Stocks’ Details

InvoCare Limited

Successful Completion of Institutional Placement: InvoCare Limited (ASX: IVC) is a leading international provider of the funeral, cemetery, crematoria and related services. As on 15 April 2020, the market capitalization of the company stood at $1.32 billion. The company has recently completed a $200 million underwritten institutional placement by issuing 19.2 million new fully paid ordinary shares. The company intends to use the proceeds to reduce net debt and increase liquidity and balance sheet flexibility.

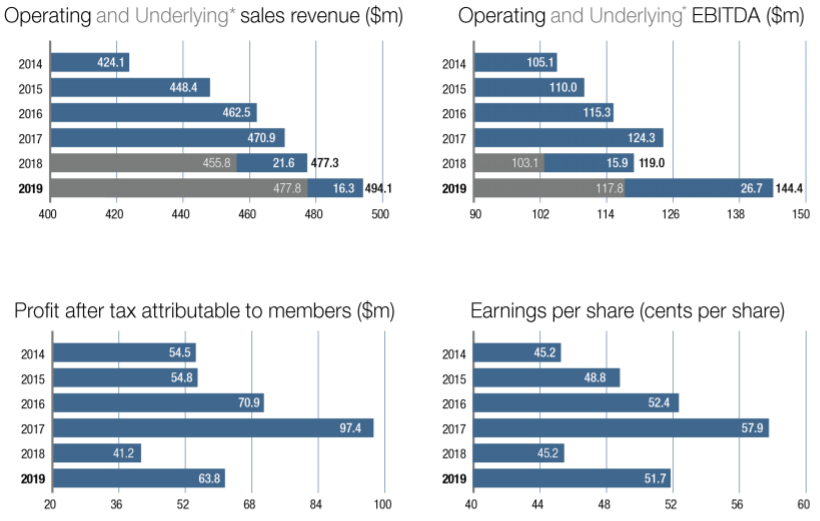

Decent Growth in EBITDA: During FY19, the company witnessed a slight increase of 3.5% in sales revenue to $494.1 million and a decent growth of 21.4% in operating EBITDA to $144.4 million. The growth was mainly due to contributions from funerals and memorial parks. This resulted in an increase of 54.6% in reported profit to $63.8 million.

FY19 Financial Highlights (Source: Company Reports)

What to Expect: The additional capital from institutional placements is expected to accelerate the roll out of the Enhance projects of Protect & Grow and to take advantage of new growth opportunities that may arise. The company will continue to focus on acquisitions and will ramp-up the pet cremation business. However, the economic and trading environment will continue to be considerably disrupted by COVID-19, and the company is witnessing the impact on its core business performance.

Stock Recommendation: As per ASX, the stock of IVC gave a negative return of 16.94% in the past six months and a negative return of 16.32% in the past one month. The stock is also trading inclined towards its 52-weeks’ low level of $9.070. During FY19, net margin of the company was 12.8%, lower than the industry median of 16.3%. On the TTM basis, the stock is trading at an EV/Sales multiple of 3.6x, higher than the industry median (Consumer Non-Cyclicals) of 1.7x. Considering the negative returns, trading levels and uncertainty in the business performance due to COVID-19, we have a watch stance on the stock at the current market price of $11.51, up by 2.039% on 15 April 2020.

United Malt Group Limited

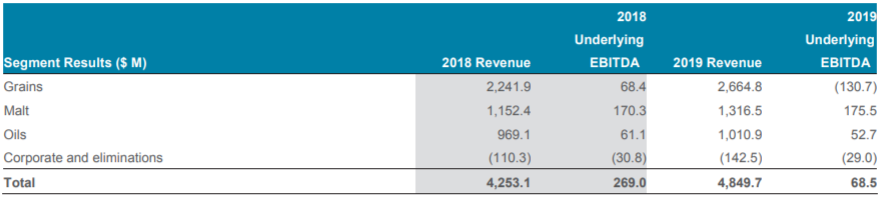

Decent Increase in EBITDA: United Malt Group Limited (ASX: UMG) is a newly established demerger of GrainCorp’s global malting business and is engaged in production, sale and distribution of bagged malt, hops, yeast, adjuncts and related products to major brewers, craft brewers, distillers and food companies. As on 15 April 2020, the market capitalization of the company stood at $1.23 billion. During FY19, Malt reported EBITDA of $176 million, up from $170 million last year. This was driven by solid customer demand, high capacity utilization and continued operational efficiency.

FY19 Financial Highlights (Source: Company Reports)

Future Expectations: The company has a strong market position and is expected to have a prudent balance sheet to support its strategic growth objectives. UMG is likely to be affected by COVID-19 and is not immune to uncertain circumstances.

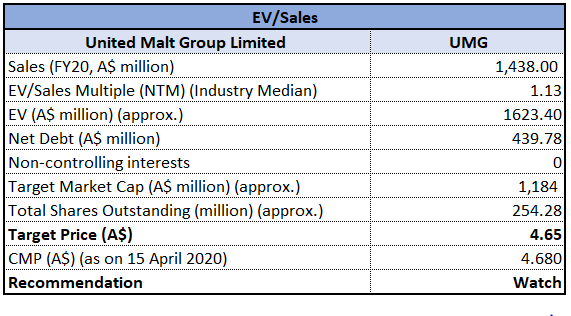

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

EV/Sales Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendations: As per ASX, the stock of UMG is inclined towards its 52-week high level of $5.240. During FY19, EBITDA margin of the company stood at 12.2%, lower than the industry median of 16.3%. Considering the trading levels and uncertainty about the business performance due to COVID-19, we have valued the stock using EV/Sales based illustrative relative valuation approach and have arrived at an indicative target price with a downside of low single digit (in percentage terms). Hence, we have a watch stance on the stock at the current market price of $4.68, down by 2.905% on 15 April 2020.

Bega Cheese Limited

Kraft Heinz Legal Proceedings: Bega Cheese Limited (ASX: BGA) is engaged in processing, manufacturing, cutting and packaging traditional cheese products, as well as the manufacture of other high value dairy products. As on 15 April 2020, the market capitalization of the company stood at $1.01 billion. The company has recently announced that the Federal Court of Australia has upheld the trial judgment and hence the company has the right to continue to use the current packaging of its Smooth and Crunchy Peanut Butter products.

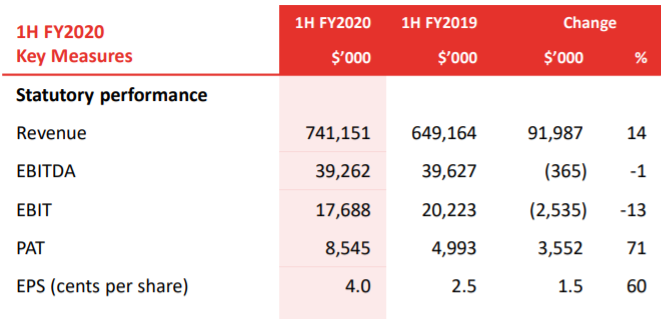

Significant Increase in PAT: During 1H20, the company reported an increase of 14% in revenue to $741.2 million and a significant growth of 71% in profit after tax to $8.5 million. This resulted in an increase of 60% in EPS to 4 cents per share. The decent financial and operational performance of the company enabled the Board to declare an interim dividend of 5.0 cents per share.

1H20 Financial Highlights (Source: Company Reports)

What to Expect: The company has continued the transition towards The Great Australian Food Company while responding to the ongoing competitive and supply challenges facing the dairy industry. The diversification strategy has positioned the company with improved capacity, capability and flexibility and is continuing to accelerate the development of new product ranges. It has provided guidance for FY20 and expects normalized EBITDA in the range $95 million to $105 million.

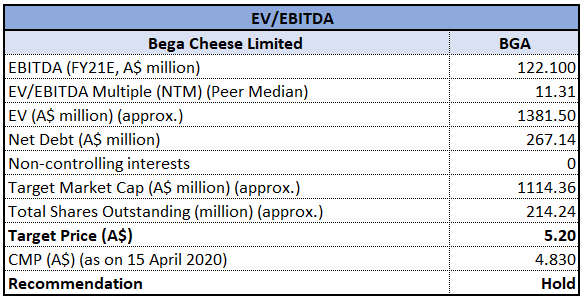

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation

EV/EBITDA Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of BGA gave a return of 9.26% on YTD basis and a return of 18.59% in the past one month. The stock is inclined towards 52-week high level of $5.530. The supply chain and customer shipments have not been materially impacted by the coronavirus.During 1H20, ROE witnessed a slight improvement over the previous half and stood at 1%, up from 0.8%. Considering the decent returns, improvement in ROE and decent outlook, we have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and have arrived at a target price of high single-digit upside (in percentage terms). For the said purpose, we have taken Tassal Group Ltd (ASX: TGR), Freedom Foods Group Ltd (ASX: FNP) etc. as peers. Hence, we recommend a ‘Hold’ rating on the stock at the current market price of $4.830, up by 2.331% on 15 April 2020.

Coca-Cola Amatil Limited

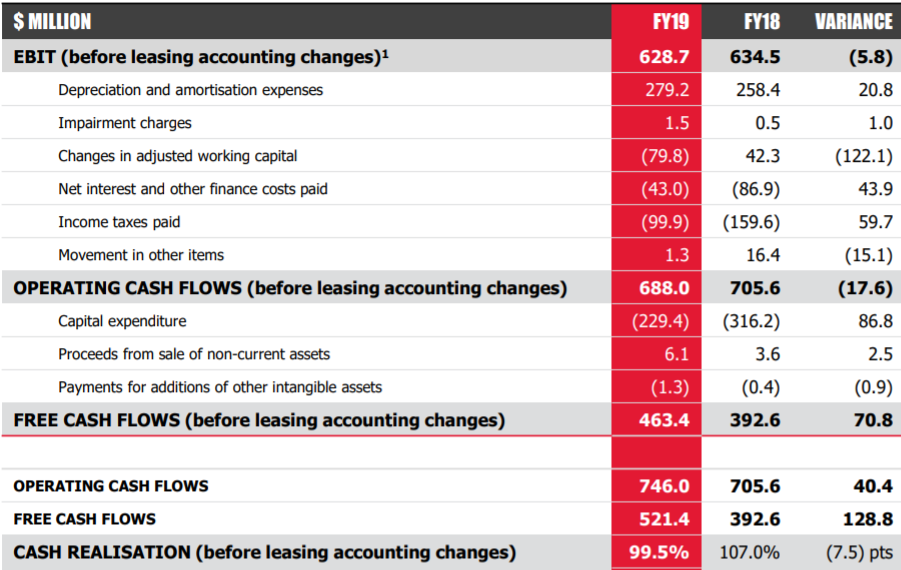

Strong Ongoing Free Cash Flow: Coca-Cola Amatil Limited (ASX: CCL) is engaged in the manufacturing, distribution and marketing of beverages. As on 15 April 2020, the market capitalization of the company stood at $6.91 billion. During FY19, the company witnessed a strong trading revenue growth for continuing operations of 6.7% and a growth of 31.9% in EBIT to $603.4 million. The company also reported strong cash flow result with ongoing free cash flow before lease accounting changes improving by $70.8 million on the prior year.

FY19 Financial Highlights (Source: Company Reports)

Growth Opportunities: Given the significant uncertainty with respect to COVID-19 pandemic, there might be short term volatility. However, the company has seen strong growth in the grocery channel as consumers stock up. CCL is maintaining a conservative balance sheet with the flexibility to fund future growth opportunities.

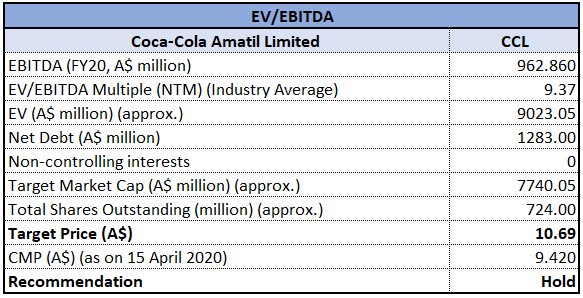

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation

EV/EBITDA Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of CCL is inclined towards its 52-weeks’ low level of $7.770. During FY19, ROE of the company stood at 23.7%, higher than the industry median of 11.8%. Considering the trading levels, decent financial performance and modest outlook, we have valued the stock using EV/EBITDA multiple based illustrative relative valuation approach and have arrived a target price with an upside of lower double-digit upside (in percentage terms). Hence, we see potential in the stock and recommend a ‘Hold’ rating at the current market price of $9.420, down by 1.361% on 15 April 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...