.png)

Stocks’ Details

Monadelphous Group Limited

1HFY20 Revenue Up by 2.6% on PCP:Monadelphous Group Limited (ASX: MND) provides construction, maintenance and industrial services to the resources, energy and infrastructure sectors. The company recently updated that the voting power of Pendal Group Limited increased from 7.22% to 8.23%, with effect from 16th March 2020. As per another update, the company withdrew the guidance provided for FY20 due to the ongoing adverse repercussions of COVID-19.

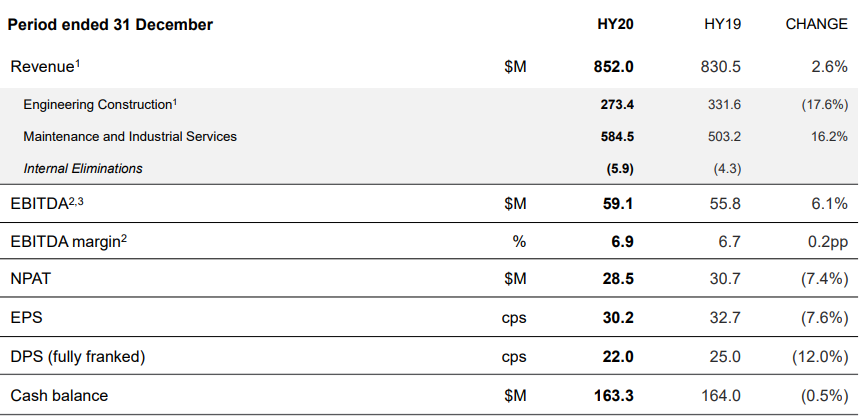

1HFY20 Results: During the first half ended 31st December 2019, the company reported revenue amounting to $852 million, representing an increase of 2.6% on the prior corresponding half. Net profit after tax came in at $28.5 million. Performance during the period was supported by strong results from the Maintenance and Industrial Services division with record growth in revenue. By the end of the period the company had a strong pipeline of work in hand with $850 million of new contracts. The Board declared an interim fully franked dividend amounting to 22 cents per share.

1HFY20 Financial Highlights (Source: Company Reports)

Outlook: Over the near term, the company expects favourable market conditions to offer significant opportunities in the resources and energy sectors. The company anticipates strong demand for maintenance services with record production levels in the resources and oil & gas sectors. However, overall performance for FY20 remains subject to the impact of COVID-19.

Valuation Methodology:EV/Sales Based Relative Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of the company corrected by 23.08% over a period of 1 month and is currently inclined towards its 52-week low level of $10.150. During 1HFY20, the company was focused on maximising growth through improved operations in core markets and enhanced service offerings. We have valued the stock using EV/Sales based relative valuation method and have arrived at a target price with lower double-digit upside (in percentage terms). For the said purpose, we have considered Worley Ltd (ASX: WOR), Downer EDI Ltd (ASX: DOW), Boral Ltd (ASX: BLD), etc. as peers. Hence, we give a “Buy” recommendation on the stock at the current market price of $10.500, down 16.667% on 18th March 2020, possibly due to a slowdown in economic activity and withdrawal of FY20 financial guidance.

Transurban Group

Excellent Project Delivery in 1HFY20:Transurban Group (ASX: TCL) is engaged in the building and operation of toll roads. The company recently updated that one of the directors, Louis Scott Charlton, disposed 200,000 stapled securities at an average price of $14.61 per security.

1HFY20 Results: During the six months ended 31st December 2019, the company reported a growth of 2.3% in average daily traffic, with proportional toll revenue going up by 8.6% to $1,396 million. Proportional EBITDA went up by 9.5% to $1,094 million.Moreover, proportional toll revenue witnessed a positive movement across all locations, including Sydney, Melbourne, Brisbane and North America. For the first half, the company declared a dividend amounting to 31.0 cents per share, fully out of the free cash flow of $927 million. The period was marked by successful project delivery, with completion of five major projects and two expected to be completed in mid-2020.

.png)

Proportional Toll Revenue (Source: Company Reports)

Valuation Methodology:EV/EBITDA Based Relative Valuation

.png)

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of the company corrected by 33.19% over a period of 1 month and is currently trading very close to its 52-week low level of $10.170. The company has been focused on enhancing the organisational capabilities and customer experience through improved systems and processes. For FY20, the company expects to distribute a total amount of 62 cents per share to its shareholders. We have valued the stock using EV/EBITDA based relative valuation method and have arrived at a target price with lower double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $10.350, down 4.255% on 18th March 2020.

Telstra Corporation Limited

Continued Progress on T22 Strategy:Telstra Corporation Limited (ASX: TLS) provides telecommunications and information services to domestic and international customers. The company recently updated that a director named Niek Jan Van Damme, acquired 40,000 ordinary shares for a total consideration of $123,900.

Half Yearly Highlights: During the period ended 31st December 2019, the company’s financial performance came out to be in line with expectations. Total income for the period stood at $13.4 billion, down 2.8% on the prior corresponding half. Underlying EBITDA went down by 6.6% and stood at $3.9 billion. The company reported good progress on the T22 strategy that has been building positive financial momentum and offers a clear vision of future achievements. The strategy has enabled a reduction of $422 million in underlying fixed costs through simplification in the business. For the half year, the Board declared a dividend amounting to 8 cents per share.

Guidance: Total income for FY20 is expected in the range of $25.3 - $27.3 billion. Underlying EBITDA is expected in the range of $7.4 - $7.9 billion. FY20 free cash flow after operating lease is expected in the range of $3.3 billion - $3.8 billion.

.png)

Income Statement (Source: Company Reports)

Valuation Methodology:Price to Earnings Based Relative Valuation

.png)

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of the company corrected by 5.94% over a period of 1 month and is currently inclined towards its 52-week low level of $2.9. With continued implementation of the T22 strategy, the company has been able to offer improved customer experience through new product and services and has been receiving a positive response in return. The company has been engaged in rationalising the number of products offered to its Enterprise customers and seems well positioned for a possible reduction of 50% by FY21. We have valued the stock using Price to Earnings based relative valuation method and have arrived at a target price with lower double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $3.180, down 8.357% on 18th March 2020.

Scentre Group

FY20 Distribution to Rise by 3%:Scentre Group (ASX: SCG) owns and operates Westfield centres in Australiai and New Zealand. The company recently updated that all its Westfield Centres, including supermarkets, grocery stores, food market and retail stores, will remain open for supply of daily essentials to the Australian community amid coronavirus outbreak. The company will ensure a safe and healthy environment across the centres for the well being of its customers and retail partners.

FY19 Results: During the 12 months ended 31st December 2019, Funds from Operations came in at $1.345 billion. Distribution for the year amounted to 22.60 cents per security, up 2% on the prior corresponding year. Annual customer visited grew to more than 548 million, reflecting the strength of the portfolio and strong demand from retail and brand partners.

.png)

FY19 Financials (Source: Company Reports)

Guidance: Operating earnings for FY20 are expected in the range of 24.75 – 24.80 cents per security, reflecting pro-forma growth of around 3.1%. FFO per security in anticipated to be ~25.30 cents, reflecting margins growth of 0.7% on FY19. Distribution is expected to increase by 3% to 23.28 cents per security.

Valuation Methodology:Price to Earnings Based Relative Valuation

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of the company corrected by 43.12% over a period of 1 month and is currently trading very close to its 52-week low level of $1.805. The company reported a strong financial position as at 31st December 2019, with sufficient liquidity of $1.8 billion to cover all debt maturities in 2020 and balance sheet gearing of 33%. The company has adapted itself to the changing needs of customers and has built a strong profile to deliver financial growth in the future. We have valued the stock using Price to Earnings based relative valuation method and have arrived at a target price with lower double-digit upside (in percentage terms). For the purpose, we have taken the peer group - GPT Group (ASX: GPT), Vicinity Centres (ASX: VCX) and Stockland Corporation Ltd (ASX: SGP). Hence, we give a “Buy” recommendation on the stock at the current market price of $1.800, down 16.279% on 18th March 2020.

Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...