Oil Search Limited

.png)

Stocks’ Details

Strong Operating Cash Flows With Higher Cash Balance: Oil Search Limited (ASX: OSH) is engaged in the business of exploration for oil and gas fields and the development and production of such fields. In early April, a Gas Agreement was signed between the PRL 15 JV (Joint Venture) and the PNG Government, defining the fiscal framework for developing Papua LNG Project. This has allowed FEED (Front-End Engineering and Design) related activities for the upstream component of Papua LNG to commence. After completing Papua LNG Gas Agreement, OSH will focus now to finalise P’nyang Gas Agreement and targets to sign in the 2Q 2019.

Financial Performance in 1Q 2019: Total production in 1Q 2019 at 7.25 mmboe at an annualised rate of 8.8 MTPA (28% above nameplate capacity) reflected a continued strong performance by the PNG LNG Project which was partially offset by lower oil field production. Total revenue for the quarter at US$398.1 million was down 21% as compared to the fourth quarter of 2018, driven by timing of LNG shipments.

Additionally, average realised oil and condensate prices at US$62.35 per barrel were down 3% as compared to 4Q 2018. Average realised LNG and gas prices posted a 7% decline to US$10.15/mmBtu.

.png)

Sales Summary (Source: Company Reports)

In Q1 FY 2019, the company produced 7.25 million barrels of oil equivalent (mmboe), with daily production rate similar to 4Q 2018.Oil Search ended the 2019 first quarter with liquidity of US$1.46 billion, comprising US$789.5 million in cash and US$670.7 million in undrawn corporate credit facilities.

Capital Management: Thedebt outstanding for OSH for the quarter was US$3.42 billion, including US$3.29 billion under the PNG LNG project finance facility and US$130 million drawn from the Company’s corporate facilities. In addition, the company utilised LOC (Letters of Credit) amounting to US$99.3 million to provide early access to some of the cash escrowed in PNG LNG accounts, which otherwise would be distributed in June 2019. The management expects to repay the debt drawn down under the corporate credit facility in the second quarter.

Overall capex incurred on exploration and evaluation activities for OSH in the quarter stood at US$85.1 million. Development expenditure in 1Q FY19 came in at US$6.0 million including US$4.1 million on the PNG LNG Project. Expenditure on producing assets was recorded US$13.4 million, while property, plant and equipment saw an expenditure of US$6.2 million.

What to Expect: Themanagement expects total production in FY19 to be in the range of 28.0 – 31.5 mmboe with the total capital cost at US$545 – 655m.

Stock Recommendation: At current market price, the stock is trading at price to earnings multiple of 23.740x with market capitalisation at ~$11.76 billion and annual dividend yield at 1.98%.

With the strong performance of PNG LNG project, signed agreement for Papua LNG Project, prudent capital expenditure with strong financials, we maintain our “Buy” recommendation on the stock at the current market price of $7.440 per share (down 1.195% on 07 May 2019).

Reliance Worldwide Corporation Limited

Acquisition of John Guest, A Strategic Fit: Reliance Worldwide Corporation Limited (ASX: RWC) is a global market leader and manufacturer in the space of water delivery, control and optimization system. The acquisition of John Guest in 2018 brought geographic diversification for RWC. The combined entity now stands with 15 manufacturing facilities, 24 distribution centres and 5 research & Development locations across America, Asia Pacific and EMEA operating segments. The company recently updated that Firetrail Investments has become a substantial holder with a voting power of 5.09%.

Financial Performance in 1H FY19: Net sales in 1H FY19 at $544.2 million witnessed strong growth of 50.1% (pcp) with reported EBITDA growth at 52.3% to $120.7 million, primarily driven by the inclusion of John Guest for the entire period. Reported net profit after tax at $65.7 million also witnessed strong growth of 58.4% on the comparative period.

.png)

1H FY19 Consolidated Results (Resource: Company Reports)

What To Expect From RWC: Going forward, management expects the outlook for the second half to be strong. Consistent with the historic pattern, John Guest growth is expected to accelerate in 2H FY 2019. Themanagement also expects lower cost copper (brass bar) to be processed in the second half, thus, reducing production costs for the company.

Stock Recommendation: Considering the accelerated growth coming from the synergy with John Guest, expanded geographical presence with a strong distribution network, strengthened product line, strong financials, etc., growth opportunities in the long run seems intact leading us to give a “Buy” rating on the stock at the current market price of $4.610 (down 1.706% on 07 May 2019).

carsales.com Limited

Strong Growth In Top-Line And Bottom-Line Continued: carsales.com Limited (ASX: CAR) is the largest online automotive, motorcycle and marine classifieds business in Australia with network operations across Asia Pacific Region. The company has appointed David Wiadrowski as a Non-Executive Director to its Board of Directors and Chair of its Audit Committee with effect from 23 May 2019. The revenue in the first half of FY19 recorded a pcp growth of 17% to $235 million (3% growth in revenue excluding SK Encar acquisition).

Dealer, Private as a revenue break-up under online advertising and Data, Research & Services businesses performed well whereas there was weaker revenue performance in Display and Finance segments in a large part because of the challenging market conditions. The group margins at 41.7% in 1H FY19 was lower as compared to 45.4% in H1 FY18, with domestic core business margin expansion offset by a decline in Stratton margins.

.png)

Strong Track Record of Financial Performance (Source: Company Reports)

What To Expect from CAR: The management expects domestic adjacent businesses of tyresales and Redbook Inspect will continue to build scale. On the International front, management expects strong local currency revenue and earnings growth in Brazil in H2 FY19 to be continued.

Stock Recommendation: At the current market price of $13.710, the stock is trading at P/E multiple of 23.890x. Considering the above-mentioned factors and growth outlook, we retain our “Buy” rating on the stock at the current market price of $13.710 (up 2.466% on 07 May 2019).

Scentre Group

AUM at $54.2 billion as on FY18: Scentre Group (ASX: SCG) is the owner and operator of Westfield in Australia and New Zealand. It encompasses ~11,500 outlets and total AUM (assets under management) of $54.2 billion as on FY18. The company recently updated about the change of interests of the substantial holder- The Vanguard Group, Inc. with present voting power at 10.278% from earlier 9.274%.

The company recently released its quarterly operating update for the first quarter of FY19. Total specialty in-store sales saw a growth of 1.5% for 1Q FY19. On a sales/square metre basis, total stable portfolio in-store sales witnessed a growth of 1.1% whereas total specialty in-store sales grew 0.7% for 1Q FY19.

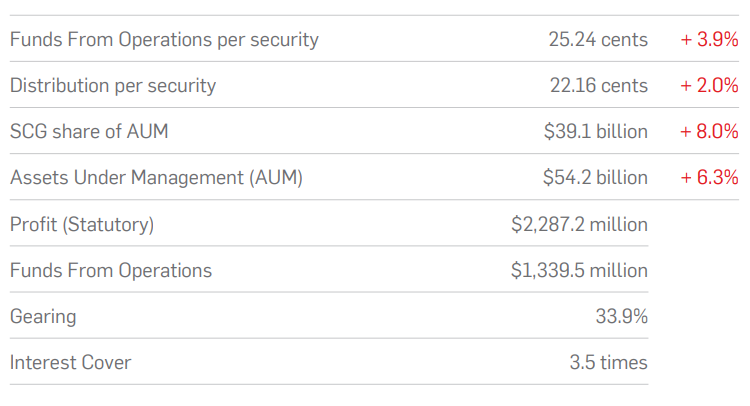

Financial Performance in FY18:The company recorded FFO (Funds from Operations) of $1.34 billion representing 25.24 cents per security, up 3.9% with a distribution of 22.16 cents per security, up 2%.

FY18 Results (Source: Company Reports)

Outlook: The management had forecasted the FFO growth at ~3% for FY19. The distribution for FY19 is expected at 22.60 cents per security, a rise of 2%.

Stock Recommendation: At the current market price of $3.690, the annual dividend yield for the stock comes in at 6.01% with market capitalization at ~$19.99 billion.For FY18, the company witnessed liquidity of $2.1 billion, gearing at 33.9%, interest coverage at 3.5x and interest rate hedging at 69%.

The management reconfirmation about the FFO growth at ~3% along with above-mentioned facts leads us to give a “Buy” recommendation on the stock at the current market price of $3.690 per share.

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...