Wellard Ltd

WLD Details

First shipment of beef cattle to China: Wellard Limited (ASX: WLD) has witnessed a stock price surge of 24.14% on September 20, 2017, as the group recently announced that it has agreed on commercial terms for the company’s historic first shipment of beef cattle to China. Approximately 2000 cattle will be loaded for the shipment from south east Australia and the cattle are being supplied to Rongcheng HCMH Trade and Service Co., Ltd, a subsidiary of Tai Xiang Group, which is an established Chinese company specialising in frozen and processed food. The shipment, despite being relatively small, is the largest to date and represents a very significant step in the Company’s implementation of its strategy for China. Moreover, the company sees this as the start of a long-term relationship with clients in China, like the customers in other markets for the last three decades, including establishing ESCAS supply chain integrity with a special emphasis on animal welfare. China offers big potential for Wellard and the Australian cattle industry in general, and this first shipment will pave the way for the development of a more regular trade. The cattle will be quarantined and then processed in a purpose-built facility in China, which has been ESCAS (Exporter Supply Chain Assurance Scheme) accredited.

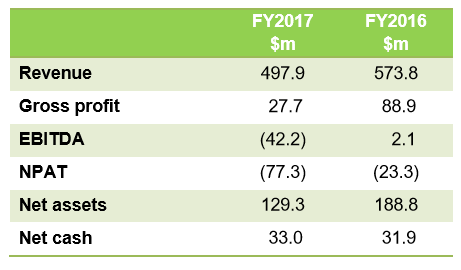

FY17 Result (Source: Company Reports)

The stock has declined 39.6% in the past six months while it is down 49% in the last one year (as at September 19, 2017) at the back of the lower than expected FY17 result wherein the group reported net loss after tax of $77.3 million while the cash position improved owing to capital raising. WLD is the largest exporter of cattle from Australia and its performance is thus sensitive to cattle prices and foreign exchange rates. Given the above in view of recent development, we put a “Speculative Buy” recommendation on the stock at the current price of $ 0.18

.PNG)

WLD Daily Chart (Source: Thomson Reuters)

Australian Agricultural Company Ltd

.JPG)

AAC Details

Improvement in net operating cash flow:Australian Agricultural Company Ltd (ASX: AAC) seems to be progressing well in terms of continuing with the gains of its past four years in FY18. The group had reported a revenue of $446.7 million in FY17 against $489.4 million in FY16 while operating EBITDA (earnings before interest, tax, depreciation and amortization) grew by 202% year on year (yoy) to $45.0 million, and statutory EBITDA stood at $133.2 million. Notably, EBITDA margin improved by 700bps to 10% compared to 3% in FY16, and net operating cash flow increased by $7.5 million to $29.3 million. Further, 27% decrease in cost of production per kg was driven by improved supply chain management, increased focus on internal supply and favourable seasonal conditions. Going forward, the group expects growth from various drivers including its luxury brands in Taiwan.

The stock declined 22.5% in the past three months while it is down 10.0% in the last one year (as at September 19, 2017) owing to volatile conditions. There was also some impact on the stock from the news encircling sudden resignation of its managing director and CEO Jason Strong. However, given the benefits from the on-going efficiency improvement measures and improving outlook for FY18,we maintain a “Buy” recommendation on the stock at the current price of $ 1.56

.PNG)

AAC Daily Chart (Source: Thomson Reuters)

Capilano Honey Ltd

.JPG)

CZZ Details

Improvement in honey stocks: Capilano Honey Ltd (ASX: CZZ), Australia’s leading packer and marketer of honey, is known to actively acquire complementary businesses and brands for better prospects; and expects growth from increasing consumer interest in health and wellness, and improving economic growth. The group has also increased its supplier base and is focusing on producing more premium products in the future. For FY17, CZZ reported a subdued revenue profile ($133.1 million), while posting 9% yoy growth in net profit at $10.3 million. Earnings before interest and tax was up slightly to $14.1 million. The drop-in sales were led by unfavourable impact of changes to net pricing with a key customer as it reduced revenue by ~$3.4 million. On the other hand, FY17 was a year of consolidation for the company delivering a strong balance sheet with lower debt. In July 2016, a capital gain of $2.1 million was realised following the sale of bee keeping assets to its new joint venture operation with Comvita Limited. However, it was offset by an unfavourable raw honey stock revaluation of $133 million in December 2016, triggered by a change in honey price. In addition, the company has incurred a significant increase in the marketing spend for the Beeotic prebiotic honey product launch while the closing financial year (FY) honey stocks have improved again from the lows of 4,960 tonnes in FY16 to 5,953 tonnes in FY17. We give a “Speculative Buy” recommendation on the stock at the current market price of $ 15.95

.PNG)

CZZ Daily Chart (Source: Thomson Reuters)

Costa Group Holdings Ltd

.JPG)

CGC Details

Berry growth witnessed super performance:Costa Group Holdings Ltd (ASX: CGC) has undertaken many growth initiatives for FY18, and these include Monarto mushroom farm expansion, execution of domestic berry growth program and development of avocado fifth pillar with Lankester farm acquisition. For FY17, CGC reported 10.7% (year on year) revenue growth at $909.1m, while posting 29.4% growth in EBITDA at $115.2m (before SGARA and material items). NPAT before SGARA and material items increased by 37.3% to $60.7m while statutory NPAT increased to $57.7m, compared to $25.3m in FY2016. The produce segment delivered a solid result by growing at 9.4% to $786.2 million with total transacted sales of more than $1 billion, while CF&L revenue growth was up 2.4% on FY2016. During the year, domestic and international berry growth, excellent citrus performance and recovery in the tomato market contributed to year on year earnings growth. Berry category growth remains high with a 55% increase in blueberry production on FY2016, for which the Corindi New South Wales farm accounted for a significant portion of the increase. Notably, the Coles Jandakot Western Australia Distribution Centre contract was renewed through to September 2023. CGC will hold its Annual General Meeting in November 2017.

.png)

Australian Berry Expansion (Source: Company Reports)

The stock has moved up 75% in the last one year while it is up 21.9% in the past six months (as on September 19, 2017), owing to sustained financial performance and increasing demand for the company’s food products. Given the on-going momentum, we maintain a “Hold” recommendation on the stock at the current market price of $ 5.33

.PNG)

CGC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...