.png)

Stocks’ Details

QBE Insurance Group Limited

Turnaround Into Profits In FY18 From Loss In FY17: QBE Insurance Group Limited (ASX: QBE) recently updated about its ongoing buy-back event wherein the company has bought back 38,17,225 shares at the total consideration of $4,72,93,484.44. The company intends to achieve up to a maximum of A$286 million in value.

Financial Performance in FY18: Net profit after tax for FY18 was $390 million as compared to a loss of $1,249 million in FY17. The Group turned into underwriting profit of $480 million in FY18 from a loss of $507 million in FY17 with an improved combined operating ratio of 95.9% in FY18 against 104.5% in last year. The result benefited on the back of significantly reduced catastrophe claims, a strong improvement in the attritional claims ratio as well as higher underlying positive prior accident year claims development, reflected in the lower net claims ratio which stood at 63.6% in FY18 as compared to 71.5% in FY17. Result in FY17 was negatively affected due to Ogden decision in the UK ($141 million).

The combined commission and expense ratio witnessed an improvement to 32.3% in FY18 from 33.0% in FY17.

.png)

Reconciliation of cash profit after tax (Source: Company Reports)

What to Expect: The group expects Combined operating ratio to be in the range of 94.5%-96.5% with net investment return at 3.0%-3.5%. The company also expects to complete the disposal of operations in FY19 at few places like Colombia, Puerto Rico, Indonesia and the Philippines, with the remaining personal lines business in North American Operations and the travel business in Australian & New Zealand Operations.

Stock Recommendation: The annual dividend yield for the stock comes in at 3.86% with market capitalization at $17.16 billion. Looking at the price performance, the stock has gained 27.34% in the last 1-year. From the valuation perspective, the stock is trading a price to book multiple of 1.4x, lower as compared to 2.4x of its industry median. FY 2018 ended with improved financials with higher gross written premium (up 3%), adjusted combined operating ratio under 100%, a rise in attritional claims ratio at 50.2% with respectable YTD stock price appreciation of 31.47%, we give a “Hold” recommendation on the stock at current market price of $13.080 per share (up 1.004% on 03 May 2019).

Challenger Limited

MS&AD Intends to Raise its Stake More Than 15% In CGF: Challenger Limited (ASX: CGF) is an investment manager with the leading annuity provider and one of the leading growing funds managers in Australia, mainly operates in two segments- a fiduciary Funds Management division and an APRA-regulated Life division.

The company recently updated about the progress regarding the strategic relationship with the MS&AD Groupwhich underpins CGF’s presence in Japanese annuities market. Under a new arrangement with MS Primary, CGF will commence reinsuring US dollar denominated annuities issued into the Japanese market by MS Primary, from 1 July 2019. MS Primary will provide to Challenger Life an annual amount of reinsurance, across both Australian and US dollar annuities, of at least ¥50 Bn (~A$640 Mn) each year for a minimum of five years.MS&AD also intends to raise its stake in the form of share in CGF >15%.

Financial Performance in 1H FY19: Volatile investment market impacted the earnings with lower asset returns in the Life business and lower Funds Management performance fees. Normalised NPAT in 1H FY19 came down by 4% to $200 million. Statutory NPAT (which includes investment experience, being the valuation movements on assets and liabilities supporting the Life business) was $6 million primarily due to volatile equity and fixed income markets in the December quarter.

Total AUM for the company as on third quarter of FY19 stood at $81 billion, up 4% in the quarter, driven by the rebound in investment markets. The total annuity sales came in at $662 million, down 13% on pcp.

.png)

Key Metrics (Source: Company Reports)

What to Expect: Australian superannuation system is supported by mandatory contributions, which are expected to rise from currently 9.5% of gross salaries to 12.0% by 2025.The superannuation system is expected to grow to over $10 trillion by 2035 from the current $2.6 trillion. Change in demographics and Government enhancing the retirement phase of superannuation also provide support to the growth in the superannuation system. The overall strong industry outlook augurs well for the CGF to take benefit out of it.

Stock Recommendation: Currently, the stock is available at the price to earnings multiple of 37.850x. The annual dividend yield for the stock comes in at 4.28% with market cap at $5.07 billion, at the price of $8.210.

Challenger is well positioned as a market leader with strong track record in developing high quality products across the segment.With highly scalable business and operating platform and strong risk management, CGF stands strong to meet customer needs.

Having said that, we give a “Buy” recommendation on the stock at the current market price of $8.210 per share (down 0.965% on 03 May 2019).

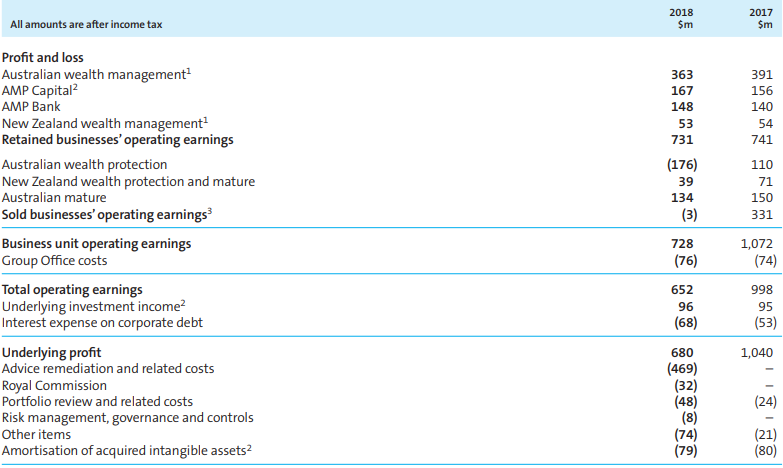

AMP Limited

Cashflows Update for 1QFY19: AMP Limited (ASX: AMP), on 02 May 2019, announced that John Patrick (JP) Moorhead is appointed as Chief Financial Officer (CFO), with effect from 1 June 2019. The net cash outflows for Australian wealth management (AWM) stood at A$1.8 billion, including A$538 million of regular pension payments, reflected expected continued weakness in inflows and higher outflows in the post-Royal Commission environment. AMP Capital net external cash outflows came in at A$20 million reflected quarter-end liquidity management. Deposits of AMP Bank rose by A$218 million with the highest growth in retail deposits, and total loan book grew by A$127 million to A$20.1 billion.

Solid growth in AUM was witnessed across Australian wealth management (5%), New Zealand wealth management (7%) and AMP Capital (4%) during the 1Q FY19, primarily driven by stronger investment markets.

Financial Performance in FY18: Underlying profit for FY18 saw a decrease of 35% to $680 million from $1,040 million in FY17, reflecting the impact of businesses subject to sale, with the operating earnings of retained businesses slightly weaker than FY17, driven by lower earnings for AWM (down 7%), offset by growth in AMP Capital (+7%) and AMP Bank (+6%).

Key Financial Highlights (Source: Company Reports)

What To Expect: AMP’s focus remains on transforming the business model in Australian wealth management to compete in a more efficient manner. The company already has taken actions to improve the outcome for customers which includes a decrease in fee on MyNorth products, which builds on the MySuper fee cuts, it delivered to clients in 2018. The management will continue to modernise its products to put AMP in a position where we can win in the market.

View and Recommendation on the Stock: At the current market price of $2.240, the stock is trading at price to earnings multiple of 225x which is higher than the concerned industry median.

Cashflows from Australian wealth management business is expected to face some challenges given the post-Royal Commission environment, with this the company remains its focus to transform it more competitive.However, in the span of previous 6 months, the stock posted the return of -16.36%.

Thus, we have a wait and watch view on the stock at the current market price of $2.240 per share (down 0.444% on May 3, 2019).

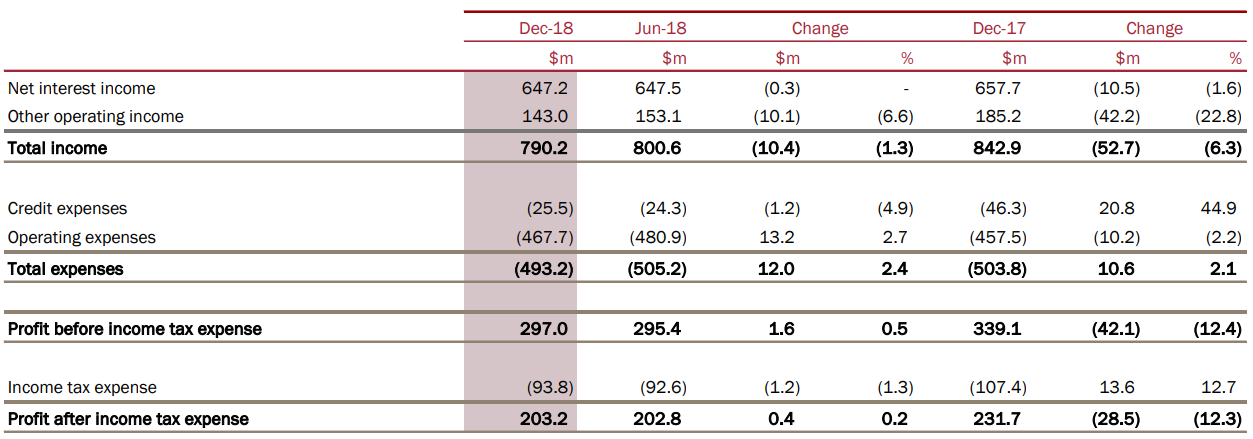

Bendigo And Adelaide Bank Limited

Financial Overview of 1H FY19: Bendigo And Adelaide Bank Limited (ASX: BEN), Australia’s leading retail bank, performed well despite an uneven playing field in a subdued, challenging, Royal Commission environment. The company recorded statutory profit after tax of $203.2 million for 1H FY19 with underlying cash earnings at $219.8 million.

NIM (or net interest margin), before revenue share arrangements, saw a decline of 1bps and stood at 2.35% mainly attributed to higher funding costs.

Financial Summary (Source: Company Reports)

What To Expect: The company has been actively managing margin for both lending and deposits. The management expects front book lending discounts will continue to challenge margin in second half of FY19.

Stock Recommendation: The stock is available at the price to earnings multiple of 11.880x with annual dividend yield at 6.76% and market capitalization at $5.09 billion. Given the deep customer connection and expansive points of presence across all channels with strong delivered growth in recent past, BEN is better place as compared to its peer group. However, its 3-month return stood at -3.90%.

Based on mixed updates and current trading scenario, we advise the market players to keep a watch on the stock at the current market price of $10.420 per share (up 0.676% on 03 May 2019) and wait for further growth catalyst.

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...