Stocks’ Details

Origin Energy Limited

Integrated Gas Business Reports Strong Earnings:Origin Energy Limited (ASX: ORG) is engaged in the operation of energy businesses, including exploration and production of natural gas, electricity generation & sale of electricity and liquefied natural gas.

Agreement with BidEnergy: The company has recently signed an agreement with BidEnergy Limited (ASX: BID) for the deployment of its Robotic Process Automation platform to the Commercial and Industrial customers of Origin Energy.

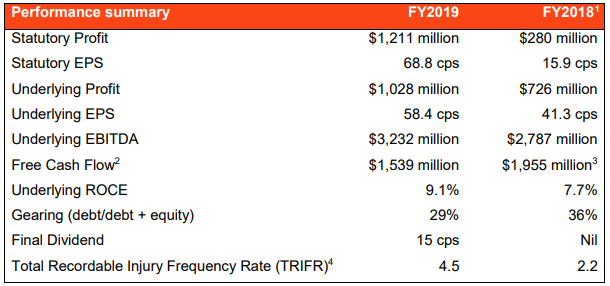

FY19 Performance Highlights: During the year ended 3 0 June 2019, statutory profit amounted to $1,211 million, representing a substantial increase on prior corresponding year profit of $280 million. Underlying EBITDA for the period amounted to $3,232 million, up 16% on pcp EBITDA of $2,787 million. Underlying profit for the year stood at $1,028 million as compared to $726 million in FY18. During the year, a fully franked final dividend of 15 cents per share was declared with a revision in dividend policy, targeting an ordinary dividend payout ratio of 30-50% of free cash flow per year.

FY19 Financial Performance (Source: Company Reports)

FY20 Guidance: In FY20, the company expects underlying EBITDA to be in the range of $1,350 million - $1,450 million. Corporate costs for the year are anticipated to be in the range of $70 million - $80 million. Australia Pacific LNG is expected to report production in the range of 680 – 700 petajoules.During the year, the company plans to incur capex in the range of $530 million and $580 million. Guidance for capital expenditure was issued after excluding Australia Pacific LNG.

Stock Recommendation: The stock of the company generated returns of 0.26% and 4.43% over a period of 1 month and 3 months, respectively. FY19 was a period of strong earnings by Integrated Gas on the back of cost efficiencies, stable production at Australia Pacific LNG, and higher effective oil price. Financial performance further improved on the back of a reduction in financing costs due to debt reduction and a lower average interest rate. Going forward, the debt balance is expected to reduce further upon the sale of Ironbark asset to Australia Pacific LNG for $231 million. Considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $7.870, up 1.157% on 11 October 2019.

Nine Entertainment Co. Holdings Limited

Significant Earnings Growth in Digital & Publishing Division: Nine Entertainment Co. Holdings Limited (ASX: NEC) is involved in broadcasting, program production and publishing activities.

Acquisition of Macquarie Media Limited: As per the recent announcement, the company updated that Fairfax Media Limited will be acquiring all remaining shares of Macquarie Media Limited. Currently, Nine Bidder has a voting power of 92.80% in Macquarie Media Limited.

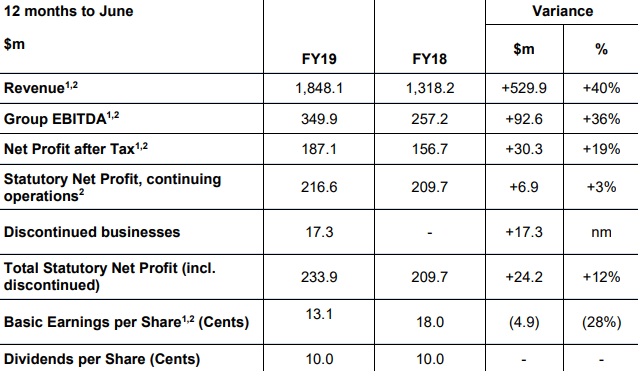

FY19 Financial Results: During the 12 months ended to 30 June 2019, the company reported a net profit after tax amounting to $233.9 million, up 12% on prior corresponding period.Revenue for the year amounted to $1,848.1 million, up 40% on pcp revenue of $1,318.2 million. Group EBITDA increased by 36% to $349.9 million.

FY19 Reported Results (Source: Company Reports)

Revenue for the digital & publishing division increased at a rate of 3%. EBITDA for the segment reported a rise of 56% on the back of more than 60% growth in both Metro Media and 9Now. Revenue for the Broadcasting division went down by 5%, which was mostly confined to the first half of the year. During the year, the company completed the acquisition of Fairfax, realising synergies worth $22 million in FY19.

Outlook & Guidance: In FY20, costs pertaining to Free to Air (FTA) television are expected to increase by approximately 4%. Market conditions in the FTA market are expected to improve, which, in turn, are likely to support revenue in Q2FY20. Digital and publishing division is expected to grow further in FY20. Stan division is expected to move into profitability on the back of increased subscribers. Group EBITDA in FY20 is expected to grow at a rate of 10%.

Stock Recommendation: The stock generated negative returns of 7.54% and 8.46% over a period of 1 month and 3 months, respectively. In FY19, the company saw a remarkable earnings growth in the digital and publishing division, with further growth expected on the back of growth at 9Now and top-line growth and cost efficiency gains coming in from Metro Media. Stan will also be seen generating profits with the increasing subscriber numbers on the platform. Overall, the company is expecting to deliver decent performance growth on the back of improvement in market conditions and merger synergies. Considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $1.860, up 1.087% on 11 October 2019.

Treasury Wine Estates Limited

Full-Year Cash Conversion Ahead of Guidance:Treasury Wine Estates Limited (ASX: TWE) is engaged in production, marketing and sale of wine. The company recently notified about the issue of 200,844 fully paid ordinary shares at an issue price of $18.5632 per share under its Dividend Reinvestment Plan.

Dividend: On 04 October 2019, the company paid a dividend amounting to AUD 0.2000 per ordinary share. Full year dividend amounted to 38 cents per share, representing an increase of 19% on pcp.

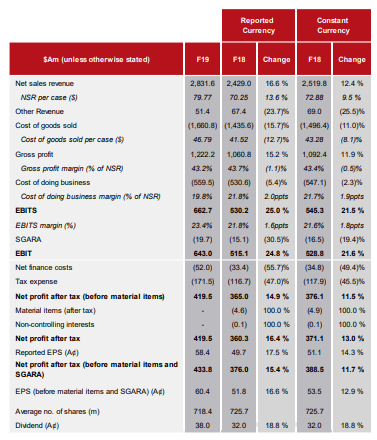

FY19 Performance Highlights: During the year ended 30 June 2019, the company reported net sales revenue amounting to $2,831.6 million, up 17% on prior corresponding period. NPAT for the period amounted to $419.5 million, up 16% on previous year. Earnings before interest, tax, SGARA, and material items (EBITS) amounted to $662.7 million, up 25% on pcp.

FY19 Financial Performance (Source: Company Reports)

FY20 Guidance: In FY20, the company expects EBITS to grow in the range of 15% - 20%. Underlying cash conversion for the year is expected to be broadly in-line with FY19.

Stock Recommendation: Over a period of 6 months, the stock of the company generated returns of 18.96%. In FY19, the company reported full-year cash conversion of 75.8% against the guidance range of 60% - 70%. The period saw the strongest organic growth rate in the company’s lifetime, with net sales revenue going up by 12% on a constant currency basis. In FY19, the company had an EBITDA margin of 26.1%, higher than the industry median of 18.9%. Net margin for the year stood at 14.6% as compared to the industry median of 8.3%. Currently, the stock is trading towards its 52-week high price of $19.47 with PE multiple of 30.51x and an annual dividend yield of 2.13%. Hence, in view of aforesaid factors and current trading levels, we give a "Hold" recommendation on the stock at the current market price of $17.930, up 0.617% on 11 October 2019.

Coles Group Limited

Strong Cash Realisation in FY19: Coles Group Limited (ASX: COL) is an Australian retailer of products like fresh food groceries, household goods, etc. On 11 October 2019, the market capitalisation of the company stood at A$20.28 Bn. Recently, the company notified that it will be conducting its AGM on 13th November 2019. As per the release dated 20th September 2019, COL announced that it would be implementing a Dividend Reinvestment Plan for its shareholders. It is expected that the DRP would operate for eligible shareholders for dividends paid subsequent to 26th September 2019.

FY19 Highlights: During the year ended 30 June 2019, the group reported sales revenue amounting to $35.0 billion, up 3.1% on previous year. Supermarkets comparable sales reported a rise for the 47th consecutive year along with EBIT growth of 2.2% yoy.

Financial Results (Source: Company Reports)

What to Expect: In FY20, the company expects Smarter Selling initiatives to deliver annualized benefits in excess of $150 million. Earnings growth under the new alliance agreement with Viva Energy are expected to remain subdued in FY20, considering the time required to build fuel volumes to target levels.

Stock Recommendation:Over a period of 6 months, the stock generated returns of 25.55%. In FY19, the company reported a strong cash realization of 110%, accompanied by an improvement in net debt position, providing significant flexibility for long term growth. The current ratio of the company stood at 0.79x in FY19, reflecting a YoY growth of 50.9%. This implies that the company is in a decent position to address its short-term obligations. Currently, the stock is trading close to its 52-week high level of $15.61 with PE multiple of 14.13x. Hence, in light of the above-stated facts and current trading levels, we reiterate our "Hold" recommendation on the stock at the current market price of A$15.370 per share, up 1.118% on 11 October 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...