Stocks’ Details

CSL Limited

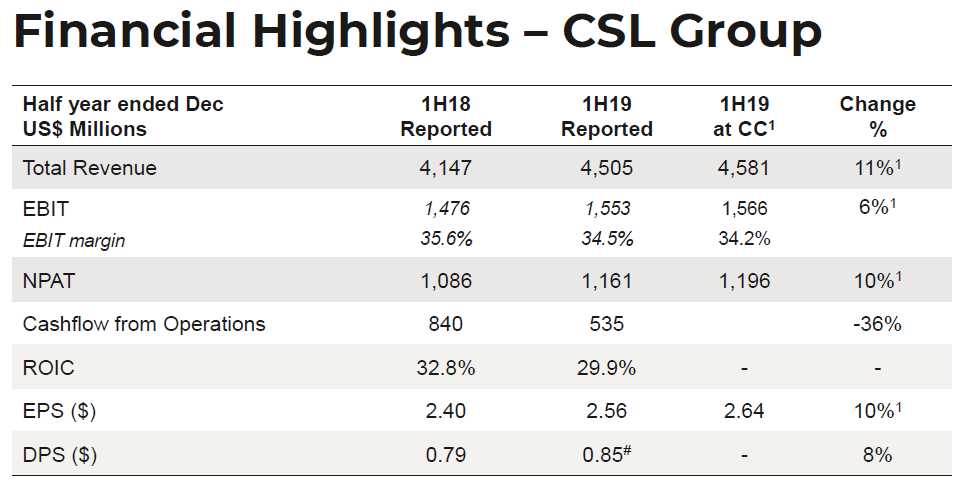

Margins Contraction Witnessed: CSL Limited (ASX: CSL) stated that it will pay an ordinary dividend of AUD 1.20317500, the record date for which was March 14, 2019 and the payment date shall be April 12, 2019. Also, the company has declared its 1H19 results where it reported a double-digit profit growth. It reported sales revenue of $4,505 million, up 11% in constant currency terms on pcp basis. This rise was primarily driven by increased usage of immunoglobulin products for chronic therapies, sales of transformational Hereditary Angioedema (HAE) product and increased sales of adjuvanted influenza vaccine.

Further, the management assumes that there would be sustained demand for plasma and recombinant products.

1HFY19 Financial Highlights (Source: Company Reports)

What to Expect From CSL: The company expects NPAT for FY19 to be in the upper-end range of approximately $1,880 to $1,950 million in constant currency terms. The company expects 30 to 35 new collection centres moving forward and this plan is on track.

The firm delivered a fall in ROE to 26% for the 1H 19 vis-a-vis 31% in the pcp. In the meantime, the stock price has fallen 4.40% in the past six months. However, the company’s stock is trading slightly towards the 52-week higher level and thus, we might say that the current price has discounted the key growth catalysts. As a result, we maintain our “Expensive” recommendation on the stock at the current market price of A$194.440 per share (up 0.444% on 20 March 2019).

Reliance Worldwide Corporation Ltd

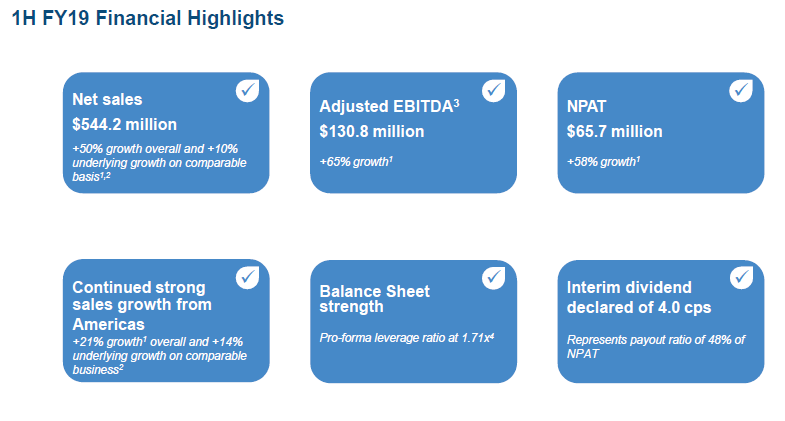

Strong EBITDA Growth & Improving Balance Sheet: Reliance Worldwide Corporation Ltd (ASX: RWC) has lately announced that Macquarie Group ceased to be a substantial holder of the group since 1 March 2019. RWC’s net sales for the half year ended 31 December 2018 was $544.2 million, implying a rise of 50% on the comparative period. The company’s reported EBITDA for the period was $120.7 million, an increase of 52% on the comparative period. These raises in financial performance are suggestive of the inclusion of the contribution from John Guest for the entire period.

RWC’s Financial Highlights (Source: Company reports)

What to Expect From RWC: As per the management, the outlook for 2H FY2019 is robust enough. The management anticipates John Guest growth to accelerate in the second half, inconsistency with the historic pattern. The lower cost copper (brass bar) to be processed in the second half, is expected to reduce the production costs. Also, there would be an acceleration of John Guest related synergies.

On the analysis front, the company has substantially deleveraged its balance sheet, as the debt-equity has been reduced to 0.37x for the 1HY ended 31 December 2018 from the levels of 1.17x reported in the pcp. Moreover, the company delivered robust EBITDA margins of 22.2% in the half-year ended December 2018, depicting the efficiency gained through operational leverage.

Meanwhile, the stock price has fallen 15.90% in the last six months and is trading pretty close to a 52-week lower level making it a decent buy opportunity. Hence, considering the company’s focus on deleveraging its balance sheet, robust EBITDA growth over pcp for HY19 and decent price levels, we reiterate our “Buy” recommendation on the stock at the current market price of $4.590 per share.

Nearmap Limited

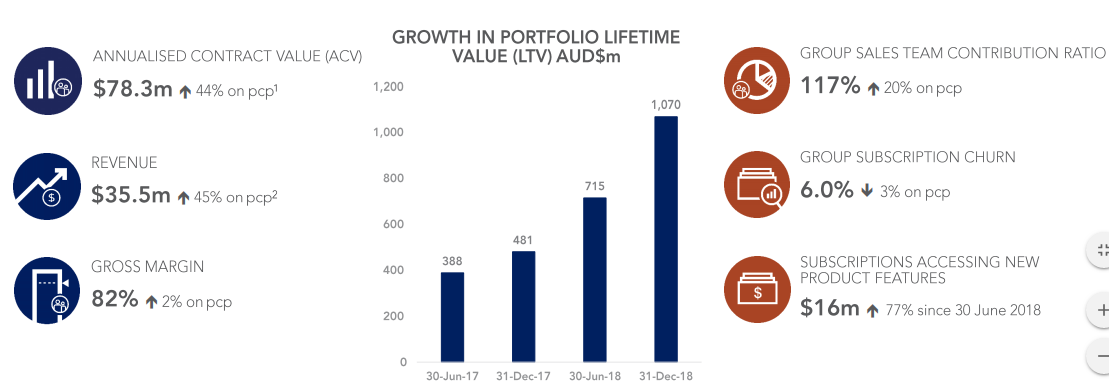

Robust growth in ACV:Nearmap Limited (ASX: NEA) lately posted its H1 FY 2019 numbers whereby, the Annualised contract value (ACV), which is considered the key growth metric, has grown strongly during the period. The ACV grew ~44% on the pcp which was on the back growth in ANZ and the US. The group’s 12-month churn ratio fell to 6% as compared to 7.5% (FY 2018), depicting the company’s continued focus on customer experience and retention.

NEA ‘s Key Financial Metrics (Source: Company Reports)

What to Expect From NEA: As regards the outlook, the company has stuck to its earlier stated guidance for FY19 to become cash flow break even excluding the effect of any capital raise. The company is Australian business is building on the market leadership and is gaining ample traction in its US business. The company is very well positioned & has got a unique business model for the long-term growth as the world market for the Geospatial mapping is expected to see expansion at a robust rate and thus expected to reach US$ 10.10 Bn in 2020.

Meanwhile, the stock price has risen by 53.89% over the past six months. Hence, considering the strong traction which the company’s U.S. business is witnessing coupled with decent growth encountered by the company’s ACV, we, therefore, maintain our “Hold” recommendation on the stock at the current market price of $2.700 per share (down 2.527% on 20 March 2019).

Nanosonics limited

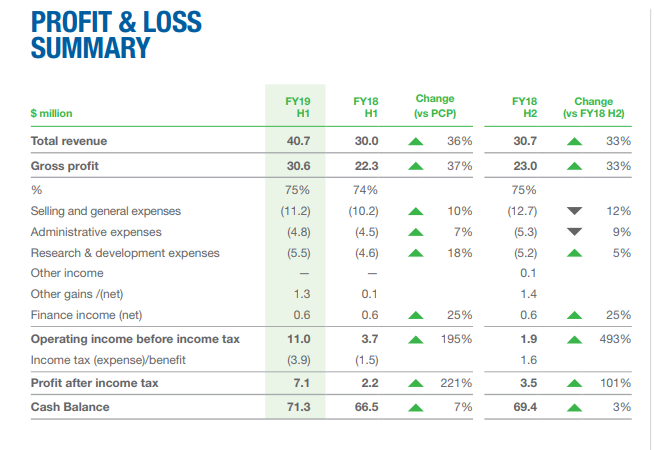

Robust top line growth: Nanosonics Limited (ASX: NAN) has lately reported that Mr Maurie Stang, Non-Executive Chairman of Nanosonics completed an on-market sale of 1,250,000 ordinary shares in the company. Following the sale, Mr Stang continues as one of Nanosonics’ largest shareholders with 18,946,517 ordinary shares representing 6.3% of the Company’s issued share capital. For the HY ended 31 December 2018, the company registered record first half sales of $40.7 million up 36% on pcp and 33% on prior half. This was on the back of a substantial share of capital revenue of $16.4 million which was up 11% on pcp.

The free cash flow for the half was $1.6 million compared with $3.9 million in the pcp. Cash flow for the half year was impacted by an increase in inventory of $3.2 million associated with the launch of trophon®2 and an increase in trade and other receivables.

NAN’s Financial Snapshot (Source: Company Reports)

What to Expect From NAN: Going further for FY 2019, the company’s strategic growth agenda continues to be focussed on establishing the Trophon technology as the standard of care in those markets where Trophon is already represented, expanding into new markets as the fundamentals for adoption strengthen with the release of new guidelines and to develop new products focussing on unmet needs in infection prevention.

Meanwhile, if we look at the past six months’ performance, the stock has delivered decent return of 38.06%. However, considering the decent outlook & the decent return given by the company’s stock, we maintain our “Hold” recommendation on the stock at the current market price of $4.340 per share (up 1.402% on 20 March 2019).

.PNG)

Stock Price Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...