Stocks’ Details

Macquarie Group Limited

Macquarie Exempted from Sec 259C:Macquarie Group Limited (ASX: MQG) acts primarily as an investment intermediary for institutional, corporate, government and retail clients and counterparties around the world, generating income by providing a diversified range of products and services to its clients. The market capitalisation of the company stood at $48.81 billion as on 11th November 2019.

Macquarie has been granted relief from section 259C of the Corporations Act 2001 relating to certain acquisitions of Macquarie shares by Macquarie Group companies.In relation with the exemption, the company has notified that, as at 01 November 2019, the number of voting shares of Macquarie in respect of which it or its controlled entities have the power to control voting or disposal expressed as a percentage of the total number of voting shares of Macquarie is 5.70%, out of which 4.52% is related to employee share plans.

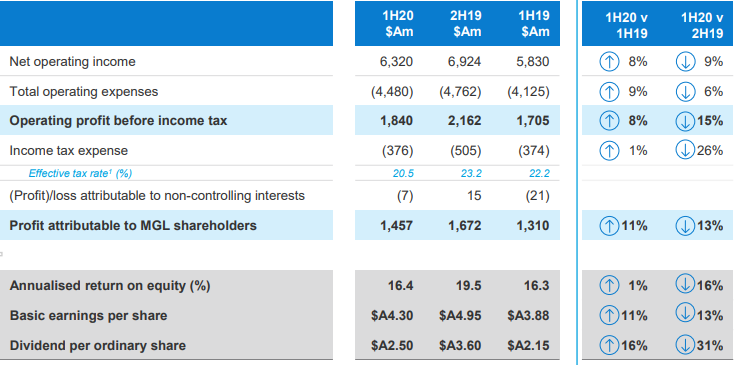

Macquarie Reports Profit Growth of 11%: In 1H20, the company has reported a net profit of $1,457 million, up by 11% YoY and down by 13% on 2H19. The company’s 1HFY20 result highlights the benefits of business and geographic diversity of the company, with enhanced client activity across many business lines and encouraging market conditions across the commodities and global markets platform.

The company declared an ordinary interim dividend of $2.50 per share (40% franked), which is higher than the interim ordinary dividend of $2.15 per share (45% franked), declared in 1H19.The company reported annualised ROE of 16.4%, in-line with 1H19 but down from 19.5% in 2H19.

Financial Highlights (Source: Company Reports)

Outlook: The company expects that the result for FY20 will be slightly lower than the results of FY19. The Company’s short-term outlook is dependent on a range of factors such as the completion rate of transactions and period-end reviews, market conditions, the impact of foreign exchange, etc. But it remains well-positioned to report superior performance in medium-term due to its thorough expertise in major markets, strength in business and geographic diversity.

Stock Recommendation: As per the ASX, the stock has gained 12.55% and 11.05% in the last three months and six months, respectively, and is currently trading close to the upper band of its 52-week trading range of $103.300 - $138.070. The stock is trading at a price to earnings multiple of 14.890x, which is above the industry median of 13.5x on TTM basis. Hence, considering its subdued outlook for FY20 along with current valuation and recent price movement, we have an “Expensive” rating on the stock at the current market price of $136.240 per share, down by 1.089% on 11th November 2019.

Insurance Australia Group Limited

Resignation of Company Secretary:Insurance Australia Group Limited (ASX: IAG) is a provider of general insurance, which comprises of a full range of personal and commercial insurance products. The market capitalisation of the company stood at $18.19 billion as on 11th November 2019. The company has announced that Ms Rebecca Farrell has resigned as the Company Secretary of IAG, effective from 1st November 2019, and Ms Sejil Mistry remains the Company Secretary of IAG.

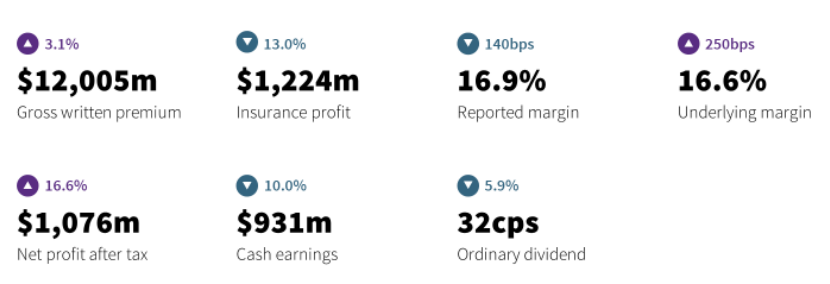

Highlights of AGM: The company reported pleasing results for FY19 due to ongoing underlying improvement in the business.Gross written premium increased by over 3%, mainly due to increased prices, supported by favourable foreign exchange translation effect in New Zealand. Like-for-like premium growth across the company was near 4%. NPAT was up by 16.6% on YoY basis becauseof the inclusion of over $200 million profit on the sale of Thailand operations.

Financial Summary (Source: Company Reports)

FY20 Outlook: The company is guiding GWP growth of low single-digit. The reported insurance margin is expected to be between 16% to 18%, which includes decent improvement in underlying performance, some offset from higher regulatory and compliance costs, and a reduction in reserve release expectations.

Stock Recommendation: IAG reported decent growth in its bottom-line with a CAGR of 10.26% over the period of FY15 to FY19. Looking at the valuation, the stock is trading at an EV/EBITDA multiple of 13.2x on TTM basis, which is above the industry average of 10.4x. This shows that the stock is trading above its peers. Based on the higher valuation multiple and current trading levels, we have a watch view on the stock at the current market price of $7.860 per share, down by 0.127% on 11th November 2019 and suggest investor to wait for further catalysts to support the valuation.

QBE Insurance Group Limited

Decent Top-line growth in 1H19: QBE Insurance Group Limited (ASX: QBE) is an international general insurance and reinsurance company which is engaged in underwriting general and reinsurance risks, investment management and management of the economic entity’s share of the NSW and Victorian workers’ compensation scheme. The market capitalisation of the company stood at $16.92 billion as on 11th November 2019. The group notified the cancellation of 948,000 QBE shares as part of the on-market share buyback and, after the cancellation of shares for the buyback, the total number of shares on the issue is 1,310,962,587.

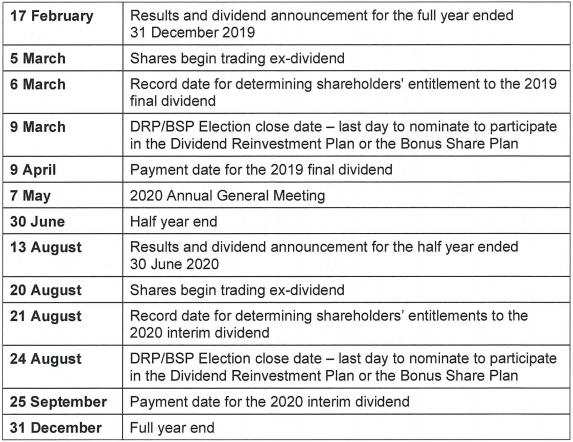

Financial Calendar for 2020: The company has released its calendar, which consists of few important dates for the investors. These dates are given below.

Key Financial Dates for 2020 (Source: Company Reports)

Changes in Senior Management: QBE has appointed Todd Jones as the CEO North America, succeeding Russ Johnston, who has decided to seek opportunities outside of QBE.Earlier, Mr Jones was the Head of Global Corporate Risk and Broking at Willis Tower Watson, and prior to that he was the CEO of Willis North America. He has also held several senior roles at AON in North America.

Results Highlights for 1H19: The group reported a statutory net profit after tax of $463 million, up by 29% from $358 million in the prior period.The cash profit after tax stood at $520 million up by 35% from $385 million in the prior period, and the cash profit return on equity was 13.4%, up from 9.6% in the prior period. The company’s half year financial performance reflects a significant improvement in attritional claims experience across all divisions combined with materially stronger investment returns. These were partially offset by an expected increase in the net cost of large individual risk and catastrophe claims, followed by the successful renegotiation of the group’s reinsurance program.

Outlook For 2019: The company’s full-year guidance for 2019 remains unchanged, and the combined operating ratio is expected to be between 94.5% to 96.5%. The net investment return is expected to be between 3.0% to 3.5%.

Stock Recommendation:As per the ASX, the stock gained 9.50% in the past three months, and is currently trading close to the upper band of its 52-week trading range of $9.500 - $13.160. Currently, the stock is trading at a price to earnings multiple of 23.480x, which is above the industry average of 16.4x on TTM basis. Based on its unchanged guidance for FY19, current trading levels, and valuation, we give a “Hold” recommendation on the stock at the current market price of $12.870 per share, down by 0.31% on 11th November 2019.

Suncorp Group Limited

Amendment in the Terms of Convertible Preference Shares: Suncorp Group Limited (ASX: SUN) is engaged in the provision of banking, insurance, wealth and other financial solutions to retail, corporate and the commercial sectors. The market capitalisation of the company stood at $16.82 billion as on 11th November 2019.

Suncorp Group Limited announced that it has amended the terms of the convertible preference shares issued by SUN in March 2014 (CPS3).The amendments have been made to facilitate the reinvestment offer, under which eligible CPS3 Holders may apply to reinvest some or all of their CPS3 in capital notes 3.

Eligible CPS3 holders who elect to participate in the reinvestment offer will receive the usual quarterly dividend on 17 December 2019, subject to the payment tests in the CPS3 Terms.

Suncorp Launches New Capital Notes Offer: Suncorp announced its intention to raise $250 million with the ability to raise more or less, through the offer of Suncorp Capital Notes 3. These notes are expected to be quoted and traded on the ASX under the code SUNPH.

These notes are fully paid, perpetual, unsecured, subordinated and mandatorily convertible notes issued by Suncorp. Distributions are floating rate, discretionary, non-cumulative, expected to be fully franked and scheduled to be paid quarterly.

Completion of Sale: Suncorp has announced that it has completed the sale of Capital S.M.A.R.T Group and ACM Parts to AMA group.The sale values 100% of Capital S.M.A.R.T at $420 million. ACM Parts was sold for a cash consideration of $20 million, which were broadly in line with book value.

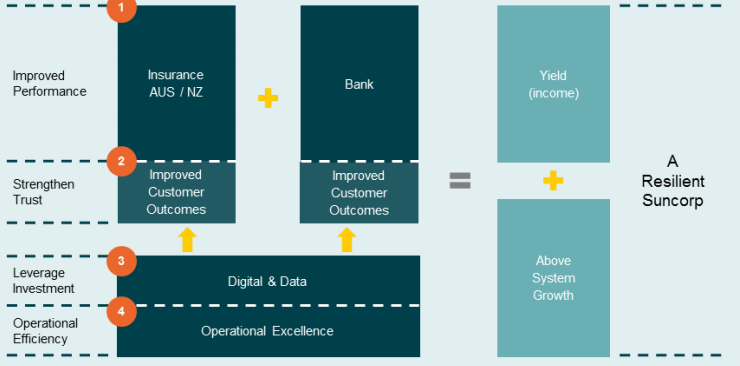

Company’s Plans for FY20: The company has made four key priorities to deliver improved performance in FY20. The first of this strategy is to align all their people and programs of work around improving the performance of insurance and banking businesses. The second priority is to adopt regulatory change, strengthen trust and improve customer outcomes. Company’s third priority revolves around increasing the scale of digital capability. The final priority is to remain focused on improving the operational efficiency of the business.

Key Priorities (Source: Company Reports)

Stock Recommendation: Currently, the stock is trading at an EV/EBITDA multiple of 10.0x, which is slightly below the industry median of 10.5x on TTM basis. As per the ASX, the stock is trading above the average of its 52-week high and low of $14.155 - $12.054. The stock has corrected 4.13% in the last one year. Considering the current trading levels, valuation metrics and the company’s 4 pointers outlook plan, we have a “Hold” rating on the stock at the current market price of $13.520 per share, up 1.349% on 11th November 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...