Infigen Energy

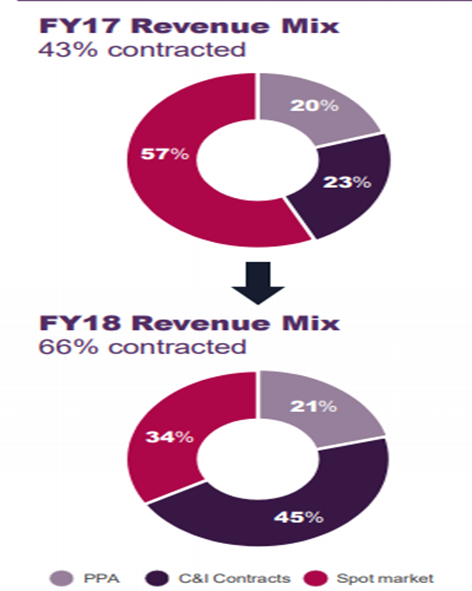

Decent Revenue Mix: Infigen Energy (ASX: IFN) posted strong FY18 results with net profit coming higher to $45.7 Mn, up $13.4 Mn against $32.3 Mn in FY17. Higher revenue was recorded as the increased productions were sold along with maintenance of electricity price in SA and marginally higher electricity price in NSW. The company has improved its revenue mix with successful implementation of the Multi – Channel Route to Market Strategy. Around 45% of the revenue was received from C&I contracts, depicting an increase of 23% from FY17.

Revenue Mix Compared (Source: Company Reports)

Slow transition and pace of integration of the renewable energy in the mainstream electricity market could pose challenge for the company going forward. The company might face multiple issues related to overall system strength at hand in the future to solve. For FY19, however, the company has laid out detailed plans, expecting to increase the production up to 14% with Bodangora. Battery storage development is underway in South Australia and is expected to go operational in 2H FY19. The company has maintained Net Interest Margin of 17.9%, higher than the industry standard of 7.1%, and this is a favorable metric for the company as it is comfortably converting the sales into profit. Return on Equity has declined from the previous year but at 3.5%, it is well in line with the Industry average of 3.8%. There is hardly any variance seen in the Debt/Equity ratio of the company at 1.14x compared to the Industry average of 1.20X. We believe that the gradual progression of the renewable energy in Australia, stable numbers posted by the company and favorable key metrics can make a difference.

Stock Performance: The stock has generated negative Year to Date yield of 14.49% and looks a bit under pressure at current juncture. However, any further weakness is not expected in the stock unless it breaches the support level of $0.550. Fundamentals of the company remain strong with PE at 12.990X, well below the competitors and efficiency of the company to convert its revenue into positive bottomline numbers. We therefore maintain ‘Hold’ on the stock at the current market price of $ 0.580.

Origin Energy

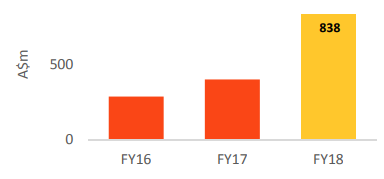

Good Results and positive outlook: Origin Energy Limited’s (ASX: ORG) stock surged 3.2% on September 11, 2018, after Prime Minister Scott Morrison announced that The National Energy Guarantee has been scrapped while outlook for gas and energy players stays at decent levels. The company has posted impressive full year numbers fueled by earnings growth in Energy markets and Integrated Gas. Underlying EBITDA from continuing operations came in higher at $2,947 Mn in FY18 compared to $2,173 Mn in FY17. Underlying profit was recorded at $838 Mn in FY18 compared to $400 Mn of pcp.

Profit Growth (Source: Company Reports)

The company recently announced that it would set up roughly 5-MW virtual power plant in Victoria that would harness the solar power and battery facilities. The power plant would be government funded and represent a cloud-based demand management platform enabling the storage of over 600 commercials as well as residential properties in Victoria. The company recently announced the substantial holding by BlackRock Group as the group now holds 5.06% voting power in Origin.

Stock Performance: The stock has been under pressure generating Year to date return of -18.22%. However, the recent bounce back from the support level of $7.526 is a positive sign for the investors. The rebound in the stock has come on the decent levels and there is no sign of divergence. We believe that the performance and the growth metrics of the company support our outlook of the company. We therefore maintain ‘Hold’ on the stock at the current market price of $ 8.070.

Oil Search

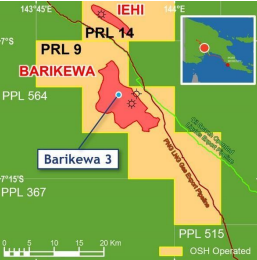

Strong Cash Flows: Oil Search Limited (ASX: OSH) was trading higher by 2.423% on September 11, 2018, underlined by the boost from the Prime Minister’s latest stance on the National Energy Guarantee. Net Profit for the 1H FY18 came in at US$ 79.2 Mn, a drop of 39% from US$129.1 Mn in the previous corresponding period. The profit declined largely due to PNG Highlands earthquake and costs. Further, the company has achieved positive operating cash flow, despite earthquake affect on the sales volume. OSH benefitted from the strong oil and gas prices which helped the company in maintaining the strong cash flows. Recently, the company’s Barikewa 3 results were positive followed by the successful appraisal of Kimu 2 which reached the total depth in late May 2018 and concluded as an extension of the Kimu gas reservoir.

Barikewa Result (Source: Company Report)

The company has declared interim dividend of USD0.02000 with ex -date on September 4, 2018, payable on September 25, 2018.

Stock Performance: The stock has performed well generating year to date return of 8.46%. Recent gap-down was short lived and the stock rebounded almost filling the gap. 14-day Relative Strength Indicator has touched the signal line and reversed sharply. Further, it is moving in tandem with the share price not showing any significant sign of divergence. We believe that profit was hit by the natural calamity that has already been factored in the stock price and from the current levels, the price is bound to move higher. We therefore maintain ‘Hold’ on the stock at the current market price of $ 8.680.

Santos

Rebuilding confidence: Santos Limited (ASX: STO) has been edging up on September 11, 2018, as investors decode the impact of recent KPL exploration update announced by the company. Santos has however performed well on the bourses this year, underlined by stellar results, reduction in debt and sale of non-core assets in Asia. The company has recently completed selling of its non-core Asian portfolio to Ophir Energy Plc. As a result of sales, the company has received the proceeds amounting to US$144 Mn at completion. The company has declared Interim dividend of USD 0.03500 payable on 27 September 2018. The company has been focusing on the low-cost operating model that stimulates the cash flows through the oil price cycle. The company believes that the recent acquisition of Quadrant Energy enhances the ownership of the company and would help in operating the high-quality portfolio of low cost, long life conventional Western Australia natural gas assets, strengthening the offshore capability of the company.

Stock Performance: The stock has performed well and structurally looks strong. Smaller corrections would not impact the secular trend of the price. As the company lightens its portfolio by selling non-core assets and focusses towards assets like Quadrant that can increase the capability of the company, and the same would be reflected in the stock price going forward. We therefore maintain ‘Hold’ on the stock at the current market price of $ 6.750.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...