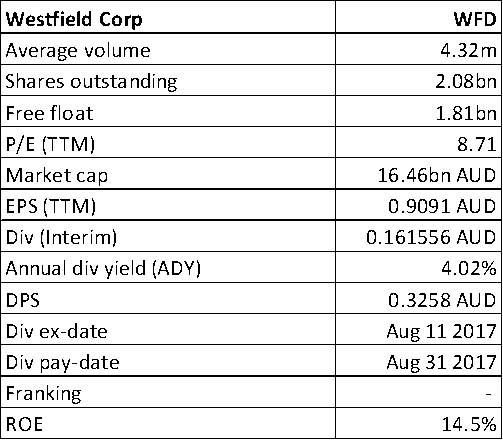

Westfield Corporation

WFD Details

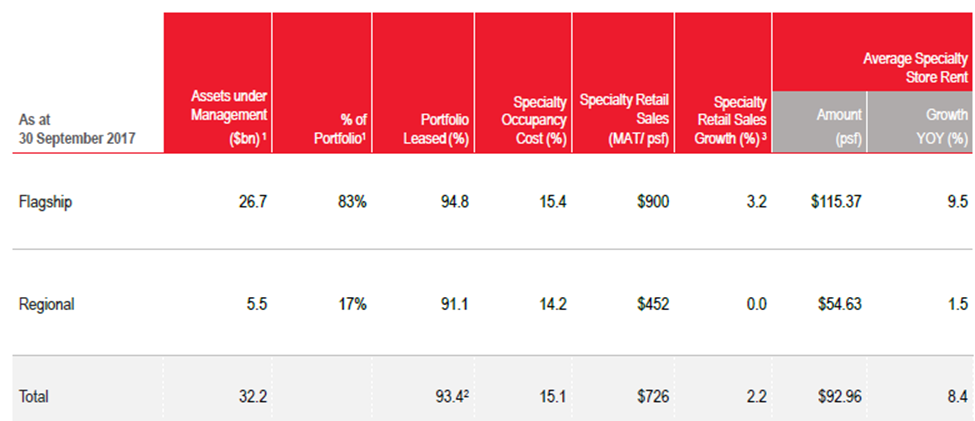

Better operating metrics:Westfield Corporation (ASX: WFD) in the third quarter ending September 2017, has increased the average store rents by 9.5% year-on-year, with retail sales growth of 3.2% across its flagship malls located primarily in London, Los Angeles, and New York. For Regional segment, the average specialty store rent grew 1.5%. WFD’s regional malls tend to have an impact from the shift to online shopping, with 83% of its assets under management now under flagship malls.

Portfolio Operating Statistics for September Quarter (Source: Company Reports)

Moreover, WFD has US$3.8 billion of current residential or commercial property development projects and another US$6 billion of pre-development projects in the pipeline. Meanwhile, WFD stock has risen 4.5% in three months as on November 09, 2017, and has been up 3% on November 10, 2017 with a broad rally for US mall owners. Given the mixed view on group outlook and tough retail environment while operating metrics are staying at a decent level, we put a “Hold” recommendation on the stock at the current price of $8.34 and will review at a later stage.

WFD Daily Chart (Source: Thomson Reuters)

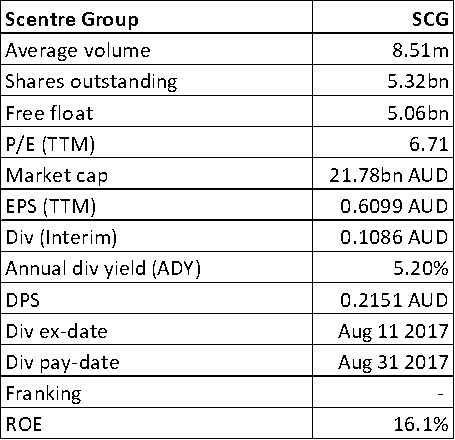

Scentre Group

SCG Details

Total sales grew 1.7% in the third quarter:Scentre Group (ASX: SCG) has reported mixed sales for its third-quarter trading update due to the general weaker state of consumer sentiment while there has been a positive sentiment on mall owners at a broader level. In the third quarter, the total sales grew 1.7% to $23 billion. The department store tenants saw sales decline of 6.7% for the nine months ending September 30, while the more popular, specialty store sales witnessed a rise of 0.9%. Overall, SCG expects full-year funds from operations growth to be in line with guidance of 4.25%, and has maintained the distribution per security of 21.73¢, which is a growth of 2%.

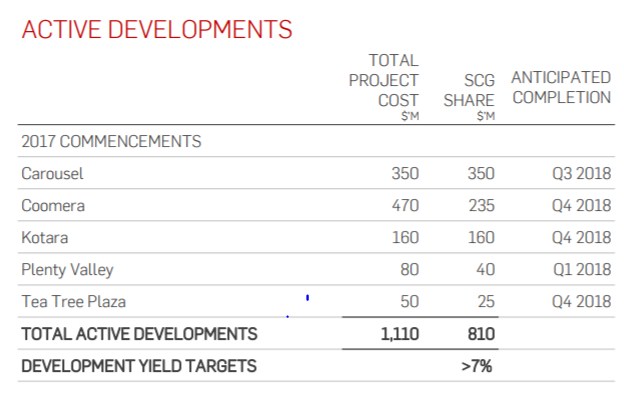

Active Developments (Source: Company Reports)

Meanwhile, SCG stock has risen 6% in last three months as on November 09, 2017 and is trading at a reasonable P/E. We give a “Buy” recommendation on the stock at the current price of $4.19

.png)

SCG Daily Chart (Source: Thomson Reuters)

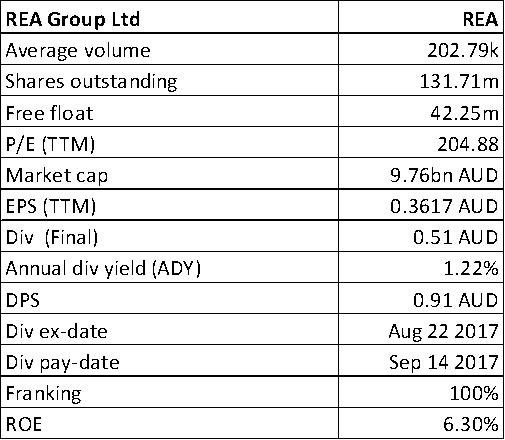

REA Group Ltd

REA Details

Financial Service revenue included in the first quarter of FY18: REA Group Ltd (ASX: REA) in the first quarter of FY18 has reported for 21% growth in the revenue to $190 million, while operating expenses grew 17% to $81 million, and earnings before interest, tax, depreciation, and amortisation (EBITDA) grew 24% to $107 million. Moreover, REA indicated that its revenue growth is faster than expenses for the whole year, although this may not be the case in every quarter. The company has reported $34 million in free cash flow in Q1 FY18. Additionally, the revenue grew due to the Australian residential business, and the inclusion of financial services revenue from August, which was not included in the prior comparative period. The strong residential growth included price changes, the continued success of the Premiere All offering and favorable listings mix. In addition, the financial services segment is on track to deliver the previously stated FY18 guidance of revenue of between $26m - $30m and EBITDA of between $7m - $11m. Meanwhile, REA stock has risen 19.64% in last six months as on November 09, 2017 and rose 1.7% on November 10, 2017. With continued favorable market conditions, we give a “Hold” recommendation on the stock at the current price of $76.17

.png)

REA Daily Chart (Source: Thomson Reuters)

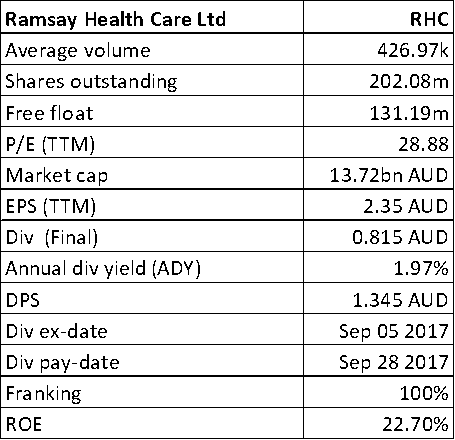

Ramsay Health Care Ltd

RHC Details

Targeting Core EPS growth of 8% to 10% for FY18:Ramsay Health Care Ltd (ASX: RHC) is expanding and developing the hospital business across the world to meet the demand from the ageing and growing population. The company expects strong growth in the Australian hospital business to continue in FY18 due to the ongoing growth in hospital utilisation rates as well as uplift from the brownfield development program. In international markets, RHC is expecting the increase in tariff in the UK scheduled for April 2018; and in France, the election of the new government has seen an uplift in business and consumer sentiment. RHC is targeting Core EPS growth of 8% to 10% for FY18. Moreover, RHC in FY 17 had reported a 12.7% growth in the Core Net Profit After Tax to $542.7 million tracking well with growth. Given the potential, we give a “Buy” recommendation on the stock at the current price of $67.33

.png)

RHC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...