Kalkine has a fully transformed New Avatar.

.png)

Stocks’ Details

Appen Limited

Strong Organic Growth in FY19:Appen Limited (ASX: APX) is engaged in the development of human annotated datasets for machine learning and artificial intelligence. In a recent announcement, the company updated that Mark Brayan, Director of the company, acquired 109,430 shares as a result of the vesting of Performance Rights.

Highlights of FY19 Results: During the year ended 31st December 2019, the company reported strong organic growth, that resulted in significant growth in revenue. Revenue for the period stood at $536 million, up 47% on the prior corresponding year. Underlying EBITDA went up by 42% and stood at $101 million in FY19. Annualised Recurring Revenue (ARR)from Figure Eight stood at $33.7 million at the end of the year, with a CAGR of 56% from 2015 – 2019.The company reported high revenue growth in Speech and Image, supported by multiple projects across major customers. During the year, dividend amounted to 5 cents per share as compared to 4 cents in FY18..png)

Income Statement (Source: Company Reports)

Outlook:The company has laid a strong foundation for future with its long-term relationships with customers that underpin growth in revenue. Over the coming few years, the company expects to increase its customer base through investments in sales and marketing, that is expected to result in softer margins in 1HFY20. Underlying EBITDA for FY20 is expected to be in the range of $125 million - $130 million, given the exchange rate of 1 AUD = 0.70 USD from Feb’20 – Dec’20.

Valuation Methodology: EV/Sales Based Valuation.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM- Next Twelve Months

Stock Recommendations: The stock of the company gave negative returns of 13.65% over a period of 1 month and is currently trading below the average of its 52-week trading range of $19.430 - $32. Since the company’s China operations are not too old, it expects a negligible impact from Coronavirus on FY20 results. It is targeting growth through investment in sales & technology and is looking forward to expanding its footprints into new geographies. We have valued the stock using EV/Sales based relative valuation method and for the purpose, have taken the peer group - Altium Ltd (ASX: ALU), Link Administration Holdings Ltd (ASX: LNK), WiseTech Global Ltd (ASX: WTC), etc. We have arrived at a target price with an upside of high single-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $22.800, up 2.703% on 03rd March 2020.

Computershare Limited

Continued Focus on Long-Term Growth Strategies:Computershare Limited (ASX: CPU) offers investor services, employee share plan services, business services, technology services, etc. The company recently updated that three of its Directors named Christopher John Morris, Joseph Mark Velli and Tiffany Kee Fuller, acquired 31,000, 7000 and 5000 ordinary shares, respectively.

1HFY20 Highlights: During the six months ended 31st December 2019, the company reported revenue amounting to $1,141.7 million, up 1.2% on the prior corresponding period. EBITDA for the period came in at $338.7 million, up 2.2% on pcp. During the half, the company executed on its long-term growth strategies and strengthened its competitive position in the market. Recurring revenues accounted for 78.3% of total revenues during the period, that speaks volumes about the quality of services offered by Computershare. Revenue from Issuer Services amounted to $430.5 million, with the new business stream including services such as Register Maintenance, Corporate Actions, Corporate Governance software products, etc. Revenue from US Mortgage Services went up by 42.6% on account of robust US housing market conditions. The Board declared an interim dividend amounting to 23 cents per share to be paid on 19th March 2020..png)

Revenue Break-up (Source: Company Reports)

Outlook: Going forward, the company expects continued momentum in Issuer Services, US Mortgage Services and Employee Share Plans that will offset the negatives impacting the business.Management EPS for FY20 is expected to go down by ~5%. Executing the long-term strategies to enhance the business quality and boost recurring revenues will remain a key focus area.

Valuation Methodology: Price to Cash Flow Based Valuation.png)

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 14.54% over a period of 1 month and is currently trading below the average of its 52-week trading range of $14.180 - $18.650. In 2HFY20, the company expects added contribution from the new US Issuer Services business. The company also has cost out programs in place that will promote added efficiencies on the platform. We have valued the stock using Price to Cash Flow based relative valuation method and arrived at a target price with an upside of high single-digit (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $15.020, down 2.086% on 03rd March 2020.

Empired Limited

Strong Growth in Operating Cash Flow:Empired Limited (ASX: EPD) provides financial instruments including bank loans, cash, trade receivables and trade payables.

1HFY20 Financial Highlights: During the half year ended 31st December 2019, revenue stood at $84 million, down 5% on the prior corresponding period. NPAT for the period amounted to $2 million, up slightly on prior corresponding period NPAT of $1.9 million. Operating cash flow for the period increased substantially, from $3.6 million in 1HFY19 to $11 million in 1HFY20. Increase in operating cash flow was a factor of increased rental expense and lease incentive. This increase coupled with a significant decline in CAPEX led to a reduction in net debt for the period..png)

Cash Flow (Source: Company Reports)

Outlook: During the first half, the company renewed a key contract with Rio Tinto, which is expected to contribute additional revenue in the second half and beyond. Full year FY20 NPAT & EPS are expected to go up significantly on FY19, on the back of a strengthened position in Australia with the renewed contract, a strong pipeline along with new contract wins in New Zealand and further decrease in CAPEX.

Stock Recommendation: The stock of the company gave positive returns of 26.79% over a period of 6 months and is currently trading above the average of its 52-week trading range of $0.235 - $0.470. The company’s strategic focus has been the reduction of overhead costs, capex and net debt, to boost cash flows. As suggested by the increase in operating cash flow in 1HFY20, the company has been justifying the strategy well and expects further progress in 2HFY20. Moreover, it is also negotiating additional contracts that will act as key catalysts for revenue growth in FY21. Considering the above factors, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.355 as on 03rd March 2020.

Praemium Limited

Record Performance in 1HFY20:Praemium Limited (ASX: PPS) is a provider of managed account, investment administration and financial planning services. In a recent announcement, the company updated that Michael Ohanessian, Director of the company, acquired 30,000 ordinary shares for a consideration of $0.355 per share.

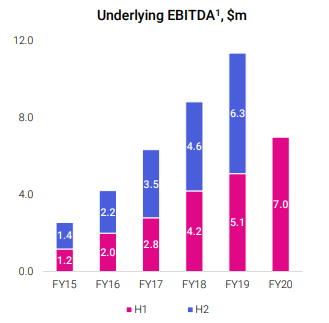

1HFY20 Results: During the half, the company reported revenue and other income amounting to $24.2 million, representing an increase of 5% on the prior corresponding half. For the first time in the company’s history, global Funds under Administration (FUA) crossed the $20 billion mark and International platform FUA exceeded $3 billion. Revenue from the Australian business went up by 13%, complimented by increase investment in R&D and innovation. EBITDA loss from the international segment decreased by 1%, with gross inflows from the segment up by 81%.

Underlying EBITDA (Source: Company Reports)

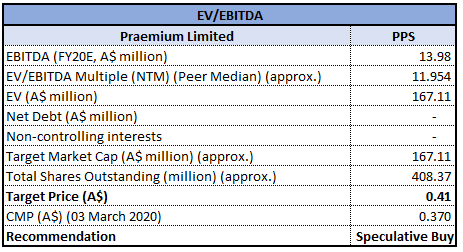

Valuation Methodology: EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM- Next Twelve Months

Outlook: During 2019, the company improved its competitive position by upgrading to a fully integrated managed accounts platform that received positive client feedback. Going forward, the company is expecting growth on the back of this key initiative, along with increased optimism from growth in the international business and growing popularity of the Virtual Managed Accounts (VMA) administration service.

Stock Recommendation: The stock of the company gave negative returns of 18.89% over a period of 1 month and is currently inclined towards its 52-week low level of $0.320. During 1HFY20, the company generated record underlying EBITDA of $7.0 million on the back of the factors discussed in the above section. We have valued the stock using EV/EBITDA based relative valuation method and for the purpose, have taken the peer group - OneVue Holdings Ltd (ASX: OVH), Netwealth Group Ltd (ASX: NWL), Hub24 Ltd (ASX: HUB), etc. We have arrived at a target price with an upside of low double-digit (in percentage terms). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.370, up 1.37% on 03rd March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...