Stocks’ Details

Challenger Limited

Strong Fund Flow to Boost Company’s Performance:Challenger Limited (ASX: CGF) is into investment management and provides financial security for retirement to its customers. CGF operates with two core investment businesses, a fiduciary Funds Management division and an APRA-regulated Life division. As per a recent announcement, Challenger Limited and its entities became an initial substantial holder of AMA Group Limited with the voting power of 5.28%.

Q1FY20 Operating Highlights for Period Ending 30 September 2019: CGF reported its Q1FY20 operating results wherein strong net flows contributed to a robust performance by Funds Management business, and there was a rise of 2% in the funds under management. There were strong flows in fixed income products, which include $69 million of flows generated by ActiveX Ardea Real Outcome Bond Fund, that implies demand from the retail investors for high quality, actively-managed ETFs.

The total annuity sales were reported at $842 million during Q1FY20, up 14% on a q-o-q basis.The Other Life reported sales of $936 million, up $737 million on Q4FY19. The company’s total assets under management amounted to $84 billion, reflecting a rise of 3% for the quarter.

.png)

Highlights of Q1FY20 Fund Under management (Source: Company Reports)

Outlook: As per the management guidance, the business is expecting a normalised net profit before tax in the range of $500 million -$550 million. Investment market conditions, including base interest rate levels, are consistent with CGF’s assumptions underpinning FY20 guidance.

Stock Recommendation:The stock of CGF is quoting at $7.550 with a market capitalization of ~$4.4 billion. The stock is trading towards its 52-week lower levels of $6.20, with an annual dividend yield of 4.94%. Despite ongoing disruption in the Australian wealth industry, total Life book grew 5.2% during Q1FY20. Hence, considering the above-stated facts coupled with current trading levels and business prospects, we recommend a ‘Buy’ rating on the stock at the current market price of $7.550 per share, up 5.007% on October 17, 2019

Bank of Queensland Limited

Sound Balance Sheet:Bank of Queensland Limited (ASX: BOQ) is into banking, financial and related services. Recently, BOQ announced the appointment of Mr Ewen Stafford as the Chief Financial Officer and Chief Operating Officer.

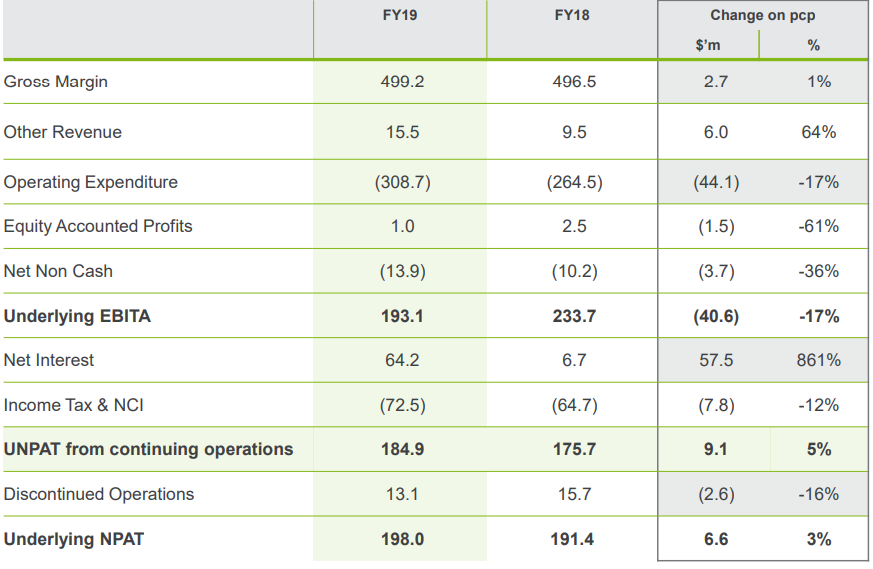

FY19 Operating Highlights for The Year Ending 31 August 2019:BOQ declared its full-year financial results wherein it reported total income of $1,089 million, which declined 2% on y-o-y basis and statutory net profit after tax of $298 million, down by 11% on a y-o-y basis. The bank posted net interest income at $961 million during FY19 as compared to $965 million in FY18. BOQ Finance has delivered robust growth through, dealer as well as structured finance programs.

The bank reported a deposit to loan ratio of 70% while it witnessed $1.1 billion growth in the customer deposits, predominantly via savings and investment accounts.BOQ declared a fully franked dividend of AUD 0.31000 payable on 27 November 2019.

.png)

FY19 Financial Highlights (Source: Company Reports)

Outlook:The balance sheet happens to be in the good shape which might attract the attention of market players. Its priorities primarily include returning to profitable and sustainable growth as well as simplification and productivity.

Stock Recommendation:The stock of BOQ is quoting at $9.420 with a market capitalization of ~$3.92 billion. The stock has delivered 4.44% and 7.82% in the last three months and six months, respectively. The stock is available at a price to book value (P/BV) of 1.0x on trailing twelve months (TTM) basis as compared to the industry median of 1.6x. BOQ continued growth in niche segments and Virgin Money Australia (VMA) and good progress in foundational investments. The bank possesses a strong balance sheet, which might help the bank moving forward. Considering the aforesaid facts, current trading levels, and business prospects, we recommend a ‘Hold’ rating on the stock at the current market price of $9.420 per share, down 2.383% on 17 October 2019.

MyState Limited

Strong Momentum in Customer Deposits to drive Business Growth:MyState Limited (ASX: MYS) is an ASX-listed non-operating holding company of diversified financial services group that consists of MyState Bank and Tasmanian Perpetual Trustees, a trustee and wealth management company. Recently, the company announced the appointment of Mr Gary Dickson as Interim CFO and will take the responsibility from 19 October 2019.

FY19 Operating Highlights for Year Ending 30 June 2019: MYS released its FY19 financial reports wherein it announced statutory NPAT at $31 million, but if discontinued operations are excluded, NPAT fell from $31.3 million to $29.8 million.During FY19, the company witnessed a 10.7% growth in loan book, well above industry peers. The following picture provides a broader overview of the key numbers:

.png)

FY19 Operating Highlights (Source: Company Reports)

Outlook:As per the management guidance, MyState Bank expects to deliver above system growth along with maintaining a high quality of loan book. The company will focus on the margin management due to the prevailing of a low-interest rate environment that is expected to be a feature of the industry in the coming years.

Stock Recommendation:The stock is trading towards its 52-week higher levels of $4.830 with PE multiple of 13.46x and an annual dividend yield of 6.25%.The stock of MYS has delivered a return of -0.43% and 11.92% during the last three months and six months, respectively. The stock is available at an enterprise value to sales (EV/Sales) of 3.4x on trailing twelve months (TTM) basis as compared to the industry median of 5.4x. The technology platform happens to be robust, simple and modern as well as allows to make productivity improvements faster and continually find efficient ways of doing the business.

Considering the aforesaid facts, we recommend a ‘Hold’ rating on the stock at the current market price of $4.690 per share, up 1.957% on 17 October 2019.

IOOF Holdings

Recent Acquisition to strengthen Company’s Footprint:IOOF Holdings Ltd (ASX: IFL) Ltd is into financial services with the market capitalization of ~$2.23 billion (as at 17 October 2019). IOOF has welcomed a receipt of No Objection Notices from OnePath Custodians Pty Limited as well as Australia and New Zealand Banking Group Limited with regards to transfer of ANZ Wealth Pension and Investments business (or ANZ P&I) to IOOF Holdings Ltd.

ANZ, as well as IOOF, have agreed on the changes to the terms of ANZ P&I acquisition, and purchase price stood at $825 million for ANZ P&I and has been revised down from $950 million. However, the purchase price is subject to the completion adjustment for net assets of ANZ P&I.

There has been a change in the revised date, after which either party can terminate the acquisition of ANZ P&I if there are any outstanding conditions precedent on that date. Previously that date was October 17, 2019, and the parties have agreed to extend that to December 31, 2019. Also, each party has an ability to extend that date on a monthly basis up to but not later than June 30, 2020. The parties have agreed to the changes to warranty caps associated with reduced purchase price and an amendment to Strategic Alliance Agreement, allowing for an earlier termination right by either party. The following picture provides an overview of the key numbers:

FY19 Operating Highlights (Source: Company Reports)

Guidance: The company is expecting an additional expense of $10 million in FY20 from governance investment. It was further stated that the impact of BT repricing is expected to be $12 million in FY20.The company added that the opportunities are underpinned by the diversified business model.

Stock Recommendation:The stock of IFL is ended at $7.050 with a market capitalization of $2.23 billion. The stock is trading towards its 52-week higher levels of $7.886 with PE multiple of 78.04x.The stock has delivered a return of 12.57% in the span of the previous one month, while in the time frame of the previous three months, it rose 25.46%. Hence, considering the aforesaid facts and current trading levels, we recommend a ‘Hold’ rating on the stock at the current market price of $7.050 per share, up 10.849% on October 17, 2019.

.JPG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...