.png)

Stocks’ Details

REA Group Ltd

Recovery in Real Estate Market: REA Group Ltd (ASX: REA) provides property and property-related services on websites and mobile apps throughout Australia and Asia. The market capitalisation of the company stood at $13.69 billion as on 26th June 2020. For the nine months ended 31st March 2020, the company reported revenue and EBITDA of $640.2 million and $390.8 million, respectively. Moreover, the group delivered an improved performance during the quarter ended 31st March 2020, reflecting the continued recovery of the real estate market prior to the effects of COVID-19 emerging in mid-March. During the quarter, overall national residential listings experienced a decline of 7%, while Melbourne and Sydney’s listings went up by 6% and 5%, respectively.

.png)

Key Financial (Source: Company Reports)

Impact on Revenue: REA expects the adverse impact on revenues due to softness in new listing volumes and measures undertaken by the group to support its customers in these challenging times.

Key Risks: As of now, the biggest challenge for business is to deal with the uncertainty in the market, which caused weakness in listing volumes. Moreover, the company is exposed to five material risk, which includes strategic risk, operational risk, compliance risk, regulatory risk, and credit risk. The company also deals with the development of new technologies and increased competition from existing or new sites and apps, which could affect the existing business model.

Stock Recommendation: The group possesses a strong balance sheet with low debt level and a cash balance of $135 million as at 30 April 2020. REA also cemented its liquidity position by entering into an additional $149 million loan facility with the existing banking syndicate. Net margin of the company stood at 31.4% in 1H FY20, reflecting YoY growth of 30.9%. This indicates that the company has improved its capabilities to covert its top-line into the bottom-line. The stock of REA has provided decent returns of 4.02% and 50.65% during the span of one and three months, respectively. Hence, considering the decent balance sheet, strengthened liquidity position and recovery in the real estate market, we give a “Hold” recommendation on the stock at the current market price of $104.900 per share, up by 0.914% on 26th June 2020.

Fortescue Metals Group Ltd

Strong Demand for Products: Fortescue Metals Group Ltd (ASX: FMG) is engaged in the mining, processing, and transporting of iron ore. The market capitalisation of the company stood at $42.71 billion as on 26th June 2020. Recently, the company announced an emissions reduction goal to achieve net zero operational emissions by 2040. The company added that this goal is core to its climate change strategy and is supported by a pathway to decarbonisation, including the reduction of Scope 1 and 2 emissions from existing operations by 26% from 2020 levels, by 2030. During Q3 FY20, the company experienced a record iron ore shipment of 42.3 million tonnes, reflecting a rise of 10% over Q3FY19. This indicates strong operating performance and resilient demand. FMG also experienced robust demand for its products, which delivered an average revenue of US$73/dry metric tonne.

.png)

Production Summary (Source: Company Reports)

Guidance: For FY20, the company expects shipments in the range of 175 million tonnes - 177 million tonnes. FMG anticipates capital expenditure to be in the rage of US$2.0 billion - US$2.2 billion.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risks: Fortescue Metals Group Ltd is exposed to transitional risks and physical risks. Transitional risks arise mainly from policy and regulatory changes and reduced product demand. While physical risks are associated with the increased severity of extreme weather events.

Stock Recommendation: During Q3 FY20, the company experienced a healthy cashflow from its business, which resulted in a cash balance of US$4.2 billion at 31st March 2020. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with the upside of high single-digit (in percentage terms). For the purpose, we have taken peers like South32 Ltd (ASX: S32), Champion Iron Ltd (ASX: CIA), Rio Tinto Ltd (ASX: RIO). Thus, in light of strong operating performance and resilient demand, strong cash flow and guidance, we maintain a “Hold” recommendation on the stock at the current market price of $14.180 per share, up by 2.235% on 26th June 2020.

Northern Star Resources Ltd

Sale of Gold Project: Northern Star Resources Ltd (ASX: NST) is engaged in the production and exploration of gold and other minerals. The market capitalisation of the company stood at $10 billion as on 26th June 2020. Recently, the company announced that it has agreed to sell the Mt Olympus Project comprising most of the Ashburton Project in Western Australia to Kalamazoo Resources Limited (ASX: KZR) for a deferred contingent cash consideration amounting to A$17.5 million. As per the terms of the agreement, NST will receive - (a) $5.0 million on mining of the first 250,000 tonnes of ore, (b) a 2% Net Smelter Royalty on the first 250,000 ounces of gold produced, with a 0.75% Net Smelter Royalty on any subsequent gold produced from the tenements. NST would also receive the same on any other metals produced from the tenements.

During the quarter ended 31st March 2020, the company reported the gold sale of 239,031 ounces at an AISC of A$1,590/oz. The company added that the Australian operations have sold 190,258oz at an AISC of A$1,505/oz and the Pogo operations sold 48,773oz at an AISC of US$1,254/oz. This helped the company to generate an underlying free cash flow of A$89 million after investing ~A$66 million in growth capital and exploration. Previously, the company has also acquired a 50% interest in KCGM.

.png)

Gold Inventories (Source: Company Reports)

Aspects: Looking forward, the company is likely to reap the benefits of the KCGM acquisition (50% Interest). The company is optimistic that the acquisition would drive more substantial growth in its net cashflow while maintaining strong overall financial returns.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risks:The company is exposed to climate change risk, which can affect its production. To mitigate this risk, the company exercises continuous quarterly ground water reviews and modeling interpretations. FMG’s business is also sensitive to several social risks.

Stock Recommendation: Current ratio of the company stood at 5.20x in 1H FY20 as compared to the industry median of 1.81x. This reflects that NST is in a decent position to address its short-term obligations as compared to the peer group. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with the upside of high single-digit (in percentage terms).For the purpose, we have taken peers such as Saracen Mineral Holdings Ltd (ASX: SAR), St Barbara Ltd (ASX: SBM), OceanaGold Corp (ASX: OGC), etc. Therefore, considering the decent liquidity position, decent gold sale in Q3 FY20 and outlook, we give a “Hold” recommendation on the stock at the current market price of $13.130 per share, down by 2.813% on 26th June 2020.

Wesfarmers Limited

A Look at Retail Performance: WesfarmersLimited (ASX: WES) is engaged in the retail operations covering home improvement and office supplies. The market capitalisation of the company stood at $49.55 billion as on 26th June 2020. Recently, the company provided a retail trading update, wherein it stated that each of its businesses remains vigilant in prioritising the safety of team members and customers. The company experienced significant demand growth in Bunnings and Officeworks as customers continue to spend more time working, learning, and relaxing at home. In Bunnings, the strong sales performance was supported by continued growth in consumer and commercial markets in all major Australian trading regions and in all product categories.

The Group’s retail businesses have delivered total online sales growth of 89% in the calendar year to date (9th June 2020). This indicates the significant investment across the Group in respective e-commerce capabilities in recent years as well as greater customer preference for shopping online during COVID-19.

.png)

Sales Performance (Source: Company Reports)

Focus for Growth: WES would continue to develop and improve its portfolio of businesses, building on its unique capabilities and platforms in order to take benefits of growth opportunities within existing businesses, recently acquired investments as well as to pursue transactions which create value for shareholders over the long term.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risks: The company is exposed to numerous risks such as strategic risk and operational risk; wherein strategic risk comes due to increased competition and ineffective execution of strategy. While operational risk mainly arises due to loss of critical supply inputs or infrastructure, including IT systems. WES’ business is also sensitive to the financial risk caused by currency volatility, adverse commodity price movements and reduced access to funding.

Stock Recommendation: EBITDA margin of the company stood at 15.2% in 1H FY20, reflecting YoY growth of 3.0%. Return on equity of the company stood at 11.4 in 1H FY20 with a growth of 5.1% on a YoY basis. Over the span of five-years (2015-2019), the company has maintained a positive free cash flow, which shows the prudent use of working capital. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with the upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Coles Group Ltd (ASX: COL), Woolworths Group Ltd (ASX: WOW), JB Hi-Fi Ltd (ASX: JBH). Thus, considering the decent performance in the retail operation, returns paid to shareholders, prudent use of working capital, we give a “Hold” recommendation on the stock at the current market price of $43.910 per share, up by 0.481% on 26th June 2020.

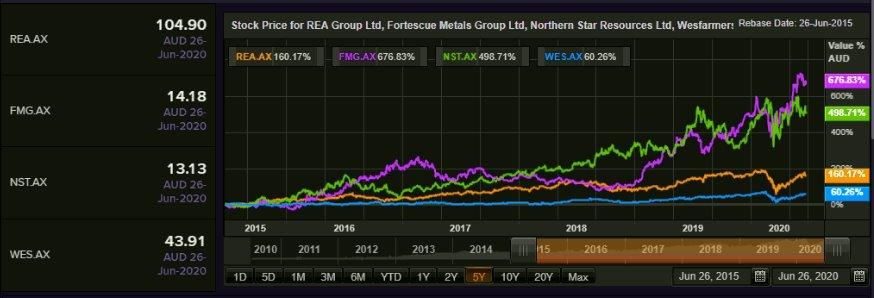

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...