.png)

Stocks’ Details

Coca-Cola Amatil Limited

Decent Top-line Growth in All Segments: Coca-Cola Amatil Limited (ASX: CCL) is engaged in manufacturing, marketing and distribution of beverages with a market capitalisation of $7.25 Bn as on 17th March 2020. For the full-year ended 31st December 2019, the company has reported a rise of 6.7% in group revenue, which reflects the impact of its business initiatives throughout each market. During the period, every business segment of CCL has delivered growth in the top-line, which includes the Australian business which reported first full-year revenue growth since 2012.

.png)

NPAT (Source: Company Reports)

Withdrawal of 2020 Guidance: Considering the uncertainty with respect to the duration and impact of the COVID-19 pandemic, the company has suspended its guidance which includes the expectation of mid-single-digit earnings per share growth in 2020 as well as in the medium-term.

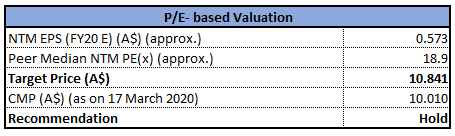

Valuation Methodology: P/E Multiple Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company declared an unfranked final dividend of 26.0 cents per share for FY19, which reflects a full year ongoing payout ratio of 86.4%. Return on equity of CCL stood at 23.7% in FY19 as compared to the industry median of 10.6%. We have valued the stock using P/E based relative valuation method, and for the purpose, we have taken peers such as Treasury Wine Estates Ltd (ASX: TWE), Wesfarmers Ltd (ASX: WES), Coles Group Ltd (ASX: COL), etc., and arrived at a target price, which is offering an upside of high single-digit (in percentage terms). Hence, considering the decent returns paid to shareholders and performance in FY19, we maintain a “Hold” rating on the stock at the current market price of $10.010 per share, down by 0.1% on 17th March 2020.

Woolworths Group Limited

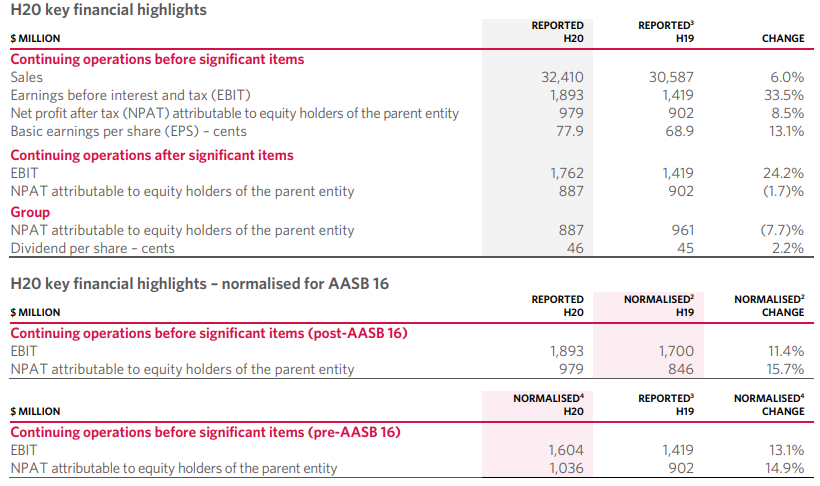

Decent Set of Financial Numbers in 1H FY20: Woolworths Group Limited (ASX: WOW) is involved in food, general merchandise and specialty retailing through chain store operations. The market capitalisation of the company stood at $45.81 Bn as on 17th March 2020. Woolworths managed to deliver growth in top-line and bottom-line during 1HFY20 despite a volatile trading environment. For the same period, sales from continuing operations stood at $32,410 million with a rise of 6.0%.

Due to strong sales growth and even with the increased costs, the Australian Food segment reported growth of 8.0% in EBIT.

Financial Summary (Source: Company Reports)

Expectation for Upcoming Half: For 2H FY20, the company is expecting higher food inflation to remain in Australian and New Zealand Food. WOW is optimistic about its plans for 2H FY20 despite a slower start to Q3.

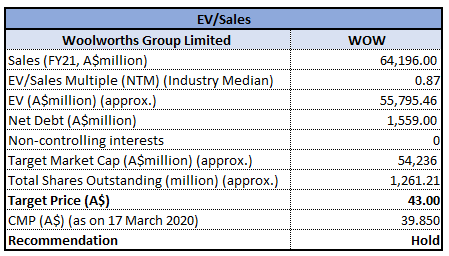

Valuation Methodology:EV/Sales Multiple Based Relative Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The Board of WOW declared a fully franked interim dividend of 46 cents per share, reflecting the growth of 2.2% on the back of decent financial position and confidence in the outlook.We have valued the stock using EV/Sales based relative valuation method and arrived at a target price, which is offering an upside of high single-digit (in percentage terms). Hence, in light of the outlook for 2H FY20, decent financial position and valuation, we maintain a “Hold” rating on the stock at the current market price of $39.850 per share, up by 9.719% on 17th March 2020.

Bubs Australia Limited

New Supply Agreement: Bubs Australia Limited (ASX: BUB) is a manufacturer of infant milk formula products and has a market capitalisation of $249.33 Mn as on 17th March 2020. BUB has recently inked a new supply agreement with Woolworths, wherein it would offer an entire range of eight infant formula products throughout a targeted selection of its 700 strong national store networks.

1HFY20 has proved as a period of solid growth trajectory for the company with gross revenue amounting to $28.75 million with a rise of 37% pcp. Bubs® Infant Formula stood as a key catalyst of growth in gross revenue.

Revenue Growth (Source: Company Reports)

Future Aspects: Bubs would continue its focus on operational and capital management. It would also focus on improving profit margins. The company is expecting product innovation extensions in goat dairy to generate future sales growth.

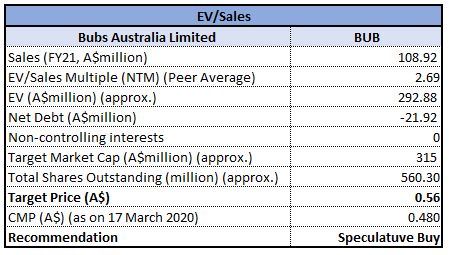

Valuation Methodology:EV/Sales Multiple Based Relative Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 3.03x in 1H FY20 against the industry median of 1.49x. This reflects that BUB is in a decent position to address its short-term obligations as compared to the broader industry. Debt to equity for 1H FY20 stood at 0.04x versus 0.19x of the industry median. We have valued the stock using EV/Sales based relative valuation method, and for the purpose, we have taken peers such as A2 Milk Company Ltd (ASX: A2M), Blackmores Ltd (ASX: BKL) and Woolworths Group Ltd (ASX: WOW) and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Therefore, considering the decent liquidity position, deleveraged balance sheet and signing of the new supply agreement, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.480 per share, up by 7.865% on 17th March 2020.

Propel Funeral Partners Limited

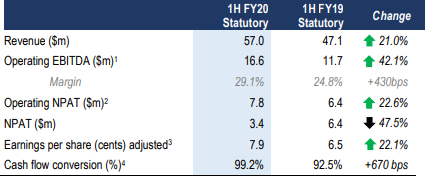

Material Growth in Revenue:Propel Funeral Partners Limited (ASX: PFP) provides death care services in Australia and New Zealand. The market capitalisation of the company stood at $281.4 Mn as on 17th March 2020. Viburnum Funds Pty Ltd and each of the parties has made a change to their substantial holdings in the company on 25th February 2020. The current voting power remains at 6.29% as compared to the previous voting power of 5.25%.

During 1HFY20, the company reported revenue amounting to $57.0 million, up 21% on pcp. Due to higher funeral volumes, average revenue per funeral growth as well as the adoption of AASB 16, the company experienced a growth in Operating EBITDA and margin. It also made an acquisition of the entire issued share capital of Gregson & Weight Pty Ltd, three substantial freehold properties as well as a parcel of vacant land on the Sunshine Coast in Queensland (QLD).

Material Growth in Revenue (Source: Company Reports)

What to Expect:For 2HFY20 and beyond, the company anticipates getting benefit from (1) the increasing and ageing population, (2) the recently expanded funding facilities and (3) acquisitions wrapped up in 1H FY20.

Stock Recommendation: The company announced a 100% franked interim dividend of 4.0 cps. It will pay the said dividend on 6th April 2020. The debt balance of PFP stood at around $67 million as at 31st December 2019. Moreover, it has a binding cash commitment to acquire the Dils Group, which would require a cash amount of around $20 million. As per ASX, the stock of PFP is trading closer towards its 52-week lower levels of $2.700, which could be understood as a decent level for entry. Thus, considering the material growth in 1H FY20, focus for FY20 and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $2.850 per share on 17th March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...