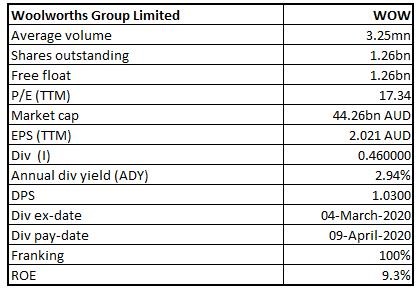

Woolworths Group Limited

WOW Details

Added New Funding to Refinance Future Debt: Woolworths Group Limited (ASX: WOW) is in food, general merchandise and specialty retailing via chain store operations. The market capitalisation of the company stood at $44.26 Bn as on 14th May 2020. Recently, the company successfully priced $400 million of senior unsecured five-year notes and $600 million of ten-year notes under its Euro Medium Term Note Programme. The company would utilize the proceeds from the Notes for the refinancing of future debt maturities of around $1 billion later in the calendar year 2020. The successful outcome of this transaction indicates the financial strength and attractiveness of WOW in the capital markets.

During Q3 FY20, the company experienced decent sales growth in all businesses except hotels business due to mandatory closure imposed by Government in response to COVID-19. It reported sales from continuing operations amounting to $16.5 bn with a rise of 10.7%. During 1H FY20, it declared an interim dividend of 46 cents per share with a rise of 2.2%.

.png)

Key Financials Q3 FY20 (Source: Company Reports)

Uncertainty Expected in Future: The company is not certain about its outlook for the remaining financial year due to these unprecedented circumstances. However, the company is in a strong operational and financial position.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: At the current market price of $35.020, annual dividend yield of the stock stands at 2.94%. The company continues to maintain solid investment-grade credit ratings on a stable outlook of Baa2 from Moody’s and BBB from S&P, respectively. Net margin of the company stood at 2.9% in 1H FY20 as compared to the industry median of 2.6%. This indicates that WOW has decent capabilities to convert its top line into the bottom line against the peer group.We have valued the stock using EV to Sales multiple based illustrative relative valuation method, and for the purpose, we have taken peers such as Coca-Cola Amatil Ltd (ASX: CCL), Metcash Ltd (ASX: MTS), Coles Group Ltd (ASX: COL) and arrived at a target price with an upside of lower double digit (in percentage terms). Thus, in light of strong operational and financial position and improvement in net margin, we give a “Hold” recommendation on the stock at the current market price of $35.020 per share, down by 0.057% on 14th May 2020.

WOW Daily Price Chart (Source: Refinitiv, Thomson Reuters)

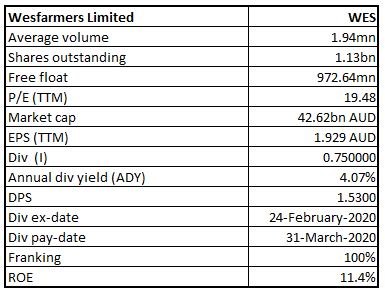

Wesfarmers Limited

WES Details

Portfolio of Cash-Generative Businesses: Wesfarmers Limited (ASX: WES) is engaged in diversified businesses with some interests in retail operations. The market capitalisation of the company stood at $42.62 Bn as on 14th May 2020. The company has a portfolio of cash-generative businesses, which is focused on long-term value creation. In response to COVID-19, every business of the group has executed several changes to protect the health and safety of team members and customer such as social distancing. The company stated that its Bunnings and Officeworks division has witnessed significant demand growth over the last two months as customers and their families spent more time working, learning, and relaxing at home.

The company has paid fully franked interim dividend of $0.75 per share for 1H FY20. The company has an Annual Dividend Yield of the company stood at 4.07%, higher than the industry average (diversified and Retail) of 3.7% on TTM basis. The below picture gives an overview of financial performance for 1H FY20

.png)

Financial Performance (Source: Company Reports)

Future Aspects: The company would continue to invest for the future, expand digital offerings & capabilities & strengthen the customer value proposition.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: WES is currently experiencing robust sales momentum in Bunnings, Officeworks & Catch. As at 30th April 2020, the net financial debt of the company stood at $0.7 Bn, which include issued bonds and drawn bank debt. At the current market price of $37.55, annual dividend yield of the stock stands at 4.07%. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers like Coles Group Ltd (ASX: COL), Woolworths Group Ltd (ASX: WOW) and Coca-Cola Amatil Ltd (ASX: CCL). Thus, considering the portfolio of cash generative businesses and decent growth in sales, we give a “Hold” recommendation on the stock at the current market price of $37.550 per share, down by 0.106% on 14th May 2020.

WES Daily Price Chart (Source: Refinitiv, Thomson Reuters)

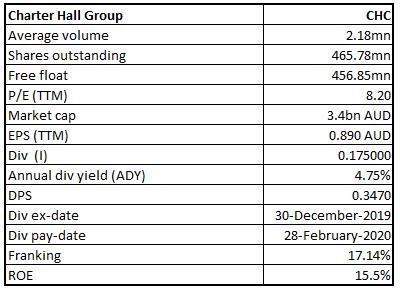

Charter Hall Group

CHC Details

Decent Growth in Distribution: Charter Hall Group (ASX: CHC) is an integral property group, which operates in fund property funds management, development property, property investment banking. The market capitalisation of the company stood at $3.4 bn as on 14th May 2020. Recently, the company notified the market that it has experienced challenges and opportunities for its business and people from COVID-19. The company reported FY20 YTD (14th May 2020) equity inflows amounting to $4.6 Bn throughout all source segment. Funds under management for the period stood at $39.2 billion with FUM Growth of $8.8 billion on a YTD basis. During half-year 2020, the company declared distribution amounting to 17.5 cents per share, reflecting a rise of 6% over pcp.

.png)

Key Financials FY20 YTD (Source: Company Reports)

Reiterated Guidance:For FY20, the company has reiterated post-tax operating earnings per security growth of around 40% on FY19. This follows a further review of the impacts of COVID-19.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: At the current market price of $7.610, annual dividend yield of the stock stands at 4.75%. The company has a highly defensive earnings stream from its well-diversified property investments, which are held by Charter Hall Property Trust. The development pipeline of the company is growing continuously.Over the span of five-years (2015-2019), the company has experienced CAGR of 18.30 in free cash flows, which reflects that the company is managing its working capital very prudently. We have valued the stock using EV to Sales multiple based illustrative relative valuation method, and for the purpose, we have taken peers such as GPT Group (ASX: GPT Dexus (ASX: DXS), LendLease Group (ASX: LLC) and arrived at a target price with an upside of lower double-digit (in percentage terms). Hence, considering the highly defensive earnings stream and decent working capital management and growing development pipeline, we give a “Buy” recommendation on the stock at the current market price of $7.610 per share, up by 4.247% on 14th May 2020.

CHC Daily Price Chart (Source: Refinitiv, Thomson Reuters)

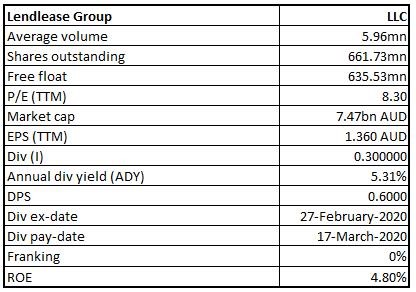

Lendlease Group

LLC Details

Equity Raising to Strengthen Balance Sheet:Lendlease Group (ASX: LLC) is mainly into retail property management with a market capitalisation of the company stood at $7.47 Bn as on 14th May 2020. Recently, the company wrapped up placement to institutional investors and raised $950 million. In order to raise additional funds of $200 million, the company has offered a security purchase plan to eligible shareholders. The company would use the proceeds to cement balance sheet as well as to support future growth. The equity raising will place the company well to continue with the delivery of its development pipeline and to take benefit of investment and development opportunities as markets stabilize. During 1H FY20, the company declared distribution of 30 cents per stapled security.

.png)

Key Dates for SPP (Source: Company Reports)

Short-Term Impact on Core Profits:For FY20, the company is expecting a short-term impact on core profit due to reduced productivity in the construction segment.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company possesses a strong balance sheet and debt position. The company expects gearing in the range of 10% – 15% at the end of FY20. Debt to equity of the company stood at 0.60x in 1H FY20 against the industry median of 0.78x. At the current market price of $11.020, annual dividend yield of the stock stands at 5.31%. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of lower double-digit (in percentage terms). Thus, considering the deleveraged balance sheet, recent equity raising and other aforesaid factors, we give a “Buy” recommendation on the stock at the current market price of $11.020 per share, down by 2.391% on 14th May 2020.

LLC Daily Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...