Stocks’ Details

IPH Limited

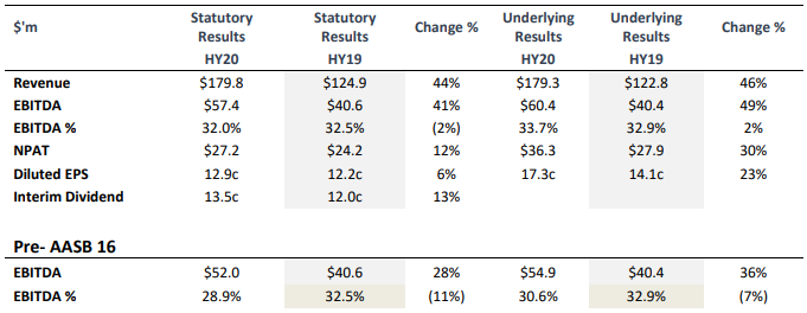

Double-Digit Organic Growth: IPH Limited (ASX: IPH) is engaged in the provisioning of intellectual property services. The market capitalisation of the company stood at $2.03 Bn as on 13th February 2020. The company recently released its results for 1HFY20, where the company reported statutory NPAT amounting to $27.2 million, reflecting a rise of 12%. The continuing momentum in Asia has helped the company to deliver double-digit organic growth in revenue and earnings. Moreover, diluted earnings per share of the company stood at 12.9 cents with a growth of 6%. These results demonstrate continuing improvement from the pre-existing business of IPH and a solid performance from the Xenith IP businesses, acquired by IPH on 15th August 2019.

For the shareholders, the company has declared a fully franked interim dividend amounting to 13.5 cps. This reflects 83% of cash adjusted NPAT.

Financial Summary (Source: Company Reports)

Focus for FY20: The strategic priorities of the company for the remainder of FY20 revolve around (1) continued successful Xenith IP integration with IPH, (2) to maintain market-leading position in Australia / New Zealand as well as continued margin expansion and (3) to continuously focus on Asia to develop the network effect.

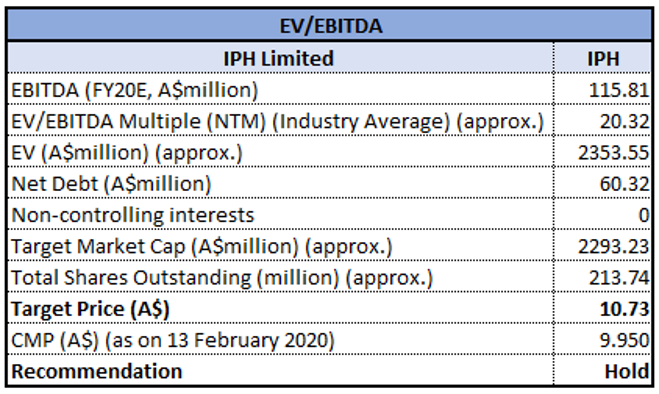

Valuation Methodology:EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per the key personnel of IPH, the company has reported a strong result. This can be seen in the continued growth of its pre-existing business and its ability to successfully integrate and generate further value through acquisitions. We have valued the stock using EV/EBITDA based relative valuation approach and arrived at a target price, which is offering an upside of high single-digit (in percentage terms). Hence, considering the strong results in 1HFY20 and focus for FY20, we maintain a “Hold” rating on the stock at the current market price of $9.950 per share, up by 4.737% on 13th February 2020, taking cues from the release of 1HFY20 results.

Treasury Wine Estates Limited

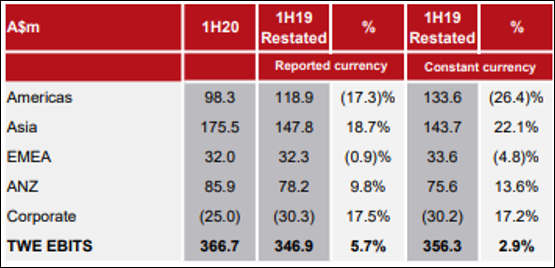

Decent Growth in 1H FY20: Treasury Wine Estates Limited (ASX: TWE) has footprints in the international wine business with a portfolio of luxury, premium and commercial wines. The market capitalisation of the company stood at $8.54 Bn as on 13th February 2020. Despite the difficult market conditions, the company managed to deliver a growth of 5% in NPAT, which amounted to $229.2 million. TWE delivered EBITS amounting to $366.7 million with a rise of 6%, with EBITS margin of 23.9%, up by 0.9 percentage points. In another update, the company announced that it has appointed Tim Ford as the Chief Executive Officer, which will be effective from 1st July 2020.

The Board of the company declared a fully franked interim dividend amounting to 20 cents per share, reflecting a rise of 11% as compared to pcp. At the current market price of $11.180 per share, the Annual dividend yield of the company stood at 3.37% as compared to the industry average (Beverages) of 3.5% on TTM basis.

EBITS by Region (Source: Company Reports)

Guidance for Reported EBITS Growth: For FY20, the company anticipated reported EBITS growth in the range of around 5% to 10% along with the existing challenging conditions in the US wine market, which are anticipated to persist through the remainder of the FY20. Moreover, full-year FY20 cash conversion is expected to be broadly in line with FY19.

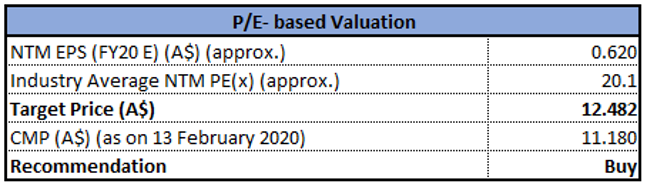

Valuation Methodology:P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: For FY21, the company anticipates reported EBITS growth of around 10% to 15%. During 1HFY20, the company maintained a strong and flexible balance sheet with improvement in leverage to 1.7x. We have valued the stock using P/E based relative valuation approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, in the light of a strong and flexible balance sheet and upside in valuation, we give a “Buy” recommendation on the stock at the current market price of $11.180 per share, down by 5.734% on 13th February 2020.

Goodman Group

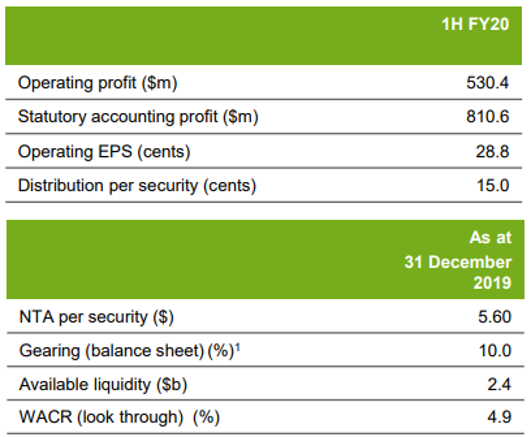

Strong Growth in Operating Profit: Goodman Group (ASX: GMG) is a globally integrated property company, which is focused on owning, developing and managing industrial property and business space in key markets around the world. The market capitalisation of the company stood at $28.16 Bn as on 13th February 2020. For the half-year ended 31st December 2019 (1H FY20), the company reported operating profit amounting to $530.4 million with a rise of 14.1% over 1H FY19, and operating earnings per share at 28.8 cents, which experienced a growth of 12.9%. These strong results have been generated by the focus of the company on specific markets where e-commerce is growing; consumer expectations are rising as well as the need for more efficient supply chains is becoming greater.

For 1HFY20, the company declared a distribution of 15.0 cents per stapled security, which is in line with the capital management strategy of the Group to achieve a payout ratio in the low 50% range.

Financial Overview (Source: Company Reports)

Distribution Guidance: For FY20, the company expects to deliver an EPS of 57.3 cents per security with a rise of 11% as compared to FY19. Also, it anticipates a full-year distribution of 30 cents per share for FY20.

Stock Recommendation: During the time span of the last 18 months, the company has made an investment of approx. $1 billion in its partnerships to finance acquisition and development opportunities.GMG has an EV to Sales multiple of 19.3x as compared to the industry average of 10.8x (Financials) on TTM basis. The stock of GMG is trading at a P/E multiple of 17.13x against the industry median (Financials) of 15.8x on TTM basis. As per ASX, the stock of GMG is trading close to its 52-week high levels of $16.600. Thus, considering the valuation and current trading levels, we give an “Expensive” rating on the stock at the current market price of $16.300 per share, up by 5.844% on 13th February 2020. The upside in the stock was largely due to the release of earnings for the half-year ended 31st December 2019.

Collins Foods Limited

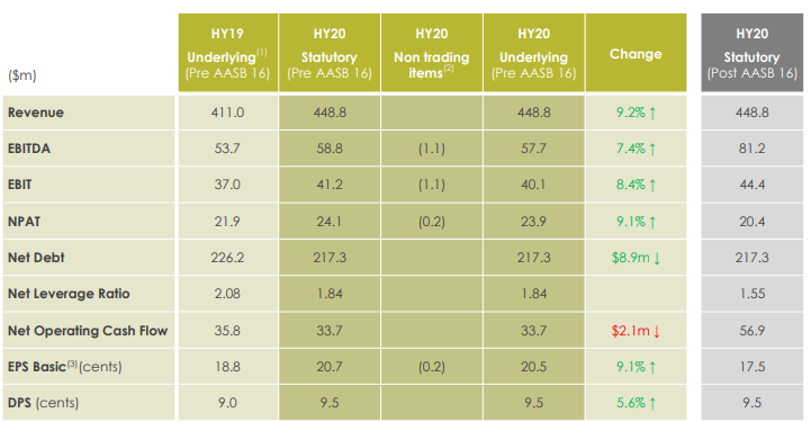

Settlement of Court Proceedings: Collins Foods Limited (ASX: CKF) is mainly engaged in the operation of restaurants. The market capitalisation of the company stood at $1.11 Bn as on 13th February 2020. The company recently notified about the settlement of the Federal Court proceedings, commenced by Taco Bill Mexican Restaurants (Australia) Pty Ltd, where a settlement was agreed between the parties involved. As a result of the settlement, the company would continue to open and operate Taco Bell restaurants in Victoria.

On the financial front, the company experienced a growth of 9.2% in revenue, which amounted to $448.8 million in 1H FY20. It experienced a decline in net debt to $217.3 million in 1H FY20 as compared to $226.2 million reported at the end of 1H FY19. The company declared a 100% franked interim dividend of 9.5 cents per ordinary share, representing the healthy operating cash flows of the business and its growth outlook.

Strong Earnings Growth (Source: Company Reports)

What to Expect: The company is focused on further strengthening all operational systems as well as executing on initiatives, which continue to improve the customer experience while maintaining operational excellence. The company is planning to build 4 new restaurants, which would take the net new restaurant count to 9 by the end of FY20.

Valuation Methodology:EV/EBITDA Based Valuation

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

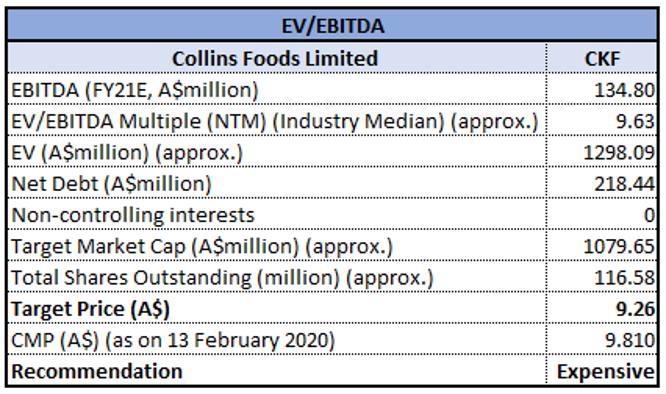

Stock Recommendation: With respect to KFC Australia network, the company experienced strong delivery performance and plans to further expand the delivery channel throughout its KFC restaurants. We have valued the stock using EV/EBITDA based relative valuation approach and arrived at a target price, which is offering correction of single-digit (in percentage terms). Also, the stock of CKF is trading close to its 52-week high of $10.800. Therefore, considering the valuation and current trading levels, we give an “Expensive” rating on the stock at the current market price of $9.810 per share, up by 2.615% on 13th February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...