CSL Limited (ASX: CSL)

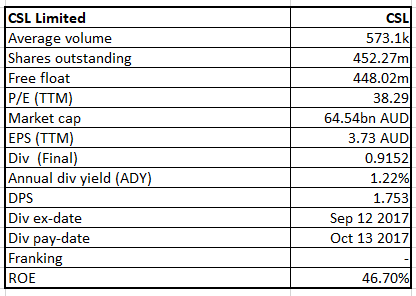

CSL Details

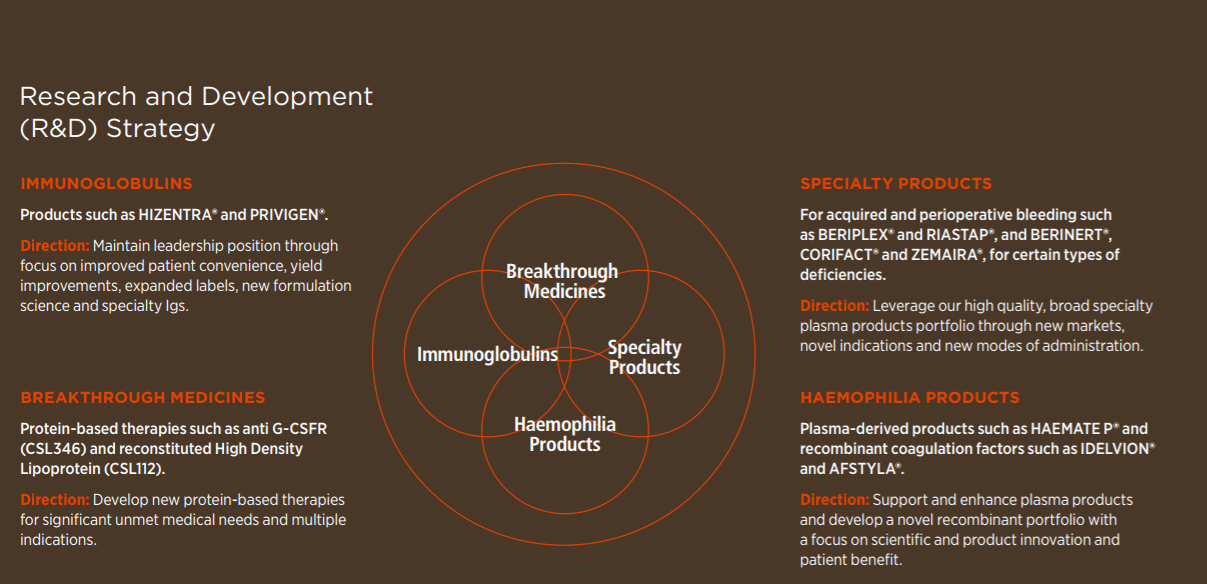

Continues to Invest in Research & Development: Late last year, CSL flagged the return of former CEO Brian McNamee as its chairman who got elected after four years. He promised that CSL is going to be a market leader soon with good operating conditions. The group is also making other changes to its board with appointment of new directors. Further, the group has confirmed to spend 10-11% of its global revenue on research and development. Global R&D activities also support CSL’s existing licensed products and development of new therapies to help aligning the technical and commercial capabilities in immunoglobulins and other speciality products. Meanwhile, CSL reported US$1,337 million as its NPAT for the year ended 30 June 2017 and its revenue was up by 15% on constant currency basis. It launched three new influenza products in US, namely Flaud, Flucelvax Quadrivalent and Afluria Quadrivalent. It is the most efficient and highest quality plasma player that has opened a total of 29 new plasma collection centres. CSL Behring’s portfolio of albumin products yielded sales of US $840 million which is an increase of 7% at a constant currency which was primarily driven by a strong and an ongoing global demand.

The group expects to have about 25 plasma centres to be opened in FY18 and this would boost immunoglobulins’ volume-based growth. The group’s progress is also dependent on the regulatory approval for Hizentra. On the other hand, growth in albumin for past 12-month period has been on the swing.

Research and Development Strategy (Source: Company Reports)

In addition to the acquisition of Seqirus immunohaematology, the Company also entered the final stages on the small to medium acquisitions which are likely to be finalised over the coming months. Meanwhile, CSL is setting itself high with products such as CSL112 to address the unmet medical need with commercial strategy already planned. So due to the demand for its immunoglobulin and speciality products, its Seqirus influenza business is expected to become profitable and CSL is expected to deliver above-average earning growth for the next decade. While the potential can be looked through, the stock is peaking close to 52-week high level and we believe that the stock is still “Expensive” at the current price of $141.90

.png)

CSL Daily Chart (Source: Thomson Reuters)

Cochlear Limited (ASX: COH)

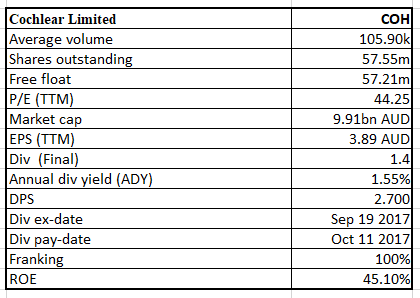

COH Details

Customer Focus: Cochlear is currently trying to penetrate the senior market targeting people affected by hearing loss, however, challenges with respect to awareness, limited capacity and manufacturing constraints do exist. The group is aiming to manage the shortcomings with the processor upgrade with an effort to boost investment to support the upgrade. Recently, Mr Diggory Howitt was appointed as the Managing Director of the company. Meanwhile, COH had reported a net profit of $224 million for FY17, which is an increase of 18% on FY16. In FY17, it invested over $150 million in R&D which represented 12% of its revenue. The balance sheet and free cash flow generation remained strong and supported the 17% increase in the fully franked final dividend to $1.40 per share which takes dividend paid for the full year to $2.70 per share, fully franked which is an increase of 16% on FY16. During the year, it had launched a new product which included Kanso Sound Processor, which is its first off-the year sound processor, and another is the Nucleus Profile Slim Modiolar electrode which is the world’s slimmest electrode.

.png)

Nucleus 7 Smart Application (Source: Company Reports)

The group has continued to lead the market with innovative new initiatives that improved the quality of the life. It also expanded its global manufacturing capacity for cochlear implants with a new $50 million facility to be built in Chengdu, Sichuan Province, China and the products produced from this expanded facility will be for China and other emerging markets’ businesses. In FY18, it expects a net profit to increase to $240-250 million and it also expects the launch of the Nucleus 7 Sound Processor which will contribute to both implant growth and will upgrade demand over the coming years. The stock price has increased by 13.8% in the past six months (as at January 08, 2018) and looks “Overvalued” at the current price of $173.50, looking at the expected upside.

.png)

COH Daily Chart (Source: Thomson Reuters)

Ramsay Health Care Limited (ASX: RHC)

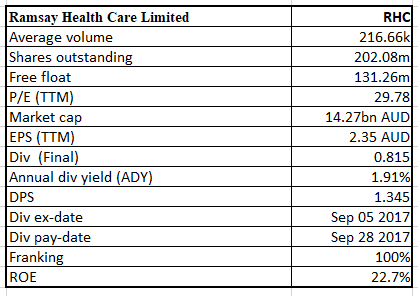

RHC Details

Ongoing Improvement: Ramsay Health Care that has a better return on equity than the industry median with steady earnings retention over the years, operates 235 hospitals, day surgery centres, treatment facilities, rehabilitation and psychiatric units and a nursing college across six countries. During 2017, it delivered a strong revenue and EBIT growth and its international business performed well. Its net profit attributable to the owners of the parent for the year ended 30 June 2017 was $488.95 million which is an increase of 8.6% as compared to the previous year and diluted earnings per share were 234.9 cents as on 30 Jun 2017, which was an increase of 8.7% on prior year. Ramsay’s Australian and Asian business achieved a revenue growth of 7%to $4.7 billion and EBIT growth of 13.9%. Its total assets increased by 1.1% mainly due to increase in working capital and total liabilities decreased by 3.5%, mainly due to reduction in interest bearing loans and borrowings. Major expansions areunderway and include St Andrew’s Private Hospital in Ipswich, Albert Road Clinic in Melbourne, Warners Bay Private Hospital in Newcastle and the new Northside Clinic in Sydney. In France, RHC launched the first digital admission process for patients. It remains committed to its focussed strategy of organic growth, financially disciplined acquisitions and expansion of its existing business through brownfield developments. The group also has the potential for out-of-hospital growth opportunities in its adjacent businesses like retail pharmacy across all the markets in which it operates. Meanwhile, RHC stock has risen 11.7% in three months as on January 08, 2018. Given the potential, boost from private insurance reforms, and macro industry trends, the group seems to be well placed to meet EPS growth target of 8% to 10% in FY18 with continued margin expansion; and we put a “Buy” recommendation on the stock at the current price of $70.50

.png)

RHC Daily Chart (Source: Thomson Reuters)

Medical Developments International Limited (ASX: MVP)

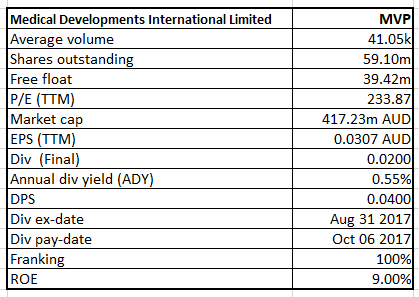

MVP Details

Positive Outlook: Last year, Medical Developments was under scrutiny when market raised few concerns on the group based on sale of 4.35 million of MVP shares by Mr David Williams to 9 global and local financial institutions in the United Kingdom, the United States of America, Hong Kong and Australia in an off-market transaction. The market otherwise noted a significant demand from a large number of leading financial institutions around the world. MVP has been gradually gaining momentum in terms of its ambition to become a global pharmaceutical and a medical device company. MVP’s Penthrox (pain relief product) has also been approved for use in Mexico, Belgium, South Africa and Singapore. Investors have been positive on approvals sought in each of the 28 EU member States as well as in other countries. Lately, Penthrox has been approved in 22 European countries. The only thing which differentiated MVP is that it has not raised or waisted huge amount of capital rather it has used the resources and spent the available money on building the science, markets and its staff. Sales and its operating performance have been mainly in line with the budget and it also expects H1FY18 results to be in line with H1FY17. MVP’s Scoresby manufacturing facility is complete and is expected to be fully operational by the end of 2017. Its long-term ambition is to gather sufficient clinical and safety data so that Penthrox can come in use into post-operative breakthrough pain, breakthrough cancer pain and other home use. Trading at extremely high levels while return on equity is lower than industry average, we give an “Expensive” recommendation on the stock at the current price of $ $7.40

MVP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...