Costa Group Holdings Limited (ASX: CGC)

.png)

CGC Details

Expansion Strategy to meet the rising demand - Costa is Australia’s leading grower, packer and marketer of premium quality fresh fruit and vegetables. Food is a very essential service for the group and it provides food almost all year round to its major supermarket customers. As population is increasing so will demand of food. Costa’s half-year revenue was up by 9.8 per cent for the period ended December 31, 2017 and amounted to $489.3 million against $445.5 million of the prior corresponding period. It is expanding its business in China with small volume of blueberries that are harvested from its farms leading into December and the main harvest was expected around Mar-May that in line with its expectations.

.png)

Growth Initiatives (Source: Company Reports)

Costa is working towards its growth strategy by investing in farms in different regions globally so that it can supply its produce over longer periods of time. The Group has planned an extension of R&D breeding program into Morocco to enable future selection of varieties bred specifically for Morocco. Further, the Group is projecting NPAT (pre-SGARA and material items) growth of approximately 25 per cent for FY18, up from previous guidance of at least 20 per cent. The full-year earnings will be more heavily weighted to the second half due to the timing of the avocado harvests and further growth of the international operations including the increased African Blue shareholding. Meanwhile, the stock was up by 76.07 per cent in the past one year and by 14.49 per cent in the last one month. The stock slipped by 1.16 per cent as on 26 June 2018. Lately, Commonwealth Bank of Australia became a substantial holder of the group. We continue with our “Hold” recommendation at the current market price of $8.51 as the Group is taking continuous initiatives towards its growth strategy.

.png)

CGC Daily Chart (Source: Thomson Reuters)

Collins Foods Limited (ASX: CKF)

.png)

CKF Details

An improvement in the underlying financial metrics- Collins Foods released its results for thefinancial year ended 29 April 2018 (FY18). It has continued to grow its KFC Australia business through organic underlying growth, and acquisitions which have expanded its Australian footprint and has consolidated its position as the largest KFC operator in Australia. The Group completed the acquisition of 25 restaurants during the financial year while continuing to drive same-store sales growth across the network. The EBITDA from the KFC Australia network was up by 10.5 per cent to $99.3 million and EBITDA margins were contracted slightly to 15.9 per cent (FY17: 16.4 per cent) due to promotional activity that generated a small shift in product mix due to the impact of some sales deleverage, principally in WA. After purchasing 28 KFC Australia restaurants and 16 KFC Netherlands restaurants, net debt increased $94.1 million to $227.2 million with a net leverage ratio of 2.14 (FY17: 1.59). Collins recorded an increase of 21.7 per cent in revenue ($770.9 million) which was driven due to like-for-like sales growth, new restaurant openings and the acquisition of KFC restaurants. Revenue in Sizzler business was a drag as the same was down by 22 per cent on the prior corresponding period to $50.8 million, driven by the closure of two restaurants in Australia.

.png)

Financial Results Summary (Source: Company Reports)

The Board will focus on its growth priorities in FY19 like in Australia it has planned to drive transaction led sales growth and has built eight further KFC restaurants. The Board kept the dividend same for FY18 as it declared in FY17 that is 9.0 cents (fully franked final dividend) and this will be paid on 26 July 2018. On the other hand, the Group faces few risks from the health and safety perspective while growing population and various public events can turn favourable. Nonetheless, the stock climbed up by 2.75 per cent after the Group released its financial results as on 26 June 2018. We recommend to “Buy” the stock at the current market price of $5.6 by looking at the positive financial results that will help Collins to achieve its FY19 priorities.

.png)

CKF Daily Chart (Source: Thomson Reuters)

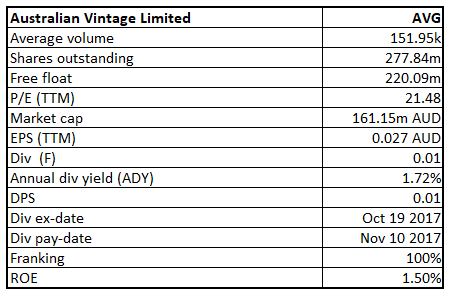

Australian Vintage Limited (ASX: AVG)

AVG Details

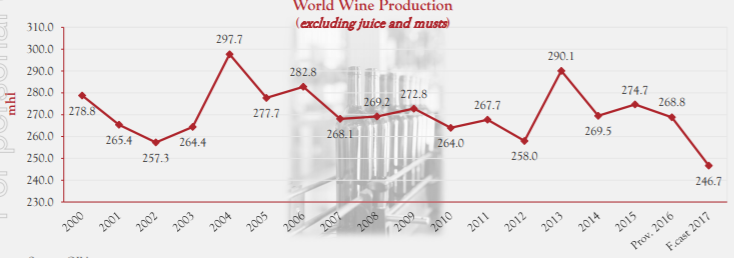

An improvement in Sales Performance - Australian Vintage Ltd is one of the largest wine producers in Australia. The Group recently reported that it crushed 93,000 tonnes of grapes from the 2018 Vintage which was in line with tonnes crushed last year. While the actual amount crushed for its own use declined by 2,500 when compared to last year which was offset by 2,500 tonnes increase in third-party contract processing. AVG’s owned, and leased vineyard yields were down by 7 per cent on expectation. The total sales to the end of April 2018 were 20 per cent above last year due to increased sales of its 3 key brands, McGuigan, Tempus Two and Nepenthe. It was worth noting that the 2018 Australian wine industry crush is estimated to be around 10 per cent down on the big 2017 crush and indicates that the quality again will be very high.

Trend of World Wine Production (Source: Company Reports)

Though the lower yields from its owned and leased vineyards means that its income from vineyards (SGARA) will be down on last year but the management is confident enough that it will achieve its forecasted profit. The Group’s decision to expand its sales team in UK was now providing benefits like the sales of its UK/ Europe segment showed a significant growth of 25 per cent and sales volumes were up by 11 per cent to the end of April 2018. The Company expects that it will generate Net Profit after tax between $7.0 million and $7.5 million in FY18. It focuses on increasing branded sales and at the same time improving the efficiency of the business by improving the quality of its outstanding wines. The stock prices were up by 30.34 in one year but started falling since last three months. We give a “Hold” recommendation at the current market price of $0.575 as the Group is placing the strategies well so that it becomes a leading global branded wine company.

AVG Daily Chart (Source: Thomson Reuters)

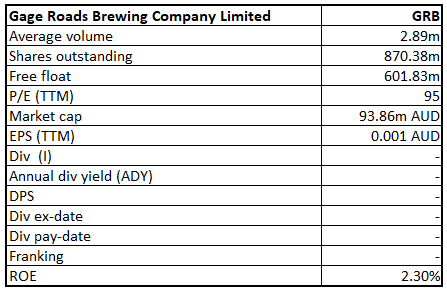

Gage Roads Brewing Co. Limited (ASX: GRB)

GRB Details

Well placed to deliver growth in earnings and sustained value - Gage Roads Brewing Co Limited is engaged in brewing, packaging, marketing and selling craft brewed beer, cider and other beverages.Recently, Pinnacle Investment Management Group Limited changed its substantial holding from 5.06 per cent to 6.65 per cent since 20 June 2018. Gage Roads will provide great choices to its fans so that they can enjoy while watching cricket at new home in St Kilda and this can be driven by the Group’s wide range of craft sales as well as a mid-strength and cider options. The Company issued 117,647,058 ordinary shares to institutional investors at $0.085 per share raising gross proceeds of $10 million pursuant to the placement that was first announced by the Company on 8 June 2018.

.png)

Proportion of the Sales Mix (Source: Company Reports)

It was made without shareholder approval in reliance on the Company’s 15 per cent annual placement capacity. The Company’s contract brewing division Australian Quality Beverages executed an extension to its exclusive contract brewing agreement with Matso’s Broome Brewery and this was in line with the Company’s long-term strategy to focus on high-quality and high-value products. Opportunities are being explored to continue to shift Gage Roads brands beyond 39 per cent of sales mix to drive margin growth. The stock jumped up by 3.158 per cent as on 26 June 2018. We give a “Hold” recommendation at the current market price of $0.098 by looking at the changing demands of Australian beer drinkers which have served the Group well and as it is expecting to meet its full-year sales target of at least 11 million Litres of underlying sales.

.png)

GRB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...