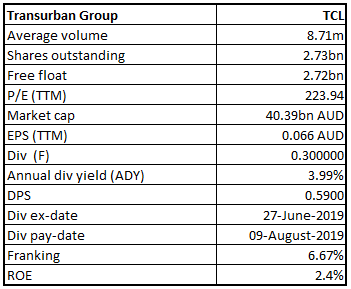

Transurban Group

TCL Details

Annual General Meeting to be held on 10 October 2019:Transurban Group (ASX: TCL) is engaged into the building and operation of toll roads in Sydney, Melbourne and Brisbane, Australia, as well as in the Greater Washington Area and Montreal in North America. It has a market a capitalisation of ~A$40.39 bn as on 3rd October 2019. The company would be conducting its 2019 Annual General Meeting on 10th October 2019. In another update, the company announced that it has issued 21,312,335 securities at the consideration amounting to $14.64. The objective for the issue of securities is to finance the acquisition of the remaining interest in M5 West and for general corporate purposes.

As per the release dated 7th August 2019, for the six-months ended 30 June 2019, the company declared a distribution amounting to 30.0 cents per share, which was paid on 9th August 2019. This consisted of 28.0 cps distribution from Transurban Holding Trust and controlled entities as well as a fully franked 2.0 cps dividend from Transurban Holdings Limited and controlled entities.At the current market price of A$14.540 per share, the annual dividend yield of the company stands at 3.99%, which is in line with the industry average (Industrials) of 3.9% on TTM basis. The following picture provides an overview of proportional results for the year ended 30th June 2019:

.png)

Proportional Results (Source: Company Reports)

What to Expect:The company expects various opportunities to continue creating value for all stakeholders over the long term. The company stated that the four projects have been open to traffic and a further three forecast to complete progressively by the end of 2020. The company expects FY20 distribution of 62.0 cps, reflects a growth of 5.1% as compared to the distribution of FY19.

Stock Recommendation:On the valuation front, the enterprise value to EBITDA ratio of the company stood at 28.2x on TTM basis as compared to the industry average (Transport Infrastructure) of 67.0x. When it comes to the stock’s past performance, TCL provided returns of 12.05% in the time span of six months. However, on a YTD basis, it generated a return of 27.97%. Hence, considering the above-stated facts and current trading levels, we give a “Hold” recommendation on the stock at the current market price of A$14.540 per share (down 1.624% on 3rd October 2019).

TCL Daily Technical Chart (Source: Thomson Reuters)

Sydney Airport

.png)

SYD Details

Changes to the Board and Compliance Committee:Sydney Airport (ASX: SYD) is a large-cap company with the market capitalisation of ~A$18.29 bn as on 3rd October 2019. As per the release dated 27th September 2019, the Trust Company (Sydney Airport) Limited the Responsible Entity of Sydney Airport Trust 1 (SAT1) advised that Eleanor Padman has resigned as Director of the Responsible Entity. Chris Green has resigned as an alternate Director for Eleanor Padman for the Responsible Entity. It was mentioned that Anne Rozenauers has been appointed as a Director of the Responsible Entity. Michael Vainauskas has resigned as a member of the compliance committee of the Responsible Entity and appointed Simone Mosse as a member of the compliance committee of the Responsible Entity. The following picture gives an idea of traffic performance for the month of August 2019:

.png)

Traffic Performance (Source: Company Reports)

As per the half-yearly results report, the company declared distribution per stapled security, amounted to 19.5 cents, which was paid on 15th August 2019. At the current market price of A$7.950, the annual dividend yield of the company stands at 4.75% against the industry median (Industrials) of 3.6%.

Future Aspects: The company expects 2019 distribution at 39.0 cents per stapled security, reflecting a growth of 4.0% on 2018 distribution and 5-year CAGR growth of 10.7%. The distribution is anticipated to be more than fully covered by net operating receipts throughout the full-year, subject to aviation industry shocks and material forecast changes.

Stock Recommendation:The company has continued to strengthen its balance sheet and credit metrics, with its cashflow cover ratio increasing to 3.2x against 3.1x for the pcp. On the valuation front, the company reported EV/EBITDA of 21.7x as compared to the industry median (Industrials) of 6.9x on a TTM basis. The enterprise value to sales ratio stood at 17.4x against the industry median (Industrials) of 1.6x on a TTM basis. As per ASX, the stock trading towards its 52-week higher levels of $8.69 with PE multiple of 45.87x. Hence, in light of aforesaid facts and current trading levels, we advise the investors to closely watch the stock at the current market price of A$7.950 per share (down 1.852% on 3rd October 2019) and wait for better entry levels.

.

SYD Daily Technical Chart (Source: Thomson Reuters)

Aventus Group

.png)

AVN Details

September 19 Quarter Distribution Reinvestment Plan: Aventus Group (ASX: AVN) provides property investment, management, leasing and development services to owners of large format retail property assets. The market capitalisation of the company stood at A$1.48 bn as on 3rd October 2019. Recently, the company updated the market with September 19quarter distribution reinvestment plan in which it stated that earlier AVN announced that it would pay a distribution of 4.22 cents per stapled security in respect of the quarter ending 30 September 2019. The payment date for the distribution is 31st October 2019.

It was also mentioned that AVN has entered into an underwriting agreement with Macquarie Capital (Australia) Limited, wherein, AVN would act as the sole underwriter of an offer of stapled securities in Aventus Group under the group’s DRP. Macquarie Capital (Australia) Limited will underwrite the entire DRP offer up to around $23.1 Mn at the DRP underwritten price which would be calculated using mechanism and pricing period as set out in AVN DRP rules and distribution announcement, less the discount of 2%. At the current market price of A$2.710 per share, the annual dividend yield of the company stands at 6.19% in comparison to the industry median (Financials) of 4.6% on a TTM basis.

Future Priorities:The company stated that its core strategy of delivering organic growth via intensive asset management remains clear and drives real results. For the upcoming 12 months, the company is focused to actively diversify its tenant base with a priority on increasing everyday-needs to continue to drive weekday traffic and energise its centres. It is also focused on maintaining disciplined capital management to allow for the execution of its strategy. The company expects to witness a rise in FFO per security in the range of 3 – 4%, which is equal to 19.0 – 19.2 cents per security for FY20 considering continued momentum from the portfolio.

Distribution Per Security (Source: Company Reports)

Stock Recommendation:The gross margin and EBITDA margin of the company stood at 78.8% and 67.7% in FY19, reflecting YoY growth of 3.6% and 17.5%, respectively. As per ASX, the stock is trading at the P/E multiple of 12.80x against the industry median (Financials) of 14.7x on a TTM basis. The price to book value of the company stood at 1.1x as compared to the industry median (Financials) of 1.2x. On the stock’s performance front, it generated returns of 16.88% and 20.00% in the time frame of three months and six months, respectively. Hence, considering the aforesaid facts, we give a “Hold” rating on the stock at the current market price of A$2.710 per share (up 0.37% on 3rd October 2019).

.png)

AVN Daily Technical Chart (Source: Thomson Reuters)

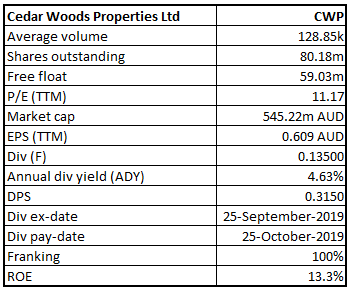

Cedar Woods Properties Limited

CWP Details

Update on Acquisition:Cedar Woods Properties Limited (ASX: CWP) is property investors and developers with a market capitalisation of ~A$545.22 Mn as on 3rd October 2019. Recently, the company with the help of a release dated 19th September 2019 announced that it has inked a conditional contract to acquire 179 Erindale Rd, Hamersley, Western Australia for the consideration of $21.2 Mn, plus GST from Broadcast Australia. It added that the acquisition remains conditional on the vendor obtaining town planning and environmental approvals, de-risking these steps for CWP. This opportunity sees CWP achieve its third acquisition over the past 12 months.

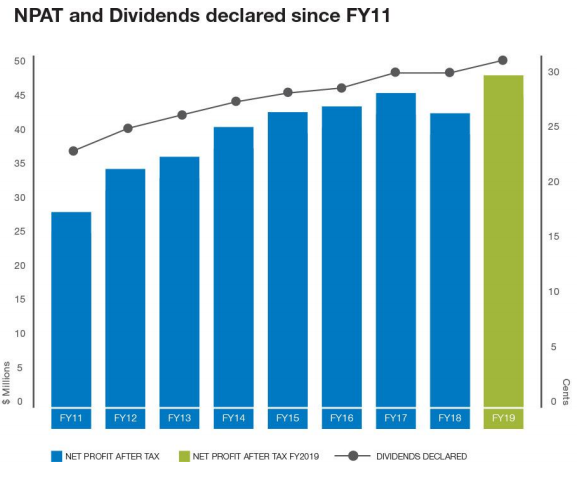

The total dividend for FY19 stood at 31.5 cps, reflecting a rise of 5%. At the current market price of A$6.800 per share, the annual dividend yield of the company stands at 4.63%, which is slightly below the industry median (Financials) of 4.7% on TTM basis.

NPAT and Dividends (Source: Company Reports)

Future Priorities:Considering current market conditions, the company expects moderately lower full- year earnings in FY20 against FY19. CWP happens to be well-positioned for the medium term with more than 9,000 undeveloped lots/units in its development pipeline throughout four states, with the ability to respond quickly to improved market conditions. Several new projects are anticipated to contribute to earnings from FY21, which include Huntington apartments in Victoria, Ariella (adjoining parcel) and Solaris in Western Australia, and Wooloowin in Queensland.

Stock Recommendation: The company produced returns of 19.51% and 27.10% in the span of three months and six months, respectively. Currently, the stock is trading towards its 52-week high price of $7.27 with PE multiple of 11.17x. Thus, considering the above-stated facts and current trading levels, we give a “Hold” rating on the stock at the current market price of A$6.800 per share on 3rd October 2019.

CWP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...