Stocks’ Details

Dubber Corporation Limited

Dubber Signs Agreement with Telstra:Dubber Corporation Limited (ASX: DUB) operates a cloud-based software technology business with a market capitalisation of ~$233.31 million as on 3rd February 2020. Recently, the company announced that it has inked a deal with Telstra, Australia’s biggest telecommunications company, to facilitate Telstra customers to gain access to Dubber’s Call Recording and Data Capture Platform.

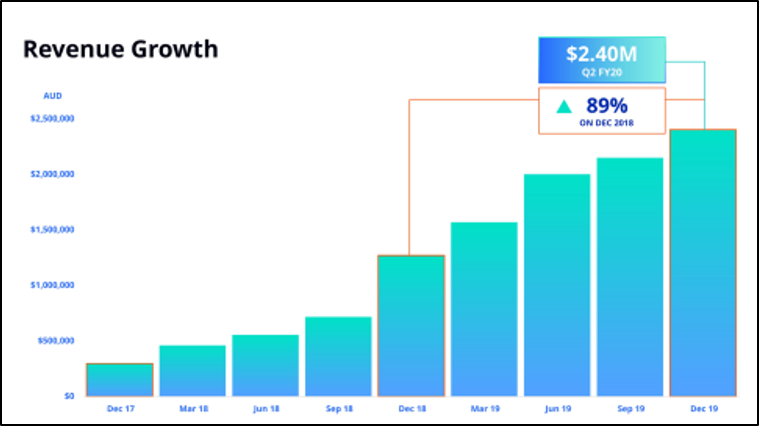

December Quarter 2019 Highlights: On 31st January 2020, the company provided an update on its operating focusfor the quarter ended 31 December 2019.The company reported revenues of $2.4 million during the quarter, an increase of 89% from the year-ago quarter. In terms of end user subscribers, the company had witnessed an increase to 122,000 numbers in comparison to 53,000 reported in the year-ago quarter. Telecommunications Service providers at the stage of billing increased to 65 from 52 reported in the year-ago period.

Revenue Growth Highlights (Source: Company Reports)

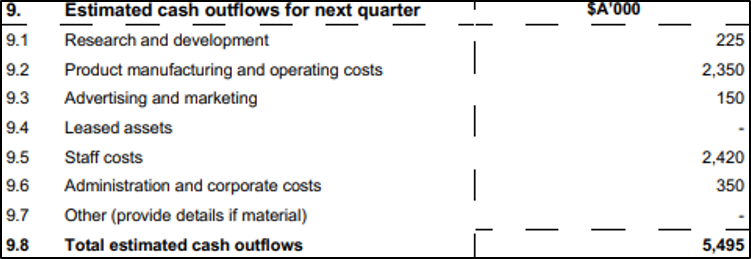

Cash Flow Details: Cash and cash equivalents at the end of the quarter stood at $15.336 million. The company’s net cash used in operating activities stood at $2.218 million, which includes $2.361 million for product manufacturing and operating costs, $1.964 million used for staff costs and $0.390 million for administration and corporate costs. For the coming quarter, the company estimates cash outflows of $5.495 million.

Projected Cash Flow (Source: Company Reports)

Stock Recommendation: As per ASX, the stock of DUB is trading above the average of its 52-week low-high of $0.445 and $1.760, respectively. Over a period of 1 year, the stock gave whopping returns of 174.16%. For FY19, the company’s current ratio stood at 9.46x, higher than the industry median of 1.75x, which reflects that the company is in a decent position to address its short-term obligations in comparison to the broader industry. The company is continuously focussed on boosting the number of active users and increase revenue. Also, DUB is focussed on expanding the global footprint of telecommunication carrier networks. Considering the returns on stock and current trading levels, we give an “Expensive” recommendation on the stock at the current market price of $1.175, down by 3.689% on February 3, 2020.

Telstra Corporation Limited

T22 strategy & 5G Expansion are Key Positives: Telstra Corporation Limited (ASX: TLS) is involved in providing telecommunication and information services, which consist of mobiles, internet and pay television. The market capitalisation of the company stood at ~$45.67 Bn as on 3rd February 2020. In FY19, TLS made a one-off issue of 13,245,705 retention rights to qualified employees. As on 15th January 2020, 7,673,385 retention rights were outstanding.

Key Takeaways from Investors Day 2019: The company recently notified that the T22 strategy is executing multiple jobs, which involves delivering cost reductions and streamlining its business.The mobile business of the company is continuing to return to a more rational market as the company goes through the expansion of 5G. In NAS, Telstra is on track to achieve profit margins in mid-teens through a constant focus on cost reduction initiatives coupled with lucrative NAS products.

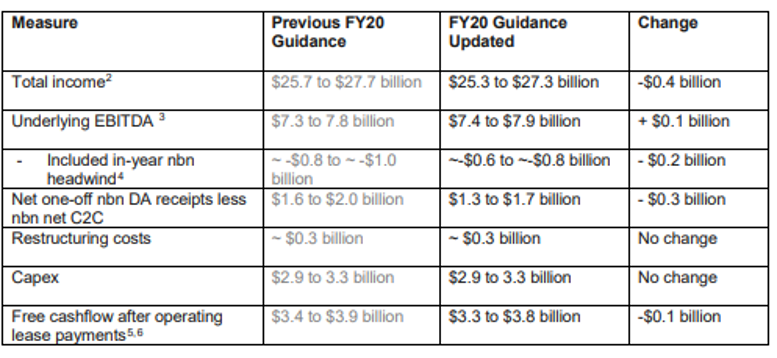

What to Expect: In FY2020, the company expects Capex to be in the range of $2.9 billion- $3.3 billion. Total income is now expected to be in the range of $25.3 to $27.3 billion in FY20, as compared to the previously guided range of $25.7 to $27.7 billion. Underlying EBITDA is expected to be between $7.4 to $7.9 billion as compared to the previously guided range of $7.3 to $7.8 billion.It anticipates additional restructuring costs amounting to ~$300 million in FY20.

Revised FY20 Outlook (Source: Company Reports)

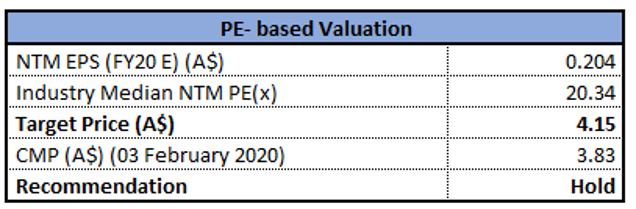

Valuation Methodology:P/E Based Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week high level of $3.978. The stock gave a positive return of 25.66% over a period of 1 year. Gross margin of the company stood at 63.8% in FY19 as compared to the industry median of 61.0%. ROE of the company stood at 14.8% in FY19 as compared to the industry median of 5.7%. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., Price to Earnings Multiple. For the purpose, we have taken the peer group – TPG Telecom Ltd (ASX: TPM), Macquarie Telecom Group Ltd (ASX: MAQ), Vocus Group Ltd (ASX: VOC), to name few, and arrived at a target price offering higher single-digit upside (in % terms). Hence, looking at the current trading levels and business prospects, we recommend a “Hold” rating on the stock at the current market price of $3.83, down 0.26% as on 3rd February 2020.

TPG Telecom Limited

FY19 Actual EBITDA Ahead of Expectations: TPG Telecom Limited (ASX: TPM) is engaged in the provisioning of consumer, wholesale as well as corporate telecommunications services. The market capitalisation of the company stood at ~$6.94 Bn as on 3rd February 2020.

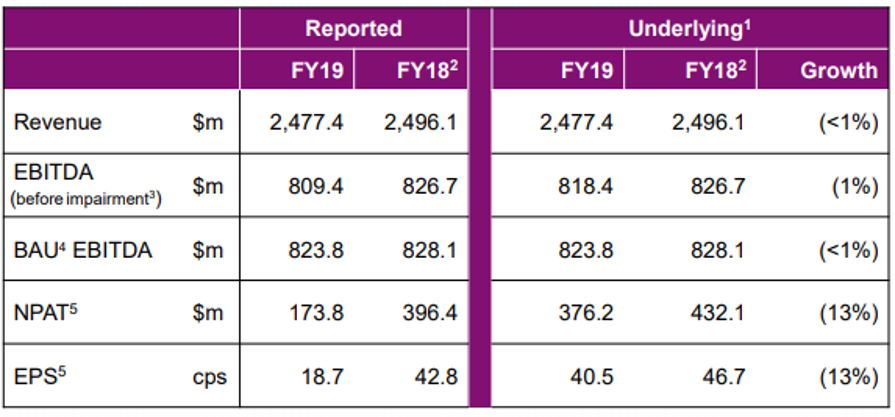

Key Highlights for FY19:During the financial year ended 31st July 2019, the company reported revenue of $2,477.4 million, a decline of approximately 1% on a year over year basis. Underlying EBITDA (before impairment) stood at $818.4 million, down from $826.7 million in FY18. Underlying net profit after tax in FY19 came in at $376.2 million, down 13% on a year over year basis. Underlying EPS for the period came in at 40.5 cents per share as compared to 46.7 cents per share in FY18.

FY19 Key Highlights (Source: Company Reports)

Outlook for FY20: The company is expected to witness the biggest financial impact in FY20 from customer migration to NBN, together with the headwinds from residential DSL. The home phone customers moving to NBN is expected to be ~$85 million. TPG forecasts to have less than 15% of its residential broadband customer base remaining on ADSL by the end of FY20. BAU EBITDA, i.e., EBITDA relating to existing Consumer and Corporate Division operations, is expected to be in the range of $735-$750 million.

Stock Recommendation: As per ASX, the stock is trading close to its 52-week high level of $7.575. The stock gave a positive return of ~7% over a period of 1 year. In FY19, the company’s actual EBITDA on a comparable basis stood above the top end of the guidance range. Net margin of the company stood at 7.1% in FY19 as compared to the industry median of 6.3%. This reflects that the company possesses decent capabilities to convert its top-line into bottom-line as compared to the broader industry. Return on equity of the company stood at 6.1% in FY19 versus the industry median of 5.7%. The stock is available at a price to book multiple of 2.4x as compared to the industry median (Telecommunications Services) of 3.0x on TTM basis. Thus, considering the above-mentioned factors, we maintain a “Hold” rating on the stock at the current market price of $7.170 per share, down by 4.144% on 3rd February 2020.

amaysim Australia Limited

Change in Director’s Interest: amaysim Australia Limited (ASX: AYS) is engaged in providing mobile services in Australia and has a market capitalisation of $100.34 Mn as on 3rd February 2020. The company recently announced thatMr Peter O’Connell,Chief Executive Officer and Managing Director of the company, has ceased to hold an indirect interest in 500,000 fully paid ordinary shares, subsequent to a Family Law Consent Order in relation to property settlement procedures.

FY19 Key Financial Highlights: During the year ended 30th June 2019, the company generated net revenue of $508.3 million as per new GAAP, down 7.8% on pcp. Underlying EBITDA for the period came in at $47.3 million as per new GAAP, down 14.5% on a year over year basis.

FY19 Financial Metrics (Source: Company Reports)

Financial Guidance: FY20 underlying EBITDA is expected to be in the range of $33 million - $39 million, on a New GAAP basis.

Valuation Methodology: P/BV Multiple Approach

P/B Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading below the average of its 52-week high-low level of $0.900 and $0.285, respectively.Going forward, the company is well funded to capitalise on its growth opportunities. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., Price to Book multiple and arrived at a target price offering lower double-digit upside (in % terms). Hence, looking at the current trading levels and business prospects, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.32, down 5.882% as on 3rd February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...