Coca-Cola Amatil Limited (ASX: CCL)

.png)

CCL Details

Improved Financial Performance for 2017: CCL announced 2017 results and reported a net profit after tax of $416.2 million (down 0.4%) that is broadly in line with the previous year and in line with the guidance provided in April 2017, and beats consensus forecasts at the back of better performance for Australian beverages. Coca-Cola Amatil’s New Zealand and Fiji segment performed strongly again and delivered a 15 per cent of the Group’s underlying EBIT. Indonesia and Papua New Guinea delivered another very strong earning result with a growth of 30.6 per cent and Alcohol and Coffee delivered 11.2 per cent growth that is line with the shareholder value proposition. The Group completed a buy-back program and acquired 39.6 million shares at an average price of $8.84 per share. While net debt increased by $344.4 million and amounted to $1.3 billion. The Group also maintained a strong interest coverage.

.png)

Segment Results (Source: Company Reports)

Its Accelerated Australian Growth Plan will require an additional investment of approximately $40 million in 2018 across marketing, execution, cold drink equipment, technology and price and this investment will negatively impact Australian Beverages and consequently the Group’s near-term earnings. In the medium term, it continues to target mid-single digit EPS growth, that will be in line with its shareholders value proposition. The Group appointed Ms Julie as a Non-Executive Director and will be effectively taking responsibilities from March 2018. The stock prices rose by 4.20% in the past six months and by 5.33% in the past one week. Looking at the improved results and potential seeding in the future with CCL increasing its final dividend by 1 cent, we give a “Buy” recommendation on the stock (up 1.6% on February 21, 2018) at the current market price of $8.83

.png)

CCL Daily Chart (Source: Thomson Reuters)

Scentre Group (ASX: SCG)

.png)

SCG Details

Delivered strong operating metrics: Up 1.8% in terms of stock price, SCG announced its results for 12 months that is till December 2017 and represented $1.290 billion of Funds from Operations and represented 24.29 cents per security, up by 4.25%. The Group delivered profit of about $4.2 billion for the year (up 41%) which included property revaluations of $3.2 billion and these revaluations reflect a strong net operating income growth across the portfolio. Its strong NOI growth was underpinned by growth in customer visitation and the retailer demand was maintained that is occupancy was greater than 99.5%. The Group completed lease deals across all categories including 31 major stores with average tenure of 15 years and 2,466 of speciality lease deals and covered an aggregate of more than 345,000 square metres of space.

.png)

Leasehold Expiry Profile (Source: Company Reports)

Comparable net operating income increased by 2.75% for the 12 months as it was majorly due to an escalation in annual rent. In 2017, the Group announced that it will continue to grow distributions at approximately 2% until it reaches a pay-out ratio of 85% of FFO. The Group forecasts FFO growth of approximately 4.0% for 12 months that is ending on 31 December 2018 and the distribution for 2018 is forecasted to be 22.16 cents per security that is an increase of 2% on prior year. We maintain a “Buy” recommendation by seeing the potential for future growth, at the current price of $3.89

.png)

SCG Daily Chart (Source: Thomson Reuters)

Seven Group Holdings Limited (ASX: SVW)

.png)

SVW Details

Growth in earning base in WesTrac and Coates Hire: SVW declared strong FY18 interim results and reported a 42 per cent of an increase in underlying EBIT from its continuing operations that amounted to $223.5 million and was driven by a strong performance from its industrial service businesses, WesTrac and Coates Hire. Seven West Media share of NPAT grew by 7 per cent in the period which was due to its cost initiatives and reduction in license fee despite of a decline in advertising revenue share. The Net Debt increased by $711.9 million and climbed to $2,020.0 million at the end of the period and that was driven by acquisition of Coates Hire debt of $1,034 million and due to an increase in investment in Beach Energy that reached to $117 million. It was offset by the net proceeds from capital raising of about $385 million and from the net proceeds of $535 million from the sale of WesTrac China.

.png)

Revenue Split for 2017 (Source: Company Reports)

An interim ordinary dividend of 21 cents per share fully-franked was declared that is up by 5 per cent on the prior comparative period. The stock price climbed by 11.6% as on February 21, 2018 after the Group announced its interim results and upgraded its full year guidance. However, the stock trades at a high price to earnings level and looks “Expensive” at the current market price of $18.40

.png)

SVW Daily Chart (Source: Thomson Reuters)

Wesfarmers Limited (ASX: WES)

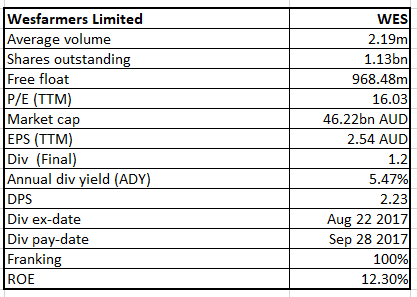

WES Details

Impacted by write-downs:Though Wesfarmers’ stock rose 3%, the group reported a net profit after tax (NPAT) of $212 million for the half-year ending on 31 December 17 indicating an 86.6% drop at the back of $1.3 billion in write-downs on Bunnings UK and Ireland and Target. On the other hand, strong production volumes and high coal prices in Resources businesses contributed to a significant increase in the Industrials division’s earnings. The Group generated operating cash flows of $2,897 million for the half and was supported by proactive working capital management.

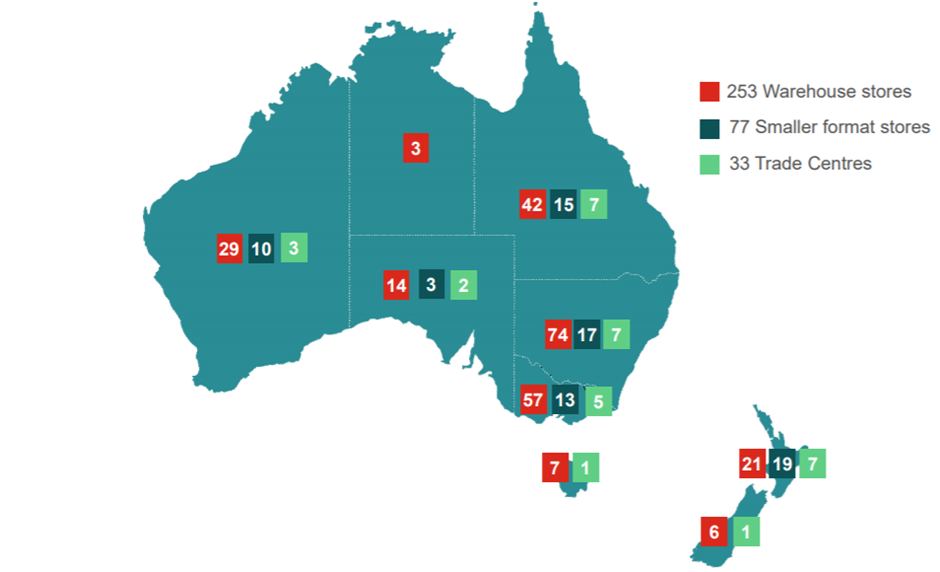

Allocation of the stores (Source: Company Reports)

In December 17, the Group announced an agreement to sell the Curragh coal mine for $700 million which also included a value share mechanism that allowed Wesfarmers to participate in possible future coal price increase and on a successful completion of this transaction, the Group expects to record a post-tax profit of $100 million approximately. The directors declared an interim dividend of $1.03 per share and this is in line with the previous corresponding period. Given the shortcomings of the group’s overall performance, the stock looks “Expensive” at the current market price of $41.99

.png)

WES Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...