.png)

Stocks’ Details

Santos Limited

Disciplined Operating Model: Santos Limited (ASX: STO) is engaged in the exploration and production of gas and petroleum. As on 23 April 2020, the market capitalization of the company stood at $8.31 billion. The company has recently released its report for the first quarter ending 31 March 2020, wherein it reported strong free cash flow of US$265 million and liquidity of over US$3 billion. The company reported a disciplined operating model and drilled 112 new wells across its onshore assets despite wet weather impacts.

During the first quarter, the company produced 17.9 mmboe and sold 22.3 mmboe. In the same time span, revenue of the company stood at $883 million.

.png)

Quarterly Operation and Financial Performance (Source: Company Reports)

Future Guidance: The company has provided guidance for FY20 and expects to produce 73-80 mmboe. Based on the current business conditions and the projected impact of COVID-19, sales volumes from the base business are expected to be at the lower end of the guidance range of 101-109 mmboe. It also anticipates unit production costs of around $6.70-7.10 per boe.

Valuation Methodology: Price to Earnings Multiple Based Valuation (illustrative)

.png)

Price to Earnings Multiple Based Approach (Source: Thomson Reuters), *1USD=1.58 AUD

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of STO gave a return of 36.64% in the past one month and is trading close to its 52-week low of $2.730, proffering a decent opportunity for accumulation. During FY19, net margin of the company stood at 16.1%, higher than the industry median of 11.6%. Considering the returns, trading levels, and future guidance, we have valued the stock using Price to Earnings multiple based illustrative valuation method and have arrived at a target upside of lower double-digit (in percentage terms). For the said purposes, we have considered Oil Search Ltd, Worley Ltd and Origin Energy Ltd., as peers. Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $4.26, up by 6.767% on 23 April 2020, owing to its recent quarterly results.

Ramelius Resources Limited

Update on Spectrum Metals Takeover: Ramelius Resources Limited (ASX: RMS) is engaged in the mining, production, and exploration of gold. As on 23 April 2020, the market capitalization of the company stood at $919.13 million. The company has reached a relevant interest of 50.5% in Spectrum Metals Limited and has declared an unconditional offer for an off-market takeover. The company is offering one RMS share for every ten Spectrum shares held for a cash consideration of $0.017 per share. The offer is open till 29 May 2020.

During the quarter ended 31 March 2020, the company reported a strong balance sheet with cash and gold of $90.4 million. In the same time span, the company produced 51,825 ounces of gold. During 1H20, the company reported a revenue of $158.5 million and witnessed a substantial increase of 329% in NPAT to $20.5 million.

.png)

1H20 Financial Highlights (Source: Company Reports)

Future Guidance: The company will continue to maintain its full year guidance for FY20 and expects to produce 205,000 - 225,000 ounces at an AISC of A$1,225 – 1,325/oz. The company has also begun the process of rationalizing non-essential exploration activities to reduce the travel requirements. RMS is well placed to accommodate both future mine development decisions and other acquisition opportunities.

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (illustrative)

.png)

EV/EBITDA Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of RMS gave a negative return of 6.27% in the last three months but a positive return of 38.95% in the past one month. During 1H20, EBITDA margin of the company stood at 41.3%, higher than the industry median of 36.6%. Considering the returns, future guidance, and decent financial performance, we have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and have arrived at an upside of higher single-digit (in percentage terms). For the said purposes, we have considered Regis Resources Ltd, Red 5 Ltd and Silver Lake Resources Ltd (ASX: SLR) as peers. Hence, we recommend a ‘Hold’ rating on the stock at the current market price of $1.24, up by 3.766% on 23 April 2020, owing to its recent update on Spectrum Metals Takeover.

Westgold Resources Limited

Update on the Asset Sale and Activity: Westgold Resources Limited (ASX: WGX) is engaged in the exploration, development, and operation of gold mines, primarily in Western Australia. As on 23 April 2020, the market capitalization of the company stood at $827.79 million. The company has recently stated that it has decided to sell the Albury Heath project to Big Bell Gold Operations Pty Ltd for a total sale price of $1.3 million.

Decent Increase in Revenue and NPAT: During 1H20, the company reported a substantial improvement in financial outcomes with an increase of 18% in revenue to $228.9 million and a growth of 187% in NPAT to $9.75 million. In the same time span, the company produced 120,127 ounces of gold at C1 Cash costs of $1,236/oz and repaid 7,500oz of gold loans, reducing the balance to 7,500oz. During the half year, the mining segments of Meekatharra Gold Operations and Fortnum Gold Operations were very profitable while the performance of the Cue Gold Operations reflects its development phase.

.png)

1H20 Financial Highlights (Source: Company Reports)

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of WGX gave a negative return of 10.78% in the last three months but a positive return of 31.43% in the past one month. Despite the global pandemic, the company’s mining sites continue to operate with full capacity, minimizing any future disruption on business. Considering the returns, decent financial performance and minimized future disruption in the business, we have valued the stock using Price to Cash Flow Illustrative Multiple Approach valuation approach and have arrived at an upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $2.140, up by 3.382% on 23 April 2020, due to its recent update on the sale of the Albury Heath project.

Lynas Corporation Limited

Lynas Selected for Phase 1 of US HRE Separation Facility: Lynas Corporation Limited (ASX: LYC) is engaged in the production of Rare Earths concentrate at Mt Weld. As on 23 April 2020, the market capitalization of the company stood at $972.84 million. The company has recently stated that it has been awarded a Phase I contract for a U.S. based Heavy Rare Earth separation facility. This will allow detailed planning and design work for the construction of a U.S. based Heavy Rare Earth separation facility.

The company has recently released its quarterly report for the period ending 31 March 2020, wherein it reported total REO production of 4,465 tonnes and sold 4,601 tonnes of REO. In the same time span, the company reported a closing cash balance of $124.6 million and invoiced sales revenue of $91.2 million.

.png)

Quarterly Operational Performance (Source: Company Reports)

What to Expect: The company expects a strong demand from its customers in Japan, Europe and the U.S. and is focused on providing them with a secure source of sustainably produced Rare Earths. Despite the current challenges of COVID-19, LYC remain committed to progressing its 2025 growth plan.

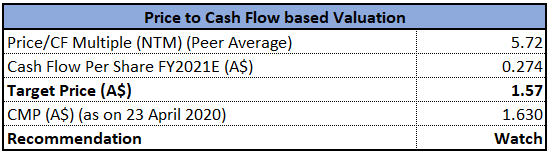

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (illustrative)

Price to Cash Flow Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of LYC gave a negative return of 42.36% in the last three months and a positive return of 25.11% in the past one month. The stock is inclined towards its 52-weeks’ low level of $1.035. During 1H20, EBITDA margin of the company stood at 24.7%, lower than the industry median of 36.6%. Considering the volatility in returns, trading levels, and positive outlook, we have valued the stock using price to cash flow based illustrative valuation approach and have arrived a downside of lower single digit (in percentage terms). For the said purposes, we have considered Western Areas Ltd, Imdex Ltd, and Champion Iron Ltd as peers. Hence, we recommend a watch stance on the stock at the current market price of $1.630, up by 16.846% on 23 April 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...