.png)

Stocks’ Details

Transurban Group

Acquisition to be Free Cash Flow Accretive: Transurban Group (ASX: TCL) is engaged in building and operation of toll roads in Australia and North America.

Security Purchase Plan & Institutional Placement:The company recently completed a security purchase plan worth $312 million, comprising issue of approximately 21.3 million SPP securities at a price of $14.64 per security. In addition to the SPP, the company also completed an institutional placement worth $500 million. The above capital raisings were carried out with the purpose of securing funds for completing the acquisition of remaining 34.62% stake in M5 West.

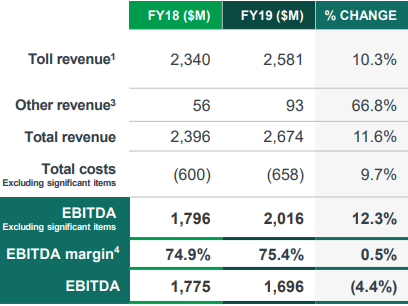

FY19 Results: During the year ended 30 June 2019, the company reported proportional toll revenue amounting to $2,581 million, up 10.3% on prior corresponding period. Statutory profit for the period amounted to $170 million and free cash flow stood at $1,527 million. Proportional EBITDA before significant items was reported at $2,016 million, up 12.3% in comparison to pcp. The company paid a dividend of 30.0 cents per share on 09 August 2019.

FY19 Proportional Results (Source: Company Reports)

Regional Performance:North America reported a remarkable increase of 45.0% in proportional toll revenue at $324 million and EBITDA growth of 61.1%. This was followed by a growth of 10.4% in proportional toll revenue in Sydney. EBITDA for the region witnessed a growth of 12.2%. Proportional toll revenue and EBITDA in Melbourne increased by 4.2% and 4.0%, respectively. Revenue and EBITDA in Brisbane reported a rise of 2.3% and 5.4%, respectively.

Outlook: Distribution for FY20 is forecasted at 62.0 cents per share, including fully franked portion of 4.0 cps.

Stock Recommendation: The stock of the company generated a return of 30.93% in the last one year. The company reported a decent financial position during FY19, with the acquisition of M5 West being one of the key highlights. The company conducted equity raising to acquire the remaining stake in the asset, which is expected to be free cash flow and value accretive in FY20. Free cash flow accretion inclusive of the equity raising is expected to be approximately 3 cents per security in FY20. Currently, the stock is trading towards its 52-week high levels of $16.06 with PE multiple of 222.58x. Hence, considering aforesaid facts and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $14.980, up 1.974% on 01 October 2019.

G.U.D. Holdings Limited

Focus on Creating Medium Term Value:G.U.D. Holdings Limited (ASX: GUD) is engaged in manufacturing, distribution and sale of automotive products, pumps, pool and spa systems in Australia, New Zealand, Spain and France.

Dividend: On 30 August 2019, the company paid a dividend amounting to 31 cents per share, up 11% on previous year dividend of 28.0 cents.

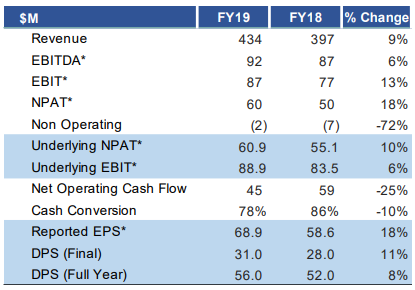

FY19 Financial Highlights: During the year ended 30 June 2019, the company reported revenue amounting to $434 million, up 9% on prior corresponding period revenue of $397 million. EBITDA for the year stood at $92 million, representing an increase of 6% on prior corresponding period EBITDA of $87 million. Net profit after tax stood at $60 million, rising 18% on pcp NPAT of $50 million. Reported earnings per share for the year amounted to 68.9 cents, up 18% on previous year.

Financial Summary (Source: Company Reports)

Outlook: In FY20, the company expects to report a modest growth in EBIT and cash conversion of around 80%.Business operations in FY20 will be focused on creating medium term value rather than short term EBIT growth. Some of the plans in pipeline include improvement in business-wide operating efficiency, product range expansion and strengthening of customer relationships.

Stock Recommendation: The stock of the company generated returns of 11.65% over a period of 1 month. In FY19, the company reported a solid automotive revenue growth of 12% despite challenging environment. The period was marked by decent growth across the key business metrics including revenue, EBITDA and NPAT. Going forward, the company will focus on creating medium-term value to strengthen the foundation for sustainable EBIT growth. Considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $10.340, up 2.783% on 01 October 2019.

Super Retail Group Limited

Like for Like Sales Growth Across all Divisions:Super Retail Group Limited (ASX: SUL) is engaged in retailing of auto parts and accessories, sports equipment, boating and camping equipment etc. The company recently appointed Justin Coss as the interim Group General Counsel and Company Secretary, as a replacement to Peter Lim.

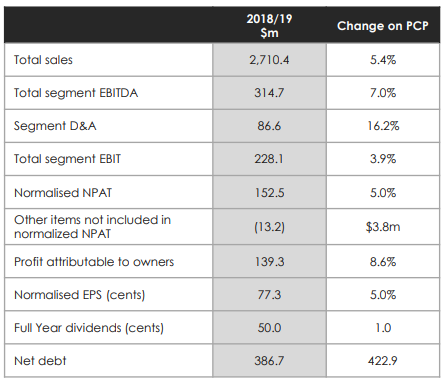

FY19 Results: During the 52 weeks period to 29 June 2019, total group sales amounted to $2.71 billion, representing an increase of 5.4% on prior corresponding period. Group segment EBITDA stood at $314.7 million, rising 7.0% in comparison to the prior corresponding period. Normalised net profit after tax was reported at $152.5 million, representing growth of 5.0% on previous year. The company declared a fully franked final dividend of 28.5 cents per share with full year dividends totalling to 50.0 cents per share.

FY19 Financial Highlights (Source: Company Reports)

Trading Update: During the first 6 weeks of FY20, the group’s three major businesses witnessed growth in like for like sales.BCF reported the highest growth of around 5%, followed by Supercheap Auto and Rebel with approximate growth of 3% and 2%, respectively. In FY20, the company expects to incur capital expenditure in the range of $85 million - $90 million.

Stock Recommendation: Over a period of 6 months, the stock of the company generated returns of 21.72%. In FY19, the company reported like for like sales growth across all divisions which was carried forward in FY20 to the company’s major businesses. The period was also marked by strong operating cashflows, supporting a reduction in net debt of the company. The company expects the implementation of a proposed new Enterprise Agreement for retail and clerical workers, which is expected to provide an incremental EBITDA of around $9 million in the first year. Currently, the stock is trading closer to its 52-week high levels of $10.29 with PE multiple of14.05x and an annual dividend yield of 5.04%. Hence, considering the above scenario, we give a “Hold” recommendation on the stock at the current market price of $9.880, down 0.403% on 01 October 2019.

SkyCity Entertainment Group Limited

Decent Performance from Local Businesses:SkyCity Entertainment Group Limited (ASX: SKC)is engaged in the business of providing tourism, leisure and entertainment services.

The company recently updated that 4 of its senior managers including Michelle Lee-Ann Baillie, Robert David Hamilton, Simon Peter Jamieson and Joanna Lee Wong, disposed ordinary shares on account of share forfeiture under the company’s Executive Long-Term Incentive Plan.

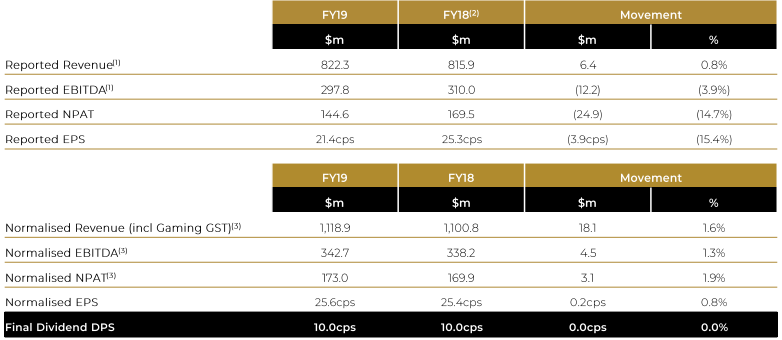

FY19 Results: During the 12 months ended 30 June 2019, the company’s reported revenue from continuing operations amounted to NZ$822.3 million, up 0.8% on prior corresponding year. Total reported revenue for the period stood at NZ$905.4 million, down 2.5% on pcp. Reported net profit for the period stood at NZ$144.6 million, down 14.7% on prior corresponding period.

Normalised revenue (including revenue including gaming GST) for the year went up by 1.6%, at NZ$1,118.9 million in FY19. Normalised total net profit was reported at NZ$173.0 million, up 1.9% on prior corresponding period. During the year, the company realised net proceeds of approximately NZ$450 million from asset sale programme. The period was also marked by the launch of an offshore online casino in partnership with Gaming Innovation Group. The company paid a fully imputed final dividend of 10.0 cents per share to the shareholders.

Results Summary (Source: Company Reports)

Outlook: Despite a challenging operating environment, the company expects to deliver a revenue growth across various businesses in FY20.With continuous improvement in performance, the company expects to report some earnings growth on a like-for-like basis.

Stock Recommendation: The stock of the company generated returns of 2.78% and 2.21% over a period of 1 month and 3 months, respectively. In FY19, the company reported decent performance from local businesses along with growth in international business turnover. Going forward, FY20 and FY21 are expected to be periods of transition for the business with two upcoming major projects in Auckland and Adelaide. The company possesses a decent platform to deliver on its strategic plan and support positive medium-term earnings growth. In FY19, the company had an EBITDA margin of 35.3%, which is higher than the industry median of 25.2%. Net margin in FY19 was reported at 20.0% as compared to the industry median of 9.4%.Currently, the stock is trading closer to its 52-week high levels of $3.90 with PE multiple of 18.09x and an annual dividend yield of 5.13%. Based on the above factors, we give a “Hold” recommendation on the stock at the current market price of A$3.740, up 1.081% on 01 October 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...