Westpac Banking Corporation (ASX: WBC)

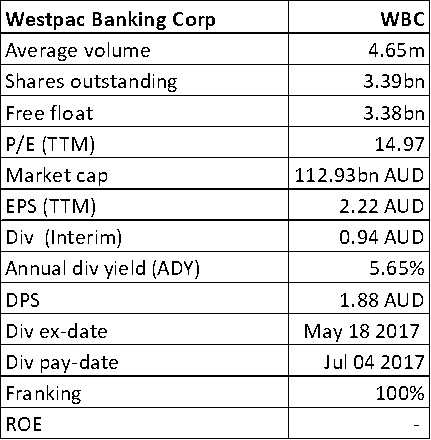

WBC Details

Sailing through a challenging phase: Westpac’s stock slipped by 2.2% on November 06, 2017 while the group announced its full year results with a 7% rise in statutory profit to 7.9 billion and 3% rise incash earnings to $8.06 billion at the back of 6% growth in Australian mortgages. Further, 4% rise in earnings from the consumer division supported the growth in cash profit for the year while Market and Treasury suffered softness in 2H17. The group has managed to grow its loan book while meeting the new macro-prudential regulatory requirements on investor and interest only lending. The group’s strategy is said to have gained momentum with the result in a challenging environment. The group’s common equity tier one capital ratio has moved up to 10.6% well ahead of the January 2020 deadline to meet the Australian Prudential Regulation Authority’s 10.5% benchmark.

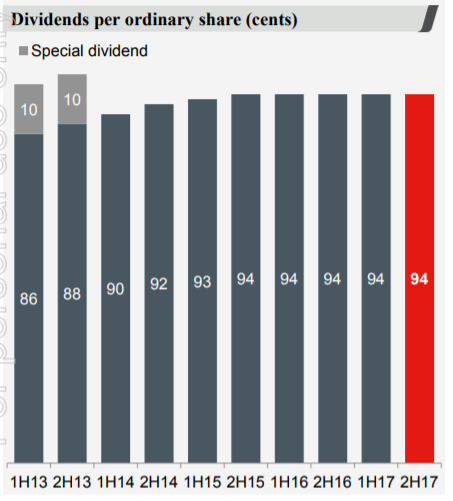

Dividend Trend (Source: Company Reports)

On the other hand, the stock seems to have been impactedfrom the BT Financial business that includes superannuation and insurance.Animpact of about $118 million from refunds and payments to super customers lost out due to unsatisfactory disclosure practices, package customers who did not receive benefits to which they were entitled, and others who did not receive on-time advice to which they were entitled, was identified. Further, an impact of about $95 million pre-tax owing to the government bank levy was also highlighted. The group has signalled for slow growth in Australia through 2018 at the back of softness in income growth, construction trends and house prices. Given the limitations, we believe that the stock is still “Expensive” at the current price of $32.55

.png)

WBC Daily Chart (Source: Thomson Reuters)

Telstra Corporation Ltd (ASX: TLS)

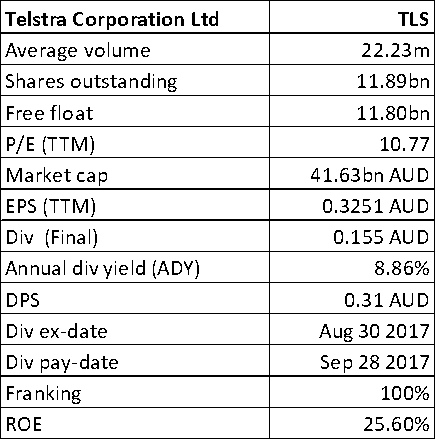

TLS Details

Evolving in terms of technology: Telstra has lately signalled for challenging economics of the national broadband network while the group remains committed to be the market leader, at its investor day conference. The group expects a hit on earnings with NBN rollout completion, primarily a $3 billion loss in earnings, at the back of wholesale prices on the NBN that leave thin margins for retailers offering services on the network. However, dynamics are said to improve gradually. A downward pressure is also indicated with respect to the growing number of resellers of NBN services. Further, Telstra has been buying bandwidth on the NBN that is sufficient to meet customer demand. Increased competition and weakness in fixed-line margins are also weighing on the stock. On the other hand, the group plans to focus on 5G and Internet of Things (IoT), to provide better services delivered over its mobile network. The group now aims to evolve in terms of a more digitally sensitized telecom player with a technology-driven vision and this can help maintain a competitive advantage. Aligning with this, the group intends to benefit from the Internet of Things, 5G mobile and Big Data; while an investment of over $1 billion is expected on digitisation and $500 million in improving customer experience. Recently, Telstra hailed over ACCC announcement on not declaringmobile roaming, benefitting customers in regional Australia. Amidst the developments, we put a “Hold” on the stock at the current price of $3.49

.png)

TLS Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd (ASX: NAB)

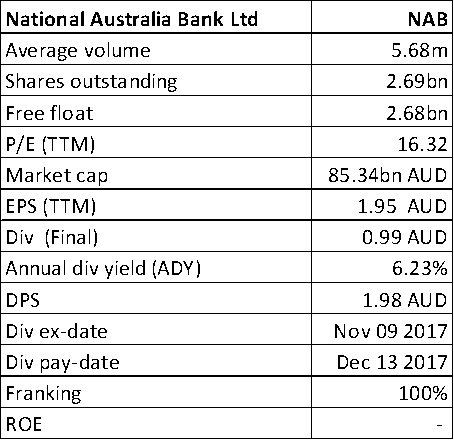

NAB Details

Investing to enhance digital capabilities and automation: National Australia Bank witnessed a full year FY17 cash profit growth of 2.5% to $6.642 billionand 2.7% rise in net operating income, with growth in both housing and business lending.The bank kept the dividend flat though.

Cost Savings (Source: Company Reports)

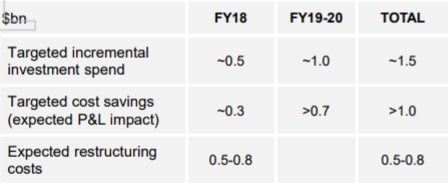

On the other hand, the bank aims to cut 4,000 jobs over the next three years through FY20, as part of a $1.5 billion restructure based on digitisation plans. While these initiatives are said to benefit the group in the long-term to gain traction for providing improved customer services, the group’s expenses have risen 2.6% and one-off impairment as a result of the restructure of between $500 million and $800 million in the first half of the 2018 financial year has been indicated. Nonetheless, NAB expects to save more than $1 billion in costs by the end of the 2020 financial year based on the initiatives. The group aims to treatits people with care and respect and equip them for the future. Further, the bank has indicated for no dividend cuts for at least the current financial year at the back of the ongoing efforts.NAB has recently announced about settling the Bank Bill Swap Rate (BBSW) legal action with the Australian Securities and Investments Commission (ASIC) while the stock has moved up 15.4% in last one year, as at November 03, 2017. Awaiting any positive developments on the bank’s new initiatives, we maintain a “Hold” on the stock at the current price of $31.56

.png)

NAB Daily Chart (Source: Thomson Reuters)

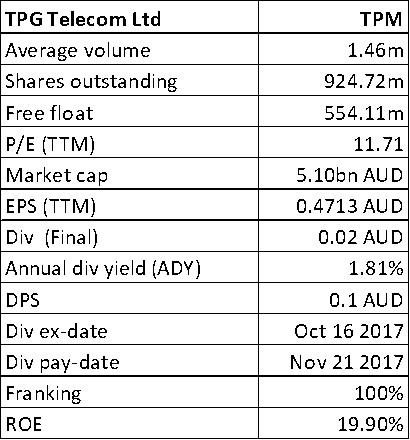

TPG Telecom Ltd (ASX: TPM)

TPM Details

Relying on strength in core business: TPG’s stock was up 4.17% on November 06, 2017 with positive sentiments building on the group again. For FY17, TPM’s reported NPAT was up 9.01% while revenue from ordinary activities were up 4.31% over FY16 and earnings (EBITDA) rose by 5%. The group is focussing on its spectrum commitments and planned mobile network builds. Accordingly, the $735m of undrawn debt facilities at the year-end were raised in order to have total committed debt facilities of $2,385m by September 2017. However, the full year dividends were 10 cents compared with 14.5 cents of last year.

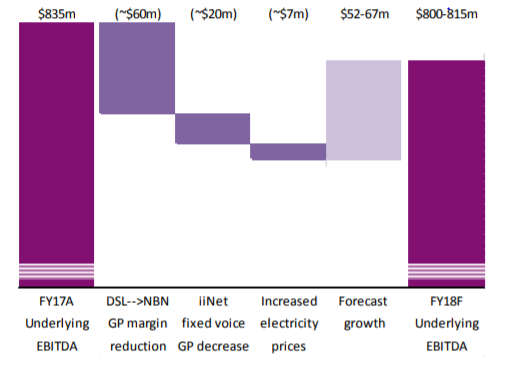

FY18 EBITDA as forecasted (Source: Company Reports)

While NBN margin is expected to erode earnings, decent performance is still expected for FY18 given the group’s core strengths. Efforts on cost control across the business and cash conversion capability, along with tracking of mobilerollouts in Singapore and Australia from both capex and timing perspectives seem to help the group amid a challenging environment. We maintain a “Buy” at the current price of $5.75

.png)

TPM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...