.png)

Stocks’ Details

oOh!media Limited

Robust Outlook With Debt Reduction Initiatives: oOh!media Limited (ASX: OML) is one of Australia's leading Out Of Home media companies and is engaged in offering advertisers the capability to create deep commitment between people and brands across Australia and New Zealand. On 15th January 2020, the company announced that Macquarie Group Limited (MQG) and its controlled bodies corporate, has become a substantial holder of the company with a voting power of 5.35%.

1H2019 Key Highlights: The company reported revenue of $304.9 million in 1HFY19, up 5% on pcp. Net profit after tax of the company came in at $9 million, down 24% year over year. Underlying EBITDA amounted to $56 million, down 4% on pcp. The company declared an interim fully franked dividend of 3.5 cents per share.

.png)

1HFY19 Highlights (Source: Company Reports)

Outlook: For FY19, the company now expects underlying EBITDA in the range of $138 Mn to $143 Mn. Growth in operational expenditure is likely to be within the range of 5% and 7%. Capital expenditure for FY19 is projected to be in the band of $55-$70 million. The company is aiming for lowering its debt with positive cash flows in 2HFY19 and targeting gearing below or close to 2.0X in FY20.

Valuation Methodology: EV/EBITDA Multiple Approach

.png)

EV/EBITDABased Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading above the average of its 52-week low and high of $2.290 and $4.740, respectively. The stock gave a return of 37.41% in the past three months. As per ASX, the stock has a market cap of $925.91 million with a PE multiple of 37.45x and an annual dividend yield of 2.88%, suggesting a decent opportunity for accumulation. Considering the decent financial performance, strong outlook and current trading levels, we have valued the stock using EV/ EBITDAmultiplebased relative valuation method and for the purpose, we have taken the peer group - Vocus Group Ltd (ASX: VOC), Village Roadshow Ltd (ASX: VRL) and Southern Cross Media Group Ltd (ASX: SXL), to name few. Therefore, we have arrived at a target price of higher single-digit growth (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $3.720, down 2.618% on 16th January 2020.

Nine Entertainment Co. Holdings Limited

Growth in Advertising & Subscription Revenues Key Positive: Nine Entertainment Co. Holdings Limited (ASX: NEC) operates in the media and entertainment segment, with a focus across linear television, digital, print and metropolitan radio.Recently, the company announced that one of its Directors, Mickie Rosenhas acquired 20,000shares for a consideration of $35,000. The company also notified that H1 FY20 results will be announced on 26 February 2020.

FY19 Highlights for the Period ended 30 June 2019: The company in a recent AGM announced that revenue in FY19 came in $2,341.7 million, down 1% year over year.Group EBITDA stood at $423.8 million, up by 10% year over year. The company has also declared fully franked dividends of 10 cents per share, an increase of 11% on a year over year basis.

.png)

FY19 Key Highlights (Source: Company Reports)

Outlook: The company remains positive on its share gain through the second half on the back of strong audience performance and is on track to lessen the impact of the challenges during the start of the year. The company continues to invest in growth schemes and is anticipating a low single-digit growth in FY20 Pro Forma Group EBITDA prior to the impact of AASB16.

Valuation Methodology: P/CF Multiple Approach

.png)

P/CFBased Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading above the average of its 52-week low and high of $1.362 and $2.13, respectively. The stock gave a return of 29.41% in the past one year. As per ASX, the stock has a market cap of $3.38 billion, with a PE multiple of 11.33x and an annual dividend yield of 5.05%, indicating a decent opportunity for accumulation. During the year, EBITDA margin improved from 18.8% in FY18 to 19.1% in FY19. Considering the improvement in EBITDA margin, modest outlook and current trading levels, we have valued the stock using P/CFbased relative valuation method and for the purpose, we have taken the peer group - Seven West Media Ltd (ASX: SWM), Carsales.Com Ltd (ASX: CAR) and Telstra Corporation Ltd (ASX: TLS), to name few. Therefore, we have arrived at a target price of higher single-digit growth (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $1.990, up 0.505% on 16th January 2020.

Seven West Media Limited

Debt Reduction & Cost-Cutting Initiatives Key Positives: Seven West Media Limited (ASX: SWM) is involved in offering free to air television and radio broadcasting, magazine & newspaper publishing. On December 2019, the company stated that Spheria Asset Management Pty Ltd became a substantial holder of the company, with a voting power of 6.23%. Recently, the company also updated on the issuance of 30,000,000 ordinary shares to Spheria Asset Management Pty Limited.

FY19 Highlights for the Period Ended 29 June 2019: The company reported revenue for the period at $1.56 billion, down ~4% year over year. The company reported underlying group net profit after tax at $129.3 million in FY19, whereas underlying group EBIT came in at $212.1 million. Earnings per share came in at 8.6 cents per share in FY19.

.png)

FY19 Key Highlights (Source: Company Reports)

Outlook: For FY20, the company anticipates Group EBIT to be in the band of $190 million to $200 million.

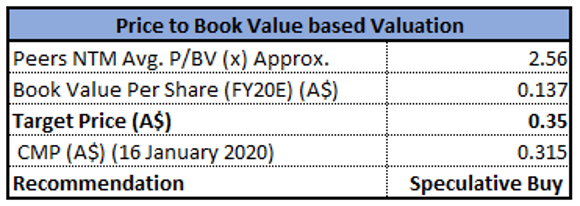

Valuation Methodology: P/B Multiple Approach

P/BBased Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week low level of $0.305.As per ASX, the stock has a market cap of $492.17 million, with 1.54 billion outstanding shares. The company aims to lower costs across the group, thus improving operational efficiency. Further, the company stays on track to enhance its balance sheet and decrease overall debt. Considering the backdrop of the above factors, we have valued the stock using P/B based relative valuation method and for the purpose, have taken the peer group - Seek Ltd (ASX: SEK), Nine Entertainment Co Holdings Ltd (ASX: NEC) and Telstra Corporation Ltd (ASX: TLS). Therefore, we have arrived at a target price with an upside of lower double-digit (in % terms). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.315, down 1.562% on 16th January 2020.

EVENT Hospitality & Entertainment Limited

ThredboContinues its Summer Resort Operations: EVENT Hospitality & Entertainment Limited (ASX: EVT) is involved in the business of motion picture showcase, operation of restaurants and hotels, possession and function of Thredbo Alpine Resort, ownership of hotel, cinemas & additional rental properties, etc. On 13th January 2020, the company announced that the Thredbo Alpine Resort will restart its summer resort operations, effective from 14 January 2020.The announcement followed the temporary closure of Thredbo, on the back of bushfires in Kosciuszko National Park (the “Park”) as declared on 2nd January this year.

FY19 Highlights for the Period ended 30 June 2019: The company’s FY19 revenue from continuing operations improved by 2% to $998 million on a year over year basis, and statutory net profit after tax was in line with the previous year and came in at $111.9 million.Group EBITDA for FY19 stood at $229 million, down 3% year over year.

FY19 Key Highlights (Source: Company Reports)

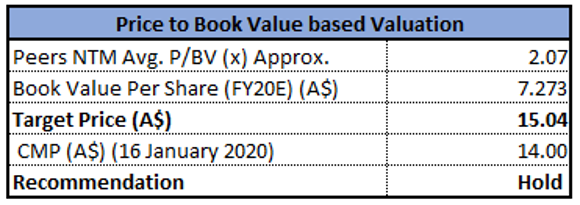

Valuation Methodology: P/B Multiple Approach

P/BBased Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week high of $14.280. The company is concentrating on growing its existing business revenue, boosting its asset performance and business transformation. Considering the backdrop of the above factors, we have valued the stock using P/BV multiple based relative valuation method and for the purpose, have taken the peer group - Ardent Leisure Group Ltd (ASX: ALG), LendLease Group (ASX: LLC) and Chorus Ltd (ASX: CNU). Therefore, we have arrived at a target price with an upside of higher single-digit (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $14.00, down 1.616% on 16th January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...