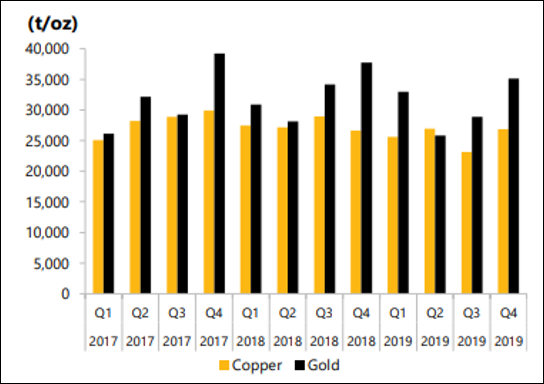

Achieved Major Milestone: OZ Minerals Limited (ASX: OZL) is a mining company focused on copper. The market capitalisation of the company stood at A$ 3.17 Bn as on 29th January 2020. The company recently announced the results of Q4 FY19 and stated that 2019 has proved to be a year of major progress for the company. With respect to Prominent Hill, the company reported copper production of 26,845 tonnes and gold production of 35,102 ounces. This reflects that the company has marked the fifth consecutive year of reliable performance at Prominent Hill where the company has achieved production at the upper end of guidance. It added that the Carrapateena project has achieved a major milestone during the quarter, with production of the first saleable copper-gold concentrate.

Prominent Hill Production (Source: Company Reports)

Focus of OZL: The focus of the company revolves around the ramp-up of Carrapateena and achieving the 4.25Mtpa production rate by the end of 2020. It is also focused on maintaining reliable production and cost performance at Prominent Hill. OZL’s focus also includes completing the West Musgrave PFS and removal of the CentroGold injunction in the Gurupi Province.

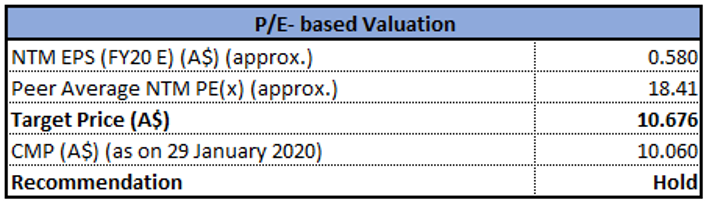

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company has continued to develop its growth pipeline with the West Musgrave Pre-Feasibility Study (PFS), which is near to completion. The company remains optimistic about the long-term demand for copper from traditional sources. We have valued the stock using P/E based relative valuation approach, and for the purpose, we have taken peers such as IGO Ltd (ASX: IGO), Northern Star Resources Ltd (ASX: NST) and Newcrest Mining Ltd (ASX: NCM), and arrived at a target price offering an upside of single-digit (in percentage terms). Hence, taking into account the performance during the December quarter and continued focus on future growth, we maintain a “Hold” rating on the stock at the current market price of A$10.060 per share, up by 2.863% on 29th January 2020.

Comparative Price Chart (Source: Daily Technical Chart)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...