Commonwealth Bank of Australia

.png)

CBA Details

Quarterly Interest Payment: Commonwealth Bank of Australia (ASX: CBA) is a leading provider of retail banking services, business and private banking, institutional banking and markets, ASB New Zealand, wealth management and international financial services. The bank has recently announced that it will pay interest of 3.36% p.a. on HKD $608,000,000 Fixed to Floating Rate Notes which are due on March 30, 2027. The interest payment date is March 30, 2020.

CBA noted the release by Reserve Bank of New Zealand (or RBNZ) with respect to final capital requirements which are applicable to the banks in NZ. RBNZ confirmed that, risk-weighted assets (or RWA) of the internal ratings based banks like ASB Bank Limited, would rise to around 90% of that required under the standardised approach. Moreover, for those banks which are deemed as systemically important (which includes ASB), Tier 1 capital requirement would be increasing to 16% of RWA, out of which 13.5% must be in the form of Common Equity Tier 1 (or CET1) capital. However, Tier 2 capital would remain in the framework, and could comprise 2% of the minimum total capital ratio of 18 percent.

Over the September quarter, excess liquid assets averaged to $32 billion and the average LCR (Liquidity Coverage Ratio) decreased by 2% from 132% to 130% because of higher net cash outflows. During the same period, the group’s leverage ratio stood at 5.5% on an APRA basis. The strength of the bank’s operating and capital performance enabled the Board to declare a final fully franked dividend of $2.31 per share, taking the full year dividend to $4.31 per share.

.png)

Group Leverage Ratio (Source: Company Reports)

Future Expectations: CBA is combining service and technology to deliver exceptional experiences to its customers and is strategisingits digital presence for its growth. In the span of next five years, the bank plans to deploy over $5 billion towards technology in order to keep improving its systems and services, to help keep the customers safe and secure, as well as in order to serve them better.

Valuation Methodology: Price/Book Value Based Approach

.png)

Price/Book Value Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:As at 30 September 2019, CBA’s Level 1 CET1 ratio stood at 11% which is based on CET1 capital of $47.4 billion and RWA (Risk Weighted Assets) of $432.2 billion. In the same time period, Level 2 CET1 ratio was 10.6%. As per ASX, the stock of CBA gave a return of 4.18% in the past 4 months and a return of 2.45% in last one month. The stock is also inclined towards its 52-week high level of $83.990. We have valued the company using Price/Book based valuation, and there are expectations that the stock might see some sort of correction moving forward. In the latest release, the bank has announced that it will release its interim results on 12th February 2020. Considering the aforesaid facts, we have a watch stance on the stock at the current market price of $80.900 per share, down by 0.369% on January 8, 2020.

CBA Daily Technical Chart (Source: Thomson Reuters)

Westpac Banking Corporation

.png)

WBC Details

Reduction in Expenses and Declaration of Dividends: Westpac Banking Corporation (ASX: WBC) provides financial services including lending, payments services, investment platforms, insurance services, leasing finance and other services. The bank has recently declared a dividend of $1.0161 on WBCPG - Cap Note 3-BBSW+4.90% Perp Non-Cum Red T-12-21 which is to be paid on March 30, 2020. The bank in its recent AGM announced that the cost of customer remediation and exiting advice resulted in reduction of cash earnings by around $1.1 billion. However, WBC was able to manage its expenses well and delivered more than $400 million in productivity savings. For the year ended 30 September 2019, Common Equity Tier One capital ratio of WBC stood at 10.67%. and net profit after tax was $6,784 million.

.png)

Financial Performance (Source: Company Reports)

Growth Opportunities: Although, the financial performance of the bank was lower, it has managed to make a good progress on its strategy primarily in improving its technology infrastructure as well as migrating more activity to the digital channels. WBC is expecting softer operating conditions and growth in balance sheet without a significant deterioration in credit quality.

Valuation Methodology: Price/Book Based Valuation

Price/Book Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of WBC is inclined closed to its 52-week low level of $23.860, proffering a decent opportunity for accumulation. In the span of 4 years from FY15 to FY19, WBC witnessed a CAGR of 4.34% in net interest income. Considering the trading levels, CAGR in net interest income and decent outlook, we valued the company using Price/Book Based valuation approach and have arrived at a target upside of lower single digit (in percentage terms). For the said purposes, we have considered Commonwealth Bank of Australia (ASX: CBA), National Australia Bank Ltd (ASX: NAB), Bendigo and Adelaide Bank Ltd (ASX: BEN) and Australia and New Zealand Banking Group Ltd (ASX: ANZ) as peers.Hence, we recommend a “Buy” rating on the stock at the current market price of $24.540, down by 0.325% on January 8, 2020.

.jpg)

WBC Daily Technical Chart (Source: Thomson Reuters)

Wesfarmers Limited

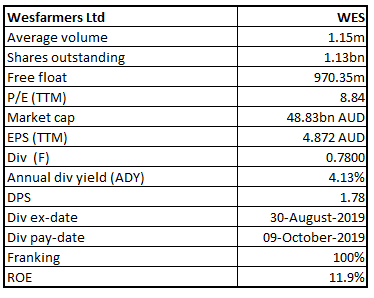

WES Details

Decent Rise in NPAT: Wesfarmers Limited (ASX: WES) is a diversified industrial company with interests including retail operations that covers home improvement and office supplies, general merchandise and specialty departments stores, gas processing and distribution, chemicals and fertilisers, etc. In the recently held AGM, the top management stated net profit after tax rose by 13.5% to $1.9 billion in FY19 from $1.7 billion in FY18. This was mainly due to higher contributions from Bunnings, Officeworks and Industrials and other activities, including the 15% share in Coles Group, more than offsetting a fall in the profits of the Kmart Group. The strengthening performance enabled the Board to declare a fully-franked final dividend of 78 cents per share, bringing the full-year ordinary dividend to $1.78 per share.

Financial Performance (Source: Company Reports)

Growth Opportunities: The company remains optimistic about the outlook for the group and is confident that the investments in the customer offer and new growth platforms would deliver value to shareholders. It also expects that growth in Officeworks’ earnings will be impacted by ongoing investment in price as well as higher team member wages, post implementation of the new enterprise agreement.

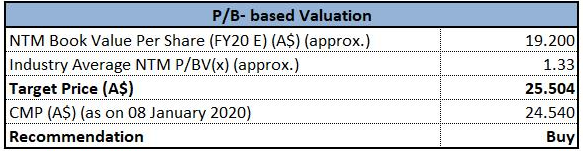

Valuation Methodology: EV/Sales Based Valuation

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of WES gave a return of 16.25% in the last 6 months, a return of 10.52% in the past 3 months and a return of 5.49% in the past one month. The stock is also trading close to its 52-week high level of $43.300. During FY19, net margin of the company stood at 6.9% as compared to the industry median of 12.9%. The company also reported a stability in its balance sheet with Debt/Equity ratio of 0.3x, lower than the industry median of 0.67x. The company is likely to report its results for 1HFY20 on February 19, 2020 and, therefore, we suggest investors to wait for the announcement. We have valued the company’s stock using EV/Sales multiple approach and there are expectations that the stock might witness some correction moving forward. Hence, we have a watch stance on the stock at the current market price of $42.920 per share, down by 0.348% on January 8, 2020.

.jpg)

WES Daily Technical Chart (Source: Thomson Reuters)

Fortescue Metals Group Ltd

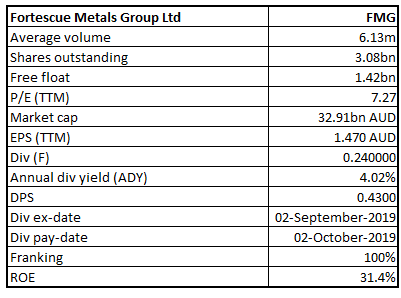

FMG Details

Strong Start to FY20: Fortescue Metals Group Ltd (ASX: FMG) is engaged in mining, processing and transportation of iron ore for export from the company's deposits within Pilbara region of WA. During FY19, underlying EBITDA of the company stood at US$6.0 billion and net profit after tax (or NPAT) amounted to US$3.2 billion. The decent financial performance enabled the Board to pay total dividend of A$1.14 per share, representing a payout ratio of 78% of FY19 NPAT. The company had a strong start to FY20 and the average revenue received stood at US$85/dmt while net debt stood at US$0.5 billion.

.png)

Financial Performance (Source: Company Reports)

Growth Opportunities: The company is building strong relationships with China and has procured over US$1 billion from China. The company has given its capital expenditure guidance and expects it to be around US$2,400 million in FY20. It also expects its C1 cost/wmt to lie in between US$13.25/wmt to US$13.75/wmt.

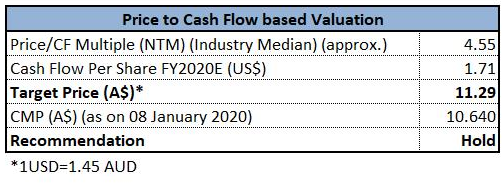

Valuation Methodology: Price/Cash Flow Multiple Approach

Price/Cash Flow Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of FMG gave a return of 19.98% in the past 3 months and a return of 4.29% in the last one month. The stock is trading close to its 52-week high of $11.100. In the span of 4 years from FY15 to FY19, the company has witnessed a CAGR of 43.4% in gross profit. During FY19, net margin of the company stood at 32%, higher than the industry median of 11.7%. In the same period, Return on Equity stood at 31.4% as compared to the industry median of 12.4%. Considering the returns, trading levels, CAGR in gross profit and high ROE, we have valued the stock using Price/Cash Flow Multiple and have arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $10.640, down by 0.468% on January 8, 2020.

FMG Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...