.png)

Stocks’ Details

Galaxy Resources Limited

Production Volume Stood at Upper end of Guidance: Galaxy Resources Limited (ASX: GXY) is engaged in the production of lithium concentrate for minerals in Australia, Canada as well as Argentina. The market capitalisation of the company stood at A$475 Mn as on 23rd January 2020. The company recently updated the market with the activities for Dec 2019 quarter. The company reported lithium concentrate production volume of 43,222 dry metric tonnes from Mt Cattlin, with grading 6.0% Li2O. This stood at the upper end of the production guidance range of 35,000 – 45,000 dmt. For the quarter, total sales volume stood at 29,778 dmt.

.png)

Production & Sales Statistics of Mt Cattlin (Source: Company Reports)

Guidance for Lithium Concentrate Production: The strategic drivers of the company involve prioritising value over volume, generating positive free cash flow, preserving resource life as well as maintaining balance sheet capacity for the benefit of the development portfolio. For Q1 FY20, the company is expecting lithium concentrate production volume in the ambit of 14,000 – 20,000 dmt following the restart of operation.

Valuation Methodology: EV/ Sales Multiple Approach

.png)

EV/ Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company was debt-free as at 31st December 2019 with cash and financial assets amounting to US$143.2 million. The company is also committed to regularly engaging with community stakeholders for providing positive, lasting benefits via employment opportunities as well as health and educational initiatives. We have valued the stock using EV/Sales based relative valuation approach, and for the purpose, we have taken peers such as Orocobre Ltd (ASX: ORE), Pilbara Minerals Ltd (ASX: PLS) and Altura Mining Ltd (ASX: AJM) and arrived at a target price of lower double-digit upside (in percentage terms). Thus, considering the cost reduction as a major focus at Mt Cattlin, debt-free position, and decent outlook, we give a “Speculative Buy” recommendation on the stock at the current market price of A$1.110 per share, down 4.31% on 23rd January 2020.

Galan Lithium Limited

Outstanding Lithium Results: Galan Lithium Limited (ASX: GLN) is engaged in the exploration of lithium and other metals. The market capitalisation of the company stood at a A$32.66 Mn as on 23rd January 2020. GLN through a release, notified the market that Ganfeng Lithium International has joined the share register of the company through its wholly owned subsidiary GFL International Co., Limited. It added that Ganfeng Lithium International is the world’s largest and China’s largest lithium compounds producer. Also, the company has reported an excellent lithium assay result from its Rana de Sal tenement. The company stated that these results are a confirmation of the previous significant intercepts in drill data of high grade/low impurity lithium bearing brines, which was received from the Western Tenements. The data from Rana de Sal as well as Pata Pila would be utilised for the maiden resource estimate of the Western Tenements, which is anticipated during Q1 CY2020. The following picture provides an idea of cash flow for September 2019 quarter:

.png)

Net cash outflow from operating activities (Source: Company Reports)

What to Expect: The company would continue to deliver on its strategy for the advancement of shareholders’ interests as well as asset values via well-defined work programmes on GLN’s tenements. The company will also continue to implement a growth strategy for further exploration, acquisition and joint venture opportunities.

Stock Recommendation: At the end of September 2019 quarter, cash at bank of the company stood at around $2.5 million. During the same quarter, GLN successfully and safely wrapped up its drilling campaign at Pata Pila and Rana de Sal. The stock of GLN is trading at a price to book multiple of 2.0x as compared to the industry average (Chemicals) of 4.7x on TTM basis. Thus, considering the growth in gross margin on YoY basis, excellent lithium assay result from its Rana de Sal tenement, and implementation of growth strategy, we give a “Hold” recommendation on the stock at the current market price of A$0.205 per share on 23rd January 2020.

Orocobre Limited

ORE Inks Two Supply Contracts: Orocobre Limited (ASX: ORE) is a mineral exploration and production company, which focuses on developing lithium/potash resources in Australia. The market capitalisation of the company stood at A$955.61 Mn as on 23rd January 2020. The company recently notified the market that two contracts have been inked for the supply of battery grade lithium carbonate to top tier Chinese cathode manufacturers including B&M Science and Technology and XTC New Energy Materials. It added that one contract has been inked by Toyota Tsusho Corporation as joint sales and marketing agent, for production from the Olaroz Lithium Facility for the supply of battery grade lithium carbonate totaling to 7,200t and a second contract signed for the supply of a total of 2,880t of micronised battery grade lithium carbonate. The following picture provides an overview of production, sales and operational update for September 2019 quarter:

.png)

Key Operational Numbers (Source: Company Reports)

Outlook: Subject to the achievement of the planned shipping schedule, the indicative weighted average price of lithium carbonate sales for the December 2019 quarter is anticipated to be around US$5,400/tonne FOB. The company is focused on reducing the cost of production and building a strong balance sheet position.

Valuation Methodology: P/B Multiple Approach

.png)

P/B Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The Financial year 2019 has proved to be another year of achievement for the company, despite the challenging global lithium market in combination with a turbulent Argentine economy. We have valued the stock using a P/B based relative valuation approach, and for this purpose, we have taken peers such as Galaxy Resources Ltd (ASX: GXY), Resolute Mining Ltd (ASX: RSG) and Westgold Resources Limited (ASX: WGX). As a result, we have arrived at a target price, offering an upside of lower double-digit (in percentage terms). Therefore, in the light of the newly signed contracts and decent performance in FY19 and Q1 FY20, we maintain a “Hold” rating on the stock at the current market price of A$3.590 per share, down 1.644% on 23rd January 2020.

Pilbara Minerals Limited

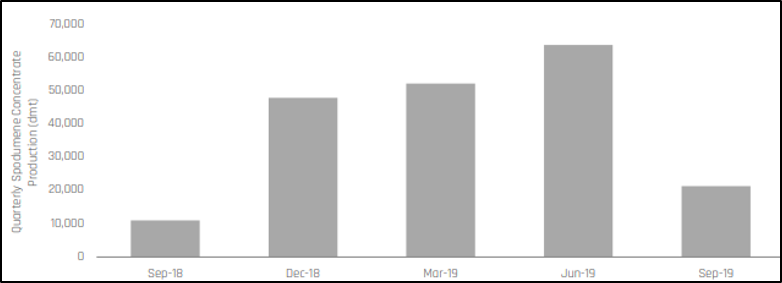

Improved Plant Performance: Pilbara Minerals Limited (ASX: PLS) is involved in the exploration of lithium and tantalum. The market capitalisation of the company stood at A$833.89 Mn as on 23rd January 2020. The company recently announced that Anthony William Kiernan has made a change to his holdings in the company by disposing 8,000,000 unlisted options at an exercise price of $0.626 on 12th December 2019. The company, in a recent presentation stated that it has experienced improved plant performance and product recovery at the Pilgangoora Lithium-Tantalum project. Also, the ramp-up of production is advancing well at Pilgangoora, with positive feedback from customers.

Spodumene concentrate Production (Source: Company Reports)

Positive Outlook for Demand: The company expects cash operating costs in the range of US$320 - $350/dmt CFR China from June 2020. The company is optimistic about its outlook for the long and medium-term demand for its spodumene concentrate.

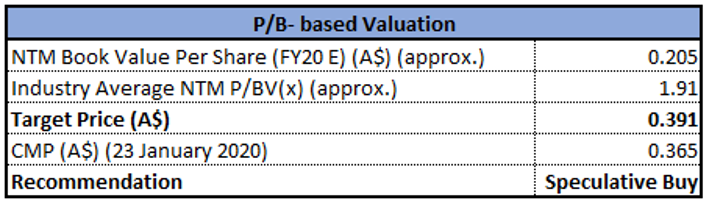

Valuation Methodology: P/B Multiple Approach

P/B Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company continues to consider the longer-term growth pathway for the Pilgangoora project on the back of a strong network of global customers and expected future demand for its high-quality product. We have valued the stock using a P/B based relative valuation approach and for this purpose, we have taken peer such as Galaxy Resources Ltd (ASX: GXY), Orocobre Ltd (ASX: ORE), Altura Mining Ltd (ASX: AJM) etc., and arrived at a target price, which is offering an upside of higher single digit (in percentage terms). Therefore, taking into account the improved plant performance and product recovery, positive outlook for its product and long-term growth pathway, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.365 per share, down 2.667% on 23rd January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...