Stocks’ Details

Dimerix Limited

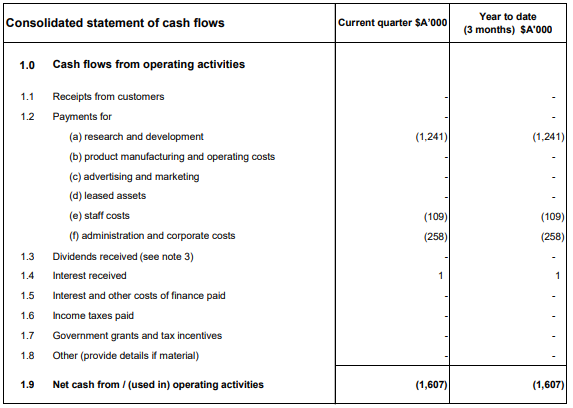

Capital Raising Through Placement:Dimerix Limited (ASX: DXB) is a clinical-stage biotechnology business, commercialising new therapies for under-served and unmet medical needs globally. The market capitalisation of the company stood at A$24.51 Mn as on 10th December 2019. The company recently announced the placement of 22.7 Mn fully paid ordinary shares to sophisticated and institutional investors at a price of $0.11 per share. The company will raise $2.5 million (before costs) through the placement. The company will utilise the fund to progress DMX-700 for Chronic Obstructive Pulmonary Disease towards in vivo proof-of-concept. The company would also utilise the funding towards the initial studies into additional pipeline candidates, general working capital purpose and corporate costs. As at 30th September 2019, the cash balance of the company stood at $1.99 million.

Cash Flow Statement (Source: Company Reports)

Expectation of Initial Data:With respect to DMX-200 clinical trials, the company is currently expecting initial data from both trials in mid-2020. The company continues to engage with potential licensing partners as it progresses, with the target to provide the best result for the patients and its shareholders.

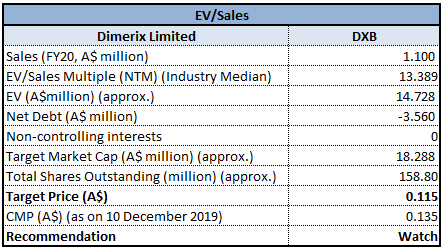

Valuation Methodology: EV to Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The company expects FY20 to be the peak year of adjustments. As per the ASX, the stock is trading near its 52-week high. We have valued the stock using EV/Sales multiple approach which depicts that the stock might witness correction in the upcoming period. Thus, considering the valuations and current trading levels, we have a wait and watch stance on the stock at the current market price of A$0.135 per share as on 10 December 2019.

Healius Limited

Favourable Decision of Court:Healius Limited (ASX: HLS) is involved into activities such as pathology, medical centres and imaging with three emerging businesses- dental, IVF and day hospitals. The market capitalisation of the company stood at ~A$1.81 Bn as on 10th December 2019. HLS recently announced that the Federal Court of Australia provided a decision in favour of the company, which was related to the tax treatment of healthcare practitioners lump sum payments.

Previously, the company was advised in 2015 that lump sum payments made by it to the healthcare practitioners for financial years 2010 to 2014 were tax deductible. It subsequently filed an application for the similar tax deductions for financial years 2003 to 2007, which was subject to Commissioner of Taxation’s discretion in allowing HLS to lodge an out-of-time objection. Following the Commissioner’s decision not to allow the objection, the company started legal proceedings. The favourable decision remains subject to Commissioner’s right of appeal to the Full Court of the Federal Court of Australia. The company can pursue a refund of tax payments and associated interest, subject to any such appeal.

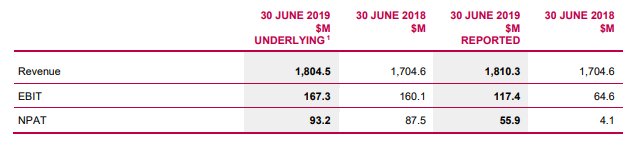

The refund was initially estimated at $60 million, as disclosed on 9th June 2015. The following picture provides an overview of financial results for the year ended 30th June 2019:

Financial Results (Source: Company Reports)

Expectation of Rise in Underlying NPAT:Subject to any unforeseen circumstances and before any impact from the implementation of AASB 16, the company is expecting underlying NPAT for FY 2020 in the range of $94 million and $102 million.The company also added that at the top end of the range, UNPAT equates to a rise of 9.4%, which in line with the seasonally adjusted run-rate from 2H FY19.

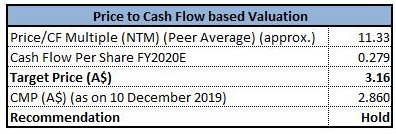

Valuation Methodology: Price to Cash Flow Multiple Approach

Price to Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The company reported a rise of 13% to $327 million in revenue in its Medical Centres division, reflecting the beginning of a turnaround in Medical Centres, backed by a strong contribution from Dental, and Health & Co making its maiden profit. The Board of the company declared a final dividend amounting to 3.4 cps, which reflected a payout ratio of 60% of the reported profit and 40% of the underlying profit. We have valued the stock by using relative valuation method, i.e., P/CF multiple approach and arrived at a target price of lower double-digit upside (in percentage terms). Thus, considering the company’s focus on managing the levels of debt and strive to balance an optimal gearing ratio with capital needs and dividends and valuations, we maintain a “Hold” rating on the stock at the current market price of A$2.860 per share, down 1.379% on 10th December 2019.

Starpharma Holdings Limited

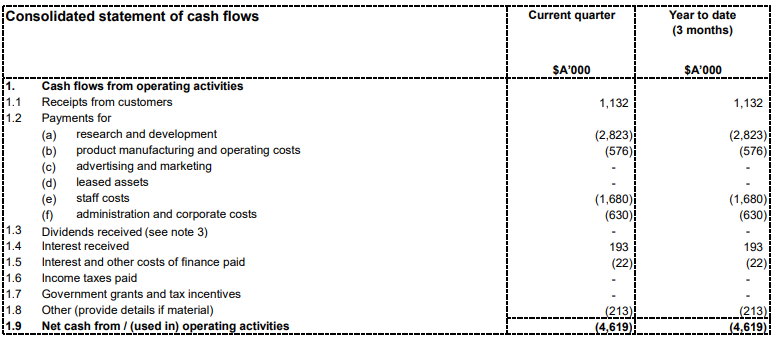

Completion of Phase 1 Component of its Phase 1 / 2 Trial: Starpharma Holdings Limited (ASX: SPL) is involved in research, development and commercialisation of dendrimer products for a pharmaceutical, life-science and other applications and has a market capitalisation of ~A$456.29 Mn as on 10th December 2019. Recently, the company announced that it has successfully completed phase 1 component of its phase 1 / 2 trial for DEP® cabazitaxel. The trial met its objective of evaluating the safety, tolerability as well as preliminary efficacy data, and identifying a recommended phase 2 dose of 20 mg/m2. During Q1FY20, the company reported net operating cash outflows of $4.6 Mn.

Cash Flow Statement (Source: Company Reports)

Outlook:Strong balance sheet and anticipated growing revenues place the company in an excellent position for growth to leverage its expertise, human capital and intellectual property portfolio in order to drive success and to increase the shareholders’ value.

Stock Recommendation:As at 30th September 2019, the cash balance of the company stood at $36.8 million. In addition, the cash balance does not include the expected $4.9 million R&D tax incentive, which is anticipated to be received during the December quarter. Current ratio of the company stood at 7.44x in FY19 as compared to the industry median of 1.79x, which reflects that the company is in a decent position to address its short-term obligations against the broader industry. Gross margin stood at 90.8% in FY19, higher than the industry median of 66.7%. The stock provided a return of 10.36% in the span of three months and 15.57% on YTD basis. Therefore, in light of decent liquidity position, outlook, and current trading levels, we give a “Hold” recommendation on the stock at the current market price of A$1.295 per share, up 5.714% on 10th December 2019, taking cues from the successful completion of the trial.

Cann Global Limited

Announcement of Agreement: Cann Global Limited (ASX: CGB) is engaged in legally developing, growing, cultivating as well as producing hemp and medicinal cannabis products. The market capitalisation of the company stood at A$47.43 Mn as on 10th December 2019. The company recently announced an agreement to secure the exclusive rights to the IP of the unique medicinal cannabis formulations, which have been used by Olivia Newton John in her recent health challenge.

The deal between CGB and John Easterling happens to be a cash-free deal and is subject to the shareholder and any other regulatory approvals that may be required, and based upon the stock-for-stock exchange agreement by and among Cann Global, Plant Matrix Research Pty Ltd which is the company that John has set up in Australia that owns the IP, and Botanical Science Pty Ltd an Australian company controlled by John Easterling which is 100% owner of PMRPL as a trustee of a trust controlled by John Easterling, set up for purposes of Cannabinoid Formula Research and Development. The following picture gives an idea of quarterly consolidated revenue:

.png)

Quarterly Consolidated Revenue (Source: Company Reports)

Positive for Short-Term Outlook: As per the Annual Report 2019, the company is optimistic about the short-term market outlook with its new Food product range, International partnerships, Asian Food Distributorship deals and its upcoming release of Pharmocann Nutraceuticals.

Stock Recommendation:CGB and Management have all the right assets and capability and is well placed to continue to deliver and increase the shareholders’ value in the coming times. The stock has EV to sales multiple of 43.3x in comparison to the industry median (Healthcare) of 8.3x on TTM basis. As per ASX, the stock of CGB is trading close to its 52-week low. Considering the aforesaid facts and stretched valuations, we have a wait and watch stance on the stock at the current market price of $0.016 per share, up 6.667% on 10th December 2019, owing to the announcement of the agreement to secure the exclusive rights to the IP of the unique medicinal cannabis formulations.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...