.png)

Stocks’ Details

Lovisa Holdings Limited

Comparable Store Sales Aided Revenue Growth: Lovisa Holdings Limited (ASX: LOV) is aninternational specialist and fast fashion jewelry retailer.

H1FY20 Financial Highlights for the Period ended 29th December 2019: LOV declared its six months results, wherein the company reported revenue of $162.8 million, up 22.2% driven by solid performance across most of the markets and growth from comparable store sales. The Australian region delivered strong growth benefiting from solid comparable store sales as well as growth in the online channel. Europe and USA sales posted new store growth and depicted an increase of 4 stores in the UK,10 stores in France and 21 in the USA. Asia sales were impacted by store closures in FY19 in Singapore and softer performance across markets. Gross margin decreased to 79% from 81.0% in H1FY19 due to decline in USD hedge rate as compared to the prior year. Profit after tax stood at $26.67, up 4.5% on y-o-y basis.

.png)

Gross margin trend (Source: Company Reports)

The Board of Directors declared a fully franked dividend of $0.15 per ordinary share with a payment date of 23rd April 2020 and ex-date of 10th March 2020.

Outlook: The business is focusing on expanding its store network and continues to expect the increase in number of stores for FY20 to be higher than FY19.

Stock Recommendation:The stock of LOV is trading at $8.90 with a market capitalization of ~$987.91 million. The stock made a 52-week low and high of $8.77 and $14.13 and is currently trading at the lower band of its 52-week trading range. The stock has delivered negative returns of 21.58% and 25.76% in the last three months and six-months, respectively. The company reported expansion in its international segment with an addition of 49 new stores during the half resulting in a total store network of 439. Considering the aforesaid facts, current trading levels and business prospects, we recommend a ‘Buy’ rating on the stock at the current price of $8.90, down 4.711% as on 4th March 2020.

Bapcor Limited

Heavy Commercial Trucks Segment to Drive Business Growth: Bapcor Limited (ASX: BAP) operates as a distributor of automotive components within the aftermarket segment. Recently, the company reported that one of its directors, named Andrew Charles Harrison, has acquired 10,000 shares at a consideration of $6.2917 per Share.

H1FY20 Operational Highlights for the Period ended 31st December 2019: BAP declared its half-yearly result, wherein the company reported revenue of $702.5 million, up 10.4% on pcp terms. The top-line growth was aided by addition of 35 stores to its network. Pro-forma EBITDA came in at $79.4 million, up 4.6% from H1FY19. Net profit after tax on pro-forma basis came in at $45.3 million, witnessing a growth of 5.1% on pcp terms. Burson reported same store sales growth of more than 5%, driven by successful promotion for six months. The company reported growth in revenue and EBITDA across every business segment. During December 2019, the company confirmed its acquisition of Truckline, which will add Heavy Commercial Vehicles in its product-line.

.png)

Key H1FY20 Business Highlights (Source: Company Reports)

The Board of Directors declared a fully franked dividend of $0.08 per ordinary share with a payment date of 13th March 2020.

Guidance: BAP expects its FY20 pro-forma NPAT to grow at middle single digit in percentage terms. The company is expecting return on investment at ~15% for FY21.

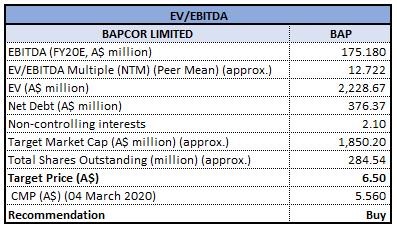

Valuation Methodology: EV/EBITDA Based Relative Valuation

EV/EBITDA based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:The stock of BAP is trading at $5.56 with a market capitalization of ~$1.67 billion. The stock made a 52-week low and high of $5.32 and $7.525 and is currently trading at the lower band of its 52-week trading range. The stock has delivered negative returns of 13.06% and 12.80% in the last three months and six-months, respectively. The addition of heavy commercial truck parts into the portfolio would provide another platform of growth for the company and place it as the only supplier of replacement parts and accessories for all segments of on road vehicles. Considering the aforesaid facts, current trading levels and business prospects, we have valued the stock using EV to EBITDA based relative valuation method. For this we have taken peers like Baby Bunting Group Ltd (ASX: BBL), Autosports Group Ltd (ASX: ASG) and Lovisa Holdings Ltd (ASX: LOV), and arrived at a target price of lower double-digit upside (in % terms). Hence, we give a ‘Buy’ on the stock at the current price of $5.56, down 5.119% as on 4th March 2020.

Myer Holdings Limited

Improved Digital to Drive Operating Performance: Myer Holdings Limited (ASX: MYR) operates in the departmental stores segment and has a portfolio of 66 stores across Australia. On 03rd February, the company informed the appointment of Paul Morris for the post of General Counsel and Company Secretary.

FY19 Business Highlights for the Period ended 27 July 2019: MYR came up with its full year results, wherein the company reported total sales of $2,991.8, down 3.5% on y-o-y basis due to 1.3% decline in the comparable store sales, excluding sales in Apple products. The company reported robust growth in the online sales of 25.6% to $262.3 million. Cost of Doing Business, during the period improved 3.1% to $1,002.4 million. The business reported a statutory NPAT of $24.5 million, as compared to a loss of $ 486 million. Operating cash flow increased by $8 million to $138 million while total net debt reduced by $69 million in FY19.

.png)

Key FY19 Income Statement Highlights (Source: Company Reports)

Stock Recommendation:The stock of MYR is trading at $0.345 with a market capitalization of ~$287.45 million. The stock made a 52-week low and high of $0.325 and $0.74 and is currently trading at the lower band of its 52-week trading range. The stock is available at EV/EBITDA multiple of 2.0x as compared to the industry (Diversified Retail) median of 7.1x. The stock has delivered negative returns of 31.37% and 35.19% in the last three months and six-months, respectively. During FY19, the company reduced costs by $32.6 million, as a result of an enhanced new staffing model in-store, improved marketing spends, lower store occupancy, as well as efficiencies and reduced waste across all areas of business. Considering the aforesaid facts, valuation, current trading levels and business prospects we recommend a ‘Speculative Buy’ rating on the stock at the current price of $0.345, down 1.429% as on 04th March 2020.

Mosaic Brands Limited

Strategic Initiatives Resulted in Improved Gross Margin: Mosaic Brands Limited (ASX: MOZ) is a retail-based company, which is focused on women’s specialty fashion retail and has brands like Millers, W.Lane, Noni B, Rivers, Katies etc., in its portfolio.

H1FY20 Operational Highlights for the Period ended 29 December 2019: MOZ declared its half yearly results, wherein the company reported revenue $413.8 million, down 10.9% on pcp. The performance was affected due to Bushfires in the months of November and December 2019. The business reported growth in the Online Sessions by 8% on y-o-y basis and delivered 678K orders in H1FY20. The company reported 33% y-o-y growth in the Mobile Sales Traffic. Online sales represented 10.1% of total sales. Net profit after tax grew by 47.5% on pcp terms to $14.1 million. The group’s gross margin grew to 60% from 57%, aided by the focus on prioritising gross margin over sales.

.png)

Key FY20 Income Statement Highlights (Source: Company Reports)

Outlook: The outbreak of COVID-19 is expected to cause manufacturing and shipping delays in the near future.

Stock Recommendation:The stock of MOZ is trading at $1.065 with a market capitalization of ~$112.3 million. The stock made a 52-week low and high of $1.020 and $3.4 and is currently trading at the lower band of its 52-week trading range. The stock is available at EV to sales multiple of 0.3x, as compared to the industry average (Specialty Retailers) of 1.2x. The stock has delivered negative returns of 54.69% and 60.41% in the last three months and six-months, respectively. Despite the challenging business environment, the business delivered decent operating performance during the first half of FY20. Acquisition of five brands from Specialty Fashion Group has reported comparable store growth in H1F20. Considering the aforesaid facts, current trading levels, valuation and business prospects, we give a ‘Speculative Buy’ rating on the stock at the current price of $1.065, down 8.19% as on 04th March 2020.

Comparative Price Chart (Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...