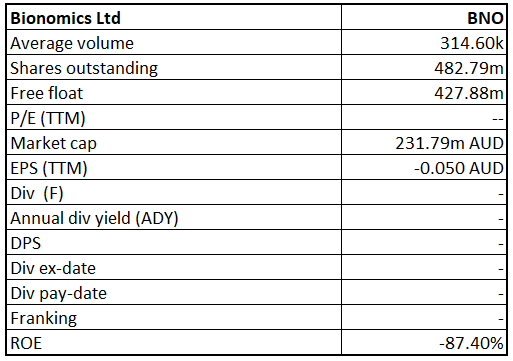

Bionomics Limited

BNO Details

Clinical Trial Pipeline: Bionomics Limited (ASX: BNO) reported full-year 2018 results with revenue and other income of $12,456.446, a drop of 55.91% from the prior corresponding period. The current year loss from ordinary activity after tax attributable to members increased by 258.71% to $24,583,423 million. BNO took a hit on its revenue and profits in the absence of any licensing income, unlike the FY2017 where the company earned $13,073,615 in revenue from licensing. As of now, the company continues to focus on cost efficiency in supportive activities and conserving cash for R&D activity which will support to enhance bottom-line in years to come. In relation to this, the company has reduced its administrative, compliance and occupancy rate by 18% in FY18 against the prior year. The group has completed the Phase 2 clinical trial to assess the safety and efficacy of BNC210 for the treatment of PTSD. Completion within the set deadline exhibits BNO’s capability to conduct and complete the large, multi-center clinical trials in the neuroscience space. Further, BNC210 has been effective in seven clinical trials to address the Panic attack symptoms and Generalized Anxiety Disorder. Then collaboration between Bionomics and MSD continues with the focus on addressing the cognitive dysfunction in Alzheimer disease and CNS indications. We expect that the company is set to make progress on the BNC210 and a strong pipeline of preclinical programs and is in the process of monetizing its oncology program which would add value for the shareholders, going ahead.

Stock Performance: Meanwhile, the stock has been in a downward spiral since 2013 until the trend seemed reversed in 2016. Price did not break the crucial support level of $0.23 and rebounded. With major strength indicator not showing any significant weakness in the stock post the result, we maintain our “Speculative Buy” recommendation on the stock at the current low levels of $ 0.460, down by 4 per cent on August 30, 2018.

BNO Daily Chart (Source: Thomson Reuters)

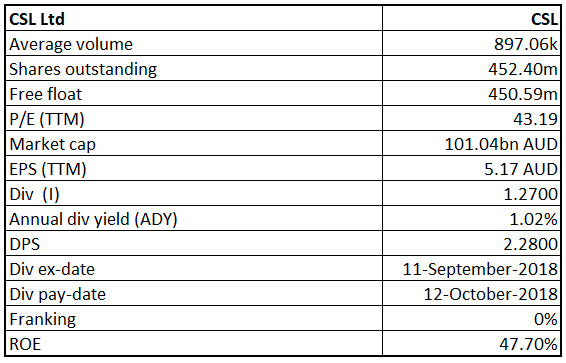

CSL Limited

CSL Details

New and existing products support financials: CSL Limited (ASX: CSL)posted an increase of 11% in the revenue at US$ 7,915 million and 28% increase in profit at US$1,729 million for FY18. Earnings per share also came in higher at $3.82 per share compared to $2.94 per share in FY17. Major revenue drivers were new products, growth in the existing products, expansion of FLUAD manufacturing. Net Profit after tax and Earnings per share witnessed consistent growth over the past five years.

Besides this, the strong demand for company’s recombinant and plasma products is expected to go ahead in FY 2019. As a result, the group expects an increase of 9% in the revenue for FY 2019 and NPAT to increase between 10% and 14% of the FY18 number. The company has posted good results and upbeat guidance for the upcoming year. However, at the current juncture, the stock looks expensive, if the recent offloading of the shares by CEO Paul Perreault is any hint. CEO Perreault has sold over $20.4 million worth of shares of the company.

.png)

NPAT/EPS Growth (Source: Company Report)

Stock Performance: The stock had a great run up over past many years generating a return of around 233% over the past five years. However, after giving a breakout from the $204 – $205 levels the stock has rallied too far, and a correction may look imminent. Relative strength indicator has entered in the overbought zone suggesting an expensive level of the stock. Based on foregoing, we maintain an “Expensive” rating on the stock at the current price of $226.3.

CSL Daily Chart (Source: Thomson Reuters)

Nanosonics Limited

.png)

NAN Details

Trophon 2 upcoming release impacted profits: Nanosonics Limited (ASX: NAN) posted revenue at $60.7 million, a drop of 10% from FY17. Profit after tax was down 79% at $5.8 million compared to the $26.2 million in FY17. Revenue and subsequent numbers were impacted by the drop in capital revenue related to the earlier than estimated regulatory approval of Trophon 2. Some of the clients of the company also deferred the purchase of the Trophon EPR, until the release of the new model. In the United States, Trophon EPR continues to increase its base, growing from 12,400 units to 15,620 units. Trophon has now been installed in around 5,000 hospitals and clinics. Customers waiting for Trophon 2 to release indicate that the fundamentals for adoption continue to be strong. In Europe too, the adoption of Trophon increased by 49% during the same period. Going forward, the company’s distribution agreement with GE healthcare in the United States would positively impact the Capital Reseller model, thereby increasing sales and margin from consumables in North America.

Stock Performance: The stock has had a stellar run after giving breakout from the level of $2.85 in June this year. Price has already corrected from the higher levels of $3.8 taking support at around $3.5 levels. Based on the technical indicators, there is no sign of trend reversals and healthy corrections present an opportunity for the investors to accumulate or take a fresh position in the stock. We maintain "Hold" rating on the stock at the current market price of $3.570.

NAN Daily Chart (Source: Thomson Reuters)

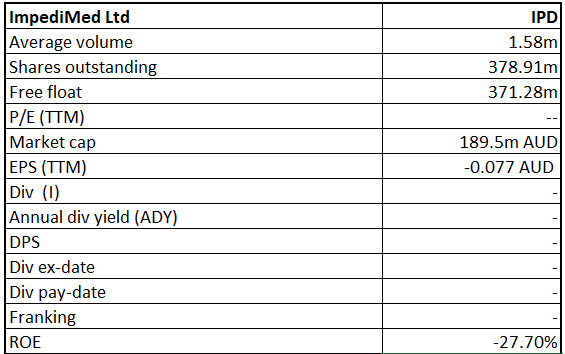

ImpediMed Limited

IPD Details

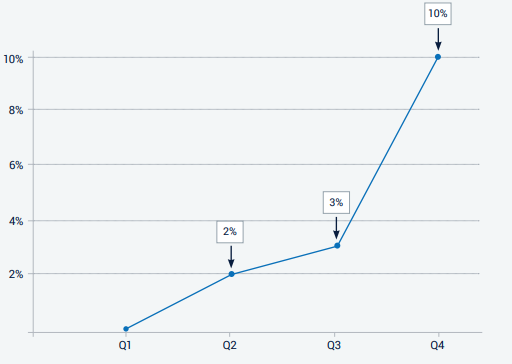

SOZO continues to drive growth: ImpediMed Limited (ASX: IPD) reported net loss of $27.1 million in FY18 compared to $27.5 Mn in FY17. Loss has decreased in the FY18 primarily due to R&D project cost related to the completion of the SOZO 1 Hardware (SOZO comes under a bio-impedance device). In the second quarter of FY2018, the company rolled out SOZO subscription model in aggregation with the launch of SOZO Digital Health platform. Growth in subscription business model has been consistent over the quarters. Further, SOZO recurring revenue have also increased Quarter over Quarter as a percentage of total medical revenue.

SOZO Recurring Revenue (Source: Company Report)

On the other hand, the company provided the first insight into its PREVENT trial suggesting that L-Dex is quite sensitive in assessing the sub-clinical lymphoedema in patients with a history of breast cancer. Meanwhile, the stock has generated YTD return of -51.69%.

Stock Performance: Among the indicators, the stock has turned from the overbought zone suggesting that the much-needed correction has already come at the price. The stock is holding its support level of $0.45 and thus, we maintain ‘Hold’ rating on the stock at the current price of $ 0.500, expecting that the SOZO subscription model and the strong pipeline would help the stock grow.

IPD Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...