Stocks’ Details

Virgin Money UK PLC

VUK’s Share Surged ~24% Post Positive Outlook:Virgin Money UK PLC (ASX: VUK) serves more than 6 Mn customers across the UK through a digital first approach that offers leading online and mobile services, supported by telephone and branch banking, including a national network of branches and business banking centres. It was previously known as CYBG plc.

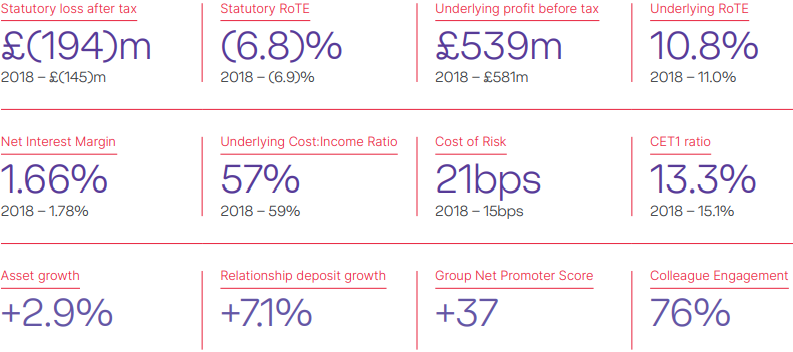

FY19 Key Highlights for the Period Ended June 30, 2019:Underlying profit decreased by 7% to £539 Mn, due to higher impairments from IFRS 9 adoption and normalisation. Statutory loss after tax for the period was reported at £194 Mn, due to legacy conduct costs and restructuring & acquisition costs.Strong growth in lending and deposits, in-line with its strategy, was underpinned by above market asset growth in Business (+4.5%) and Personal (+16%), and disciplined growth in Mortgages (+1.7%); good growth in lower-cost relationship deposits (+7%) across both Business and Personal business lines. The company reported Group NPS of +37 as compared to +34 in FY18. With B digital banking service, NPS was reported at +52.

The Board of Directors have suspended Dividend for FY19 considering additional PPI provisions, but expected to reconsider dividends for FY20 in-line with normal practice.

Key Business Metrics (Source: Company Reports)

What to Expect:As per the release, the first ever Virgin Money digital current account is ready to launch in December, built on its innovative FinTech-friendly digital platform. First three new concept Virgin Money stores are expected to open in December. New Digital Disruption Hub in Newcastle is expected to accelerate customer experience and digital functionality improvements from January 2020 in support of its target for Top 3 CMA service quality rankings. Moreover, VUK plans to launch unique personal rewards and loyalty programme leveraging the wider Virgin Group. A business banking proposition in 2020 is progressing well.

FY20 Guidance:NIM is expected to come in between 160-165bps. Underlying operating costs are expected to be less than GBP 900 Mn. CET1 ratio operating level has been anticipated to be around 13%. With CMD strategy on track, including modest improvement in NIM by FY22, operating costs for FY22 can be expected less than GBP 780 Mn and statutory RoTE are expected to be more than 12% by FY22.

Stock Recommendation:VUK’s share generated a negative YTD return of 17.48%. Its efficiency ratio for H1FY19 stood at 76.8%, lower than 114.5% in H1FY18. Its loan and deposit growth for H1FY19 stood at 132.7% and 113.8%, higher than 2.9% and 2.8% in H1FY18, respectively. Moreover, its EV/Sales and Price to Book Value multiples on NTM (Next Twelve Months) basis stand at 1.3x and 0.4x, lower than the industry median of 2.1x and 0.9x, indicating an undervalued position at the current juncture. Hence, considering the aforesaid facts and current trading levels, we recommend a “Hold” rating on the stock at the current market price of $3.350, up 24.533% on November 29, 2019, taking cues from the release of Annual Report 2019 & Pillar 3 Disclosures.

Bendigo And Adelaide Bank Limited

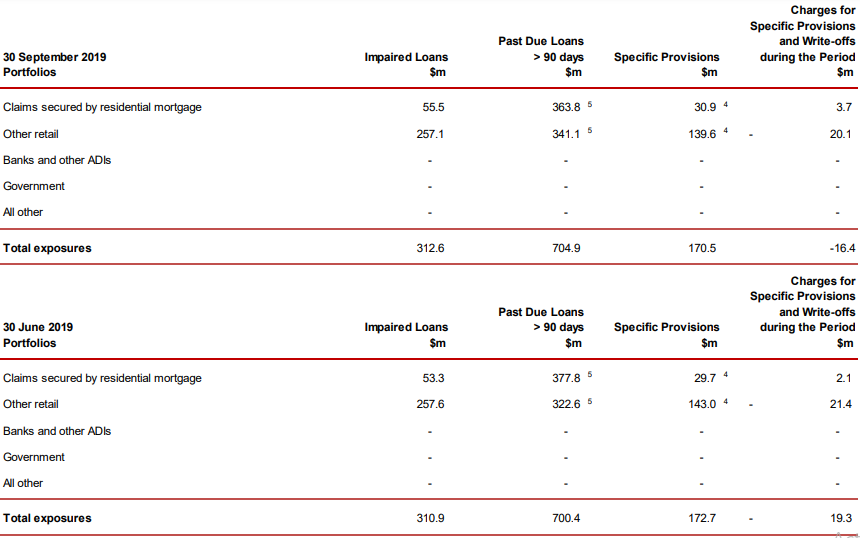

Update on Basel III Pillar 3 Disclosures to the Market:Bendigo and Adelaide Bank Limited (ASX: BEN) provides a broad range of banking and other financial services including consumer, residential, business, rural and commercial lending, deposit-taking, payments services, wealth management and superannuation, treasury and foreign exchange services. On November 26, 2019, the bank provided Basel III Pillar 3 Disclosures for the September quarter, to the market. Under Capital Adequacy, Claims secured by residential mortgage as on September 30, 2019, was reported at $16,906.7 Mn as compared to $16,777.6 Mn on June 30, 2019. Capital requirements for other retail were reported at $14,867.1 Mn on September 30, 2019 as compared to $15,066.7 Mn on June 30, 2019. Total risk-weighted assets were reported at $37,442.4 Mn on September 30, 2019 as compared to $37,483.1 Mn on June 30, 2019.

Capital ratio for common equity tier 1 as on September 30, 2019 was reported at 8.68% as compared to 8.92% on June 30, 2019. Under total exposures, loans exposure as on September 30, 2019 was reported at $60,065.0 Mn as compared to $59,874.3 Mn on June 30, 2019.

Key Metrics (Source: Company Reports)

What to Expect:As per the release, the bank is testing new concept stores to continue its commitment to build better customer experience. Its ‘smart’ retrofitted Norwood branch in South Australia has exceeded expectations with a 64% increase in foot traffic and a significant uplift in the business. It recently launched a second concept store in Leichardt, New South Wales and will soon open another in Victoria.

Stock Recommendation:At the current market price of $10.030, the stock is available at a price to earnings multiple of 13.200. BEN’s share has declined by ~5.65% in the last one year. Bank’s success of attracting new customers, especially in the younger demographic, gives it an opportunity to foster lifelong customer relationships. Moving forward, digitization of its offerings and focus on its priority markets provide clear competitive advantage to the Bank in delivering significant long-term growth opportunities. However, its efficiency ratio for FY19 stood at 62.2%, higher than the industry median of 53.5%. Hence, considering the company’s strategy for FY20, recent launch and current trading levels, we have a wait and watch view on the stock at the current market price of $10.030, down 1.473% on November 29, 2019.

Challenger Limited

CGF Declared Distribution Amount on Two of its Securities:Challenger Limited (ASX: CGF) is involved in two operating segments, i.e., Life and Funds Management. Both operating segments are supported by centralised operations, which are responsible for providing the necessary resources to meet regulatory, compliance, financial reporting, legal and risk management requirements. Recently, CGF ceased to be the substantial holder in AMA Group Limited, effective from November 26, 2019. In another update, CGF announced a distribution amount of AUD 0.7600 on security ‘CGFPA - CNV PREF 3-BBSW+3.40% PERP SUB NON-CUM RED T-05-20’, fully franked with record date and payment date on February 17, 2020 and February 25, 2020, respectively. For another security ‘CGFPB - CAP NOTE 3-BBSW+4.40% PERP NON-CUM RED T-05-23’, CGF announced distribution amount of AUD 0.9500 (fully franked) with record date and payment date on February 14, 2020 and February 24, 2020, respectively.

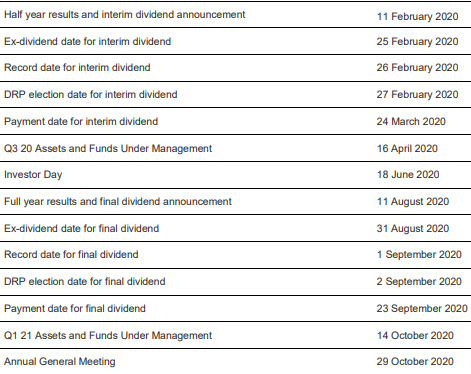

As per its 2020 financial calendar, half-yearly results and interim dividend announcement are expected on February 11, 2020. Announcement of Q3FY20 Assets and Funds Under Management are expected on April 16, 2020.

FY20 Financial Calendar (Source: Company Reports)

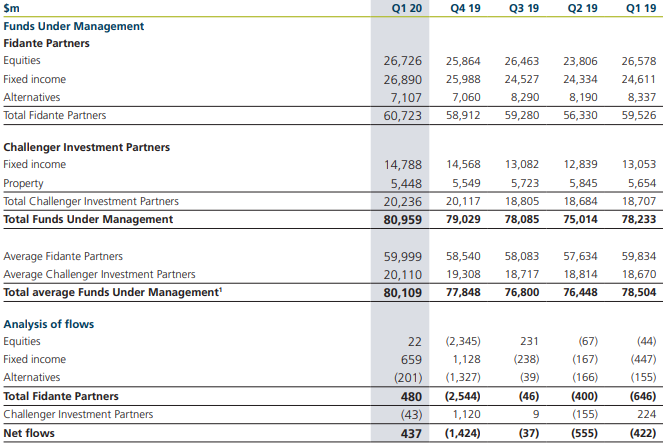

Q1FY20 Key Highlights for the period ended June 30, 2019:Total assets under management increased by 3% to $84 Bn (Q-o-Q). Life net book growth increased by 5.2% to $766 Mn (Q-o-Q). Total annuity sales increased by 14% to $842 Mn (Q-o-Q), wherein Australian annuity sales were reported at $624 Mn, a decline of 11% on Q4FY19, and Japanese annuity sales were reported as 26% of total annuity sales, an increase of $180 Mn on Q4FY19. Other Life sales for the period were reported at $936 Mn, an increase of $737 Mn on Q4FY19. Fund Management net flows for the period was reported at $437 Mn and funds under management increased by 2% for the quarter.

Quarterly Funds Under Management and Net Flows Data (Source: Company Reports)

What to expect:In FY20, normalised net profit before tax is expected to be in the range between $500 Mn and $550 Mn. Investment market conditions, including base interest rate levels, are consistent with CGF’s assumptions, underpinning FY20 guidance.

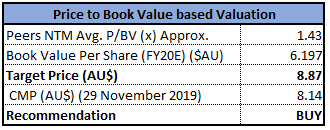

Valuation Methodology:Price to Book Value Multiple Approach

Price to Book Value Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation:CGF’s share generated negative a YTD return 10.30%. Its gross margin for FY19 stood at 74.1%, better than the industry median of 66.3%. Its cash cycle for FY19 stood at negative 459.5 days as compared to the industry median of positive 538.0 days, which implies that the company is efficiently managing its asset-liability balances. Its debt to equity ratio for FY19 stood at 1.97x, lower than industry median of 2.12x. Considering the financial performance, business prospects and aforesaid facts, we have valued the stock using one relative valuation method, i.e., Price/Book Value Multiple, and arrived at the target price of lower single-digit growth (in % term). Hence, we recommend a “Buy” rating on the stock at the current market price of $8.140, down 0.611% on November 29, 2019.

Bank of Queensland Limited

BOQ’s Share Under-Valued at the Current Juncture:Brisbane Headquartered, Bank of Queensland Limited (ASX: BOQ) is an Australian retail bank, which was established in 1863.

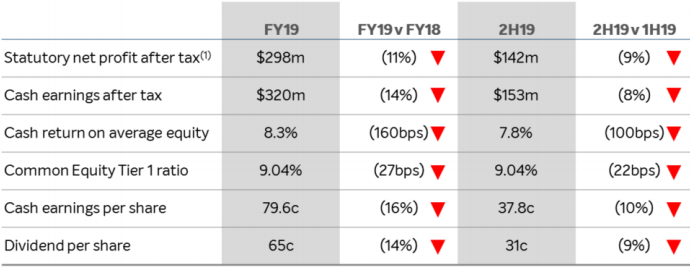

FY19 Key Highlights for the period ended June 30, 2019:Statutory net profit after tax decreased by 11% to $298 Mn, and cash earnings after tax decreased by 14% to $320 Mn. Cash return on equity reduced to 8.3%, with a common equity tier 1 also reduced to 9.04%. Cash earnings per share decreased by 16% to 79.6 cents per share. The Board of Directors declared a second half dividend of 31 cents per share, a reduction of 14%. As total income reduced by 2% and operating expenses increased by 4%, the cost to income ratio increased to 50.5% for the year and was higher in the second half. Loan impairment expense increased by 33 Mn to 74 Mn, or 16 basis points of gross loans.

FY19 Key Metrics (Source: Company Reports)

What to expect:As per the release, low credit growth and lower interest rates have hampered Bank’s net interest income growth. Moreover, bank’s operating expenses have increased in-line with the stated guidance. Uplift in regulatory and compliance costs are expected to be continued in FY20, which may hamper company’s earnings. However, positive future economic growth would help the growing population to spend more, leading to an increase in loan disbursements by banks.

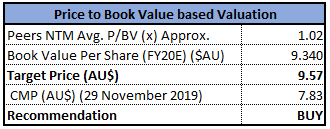

Valuation Methodology:Price to Book Value Multiple Approach

Price to Book Value Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation:BOQ’s share generated a negative YTD return of 16.09% and is currently trading close to its 52-week low level of $7.750, proffering an opportunity for share accumulation. Its annual dividend yield stands at 8.15%. Despite the disappointing FY19 performance, company’s investments in new innovative technologies are expected to deliver good value to the Bank’s customers and help the bank to boost its earnings in the coming times. Considering the business highlights and outlook, we have valued the stock using a relative valuation method, i.e., Price to Book Value Multiple and arrived at a target price of double-digit growth (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of A$7.830 per share, down 1.88% on November 29, 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...