.png)

Stocks’ Details

Transurban Group

Distribution for 1H FY20:Transurban Group (ASX: TCL) owns, operates and develops electric toll roads as well as intelligent transport systems. The market capitalisation of the company stood at A$40.75 Bn as on 2nd January 2020. The company, through a release dated 10th December 2019, announced that Hills M2 Motorway (100% owned by TCL) has successfully raised non-recourse debt amounting to A$403 Mn through a new bank facility with a tenor of 12 months. The funds raised would primarily be utlilised by Hills M2 to refinance an existing bank facility, which would be maturing in March 2020. For the six-months ended 31st December 2019, the company declared a distribution amounting to 31.0 cents per stapled security. This comprises a distribution of 29.0 cent from Transurban Holding Trust and controlled entities and a 2.0 cent fully franked dividend from Transurban Holdings Limited and controlled entities.

Notably, at the current market price of A$14.900 per share, annual dividend yield of the company stood at 4.09%. The following picture provides an idea of EBITDA margins:

.png)

EBITDA Margins (Source: Company Reports)

Expectation of Growth in Distribution:The company is expecting a distribution of 62.0 cents per security for FY20, reflecting growth of 5.1% as compared to the distribution of FY19. The company is anticipating significant opportunities to continue, which might create value for all stakeholders over the long term.

Valuation Methodology: EV/Sales Multiple Approach

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The company would be paying the distribution of 31 cents on 14th February 2020. The near-term priorities of the company revolve around (1) Delivering committed projects, (2) Maximising the performance of operations and (3) Enhancing the customer and community offerings. We have valued the stock using EV/ Sales based relative valuation approach and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Therefore, considering the distribution-related parameters, expected growth in distribution, and expected upside, we give a “Hold” recommendation on the stock at the current market price of A$14.900 per share, down 0.067% on 2nd January 2020.

CIMIC Group Limited

Acquisition by Ventia: CIMIC Group Limited (ASX: CIM) provides construction, mining as well as operation and maintenance services to the infrastructure sector. The market capitalisation of the company stood at A$10.73 Bn as on 2nd January 2020. The company recently announced that Trevor Gerber has ceased to be a Director in the company from 31st December 2019. CIM has recently noted that its 50:50 investment partner, Ventia, has inked an agreement with Ferrovial S.A. to purchase Broadspectrum. However, it is subject to standard conditions and regulatory approvals. The acquisition is for an equity value amounting to A$485 Mn and the combined group is anticipated to generate revenue of more than A$5 Bn. The acquisition is anticipated to be wrapped up in 2020.

For the six months ended 30th June 2019, CIM declared a fully franked interim ordinary dividend amounting to 71 cps, which was paid on 3rd October 2019.At the current market price of A$32.790 per share, the annual dividend yield of the company stood at 4.74%. The following picture provides an overview of NPAT for 1H FY19:

.png)

NPAT (Source: Company Reports)

Strong Pipeline of Opportunities:Subject to market conditions, the company is expecting NPAT for 2019 in the ambit of $790 million to $840 million. The company possesses a strong pipeline of construction, mining and services opportunities for 2020 and beyond. The company is also focused on delivering returns to shareholders, which might help it in garnering attention of the market participants.

Valuation Methodology: P/E Multiple Approach

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The company continues to make progress on its objectives, and the Group remains in a strong financial position. The strong balance sheet of CIM provides flexibility to seek strategic growth initiatives as well as capital allocation opportunities. Net margin of the company stood at 5.3% in 1H FY19 as compared to the industry median of 3.7%. This reflects that the company has decent capabilities to convert its topline into the bottom line as compared to the broader industry. We have valued the stock using P/E-based relative valuation approach and arrived at a target price, which is offering an upside of higher single-digit (in percentage terms). Therefore, considering the decent financials for nine months to 30 September 2019, a strong balance sheet, along with expected upside in the stock price, we give a “Buy” recommendation on the stock at the current market price of A$32.790 per share, down 1.056% on 2nd January 2020.

Telstra Corporation Limited

Decent Returns to Shareholders:Telstra Corporation Limited (ASX: TLS) provides telecommunication and information services, which include mobiles, internet and pay television. The market capitalisation of the company stood at A$42.1 Bn as on 2nd January 2020. The company recently stated that the T22 strategy is performing multiple jobs, which includes delivering cost reductions and simplifying its business. The mobile business of the company is continuing to return to a more rational market as the company goes through the evolution of 5G. In NAS, Telstra is on track to achieve mid-teens profit margins via a focus on cost reductions as well as profitable NAS products.

For FY 2019, the Board of the company declared a final dividend of 8 cps, fully franked. This comprised of a final ordinary dividend amounting to 5 cps and a final special dividend of 3 cps. When combined with total interim dividend, which was paid in the month of February 2019, the total dividend comes out to be 16 cents per share for FY19.

Expectation of Fall in Direct Labour Costs: On the Income front, the company would experience impact from the accounting for its loyalty program, Telstra Plus, in 1H FY20 results. This would defer around $150 million of the income. The direct labour costs would continue to fall in FY20. The following picture provides an idea of FY20 guidance:

.png)

Revised FY20 Guidance (Source: Company Reports)

Valuation Methodology: Price/Earnings Multiple Approach

.png)

Price/Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:Gross margin of the company stood at 63.8% in FY19 as compared to the industry median of 61.0%. Return on equity of the company stood at 14.8% in FY19 against the industry median of 5.7%. This reflects that the company has provided decent returns to the shareholders in FY19 in comparison to the peer group. We have valued the stock using P/E-based relative valuation approach and reached at a target price, which is offering an upside of higher single-digit (in percentage terms). Hence, considering the company’s target to reduce annual underlying fixed costs by $2.5 billion by FY22, favourable valuations, and decent dividend-related parameters, we maintain a “Hold” rating on the stock at the current market price of A$3.580 per share, up 1.13% on 2nd January 2020.

Contact Energy Limited

A look at November Month Report:Contact Energy Limited (ASX: CEN) is engaged in generation and retailing of electricity and has a market capitalisation of A$4.99 Bn as on 2nd January 2020. The company recently announced that it would be releasing its 1H FY20 (six months ended 31st December 2019) results on 10th February 2020. The Customer business of the company has recorded mass market electricity and gas sales of 313 GWh and mass market electricity and gas netback of $90.48/MWh in the month of November 2019. Notably, the Wholesale business reported contracted wholesale electricity sales, including which sales to the Customer business, totalled 596 GWh.

During FY19, the company has declared a full-year dividend amounting to 39 cps.At the current market price of A$6.945 per share, the annual dividend yield of the company stood at 5.03%. The following picture provides an overview of dividend declared in the past years:

.png)

Dividends (Source: Company Reports)

Target to Maintain Consistency in Dividend:As per 2019 Annual Report, the company is focused on decreasing operational expenses for taking costs out of the Customer business. However, at the same time, the company is focused towards developing new products, improving customer experience as well as selectively deploying resources for robotics and automation. Despite the variable hydrology, costs to maintain its plant, and volatile market conditions, CEN targets to maintain consistency in the dividend.

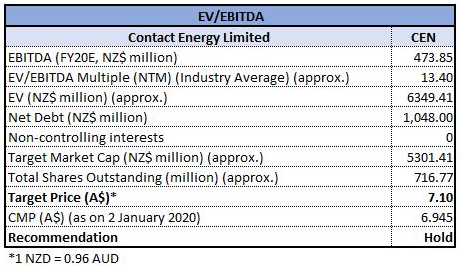

Valuation Methodology:EV/EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:For FY20, the company is targeting ordinary dividend amounting to 39 cps. Current ratio of the company stood at 0.76x in FY19 as compared to 0.70x in FY18. This reflects that the company has improved its position to address its short-term obligations. Debt to equity of the company stood at 0.39x in FY19 as compared to the industry median of 0.44x. During the span of one month, the stock of CEN provided a return of 2.74% and 23.36% on a YTD basis. We have valued the stock using EV/EBITDA based relative valuation method and arrived at the target price which is offering an upside of lower single digit (in percentage terms). Therefore, considering the decent liquidity position, stable balance sheet, returns in the past period, and the expectation of maintaining consistency in its dividend, we maintain a “Hold” rating on the stock at the current market price of A$6.945 on 2nd January 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...