Stocks’ Details

CSL Limited (ASX:CSL)

Positive Outlook uplifted the Profit Guidance- For the past one year, the stock was rising by 38.72 per cent among the big names but saw a dip of 1.139 per cent as on 29 June 2018. The Company recently announced a revised profit outlook for fiscal 2018 and anticipates that it will be able to deliver net profit after tax for FY18 in the range of approximately $1,680 to $1,710 million USD at constant currency. Initially, it was expecting profit in the range of $1,550 to $1,600 million USD at constant currency. This was driven due to a positive product and geographic sales mix shift which was better than expected sales of Idelvion® and Haegarda®. It was observed that Seqirus was also performing well due to severe northern hemisphere influenza season. Moreover, the phasing of investments in some of its clinical trials also yielded a positive financial variance. There were few indicators identified which can impact its performance and these include material price and volume movements in plasma products, competitor activity, changes in healthcare regulations and reimbursement policies, royalties arising from the sale of Human Papillomavirus Vaccine and plasma therapy life-cycle management strategies.

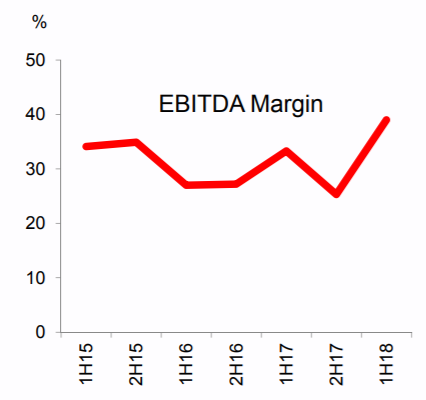

EBITDA Margin Growth (Source: Company Reports)

The current ratio and quick ratio came at 2.86x and 1.42x, respectively in the six months as at 31 December 2017 while debt to equity ratio was moderately down to 1.16x in 1HFY18 from previous six months (1.26x). The Company reported an increase of 12.8 per cent (for six months period ending on 31 December 2017) and 34.8 per cent in revenue (US$4.1 billion) and in NPAT (US$1.1 billion) as compared to the same period in the last year and whereas it recorded an interim dividend of 79.0¢ as compared to 64.0¢ in last year.

Further, the Company completed a buy-back and paid A$150.3 million for the acquisition of shares. On the other hand, the Group has appointed Ms. Fiona Mead to the Board as Company Secretary and Head of Group Governance, effective from June 04, 2018. The Company disclosed to ASX that one of its director Megan Clark had a direct interest in the Company and acquired 290 ordinary shares via on-market acquisition.The stock has moved towards its 52-week high level and looks “Expensive” at the current price of $ 192.620.

BHP Billiton Limited (ASX:BHP)

Financial Assistance to Renova Foundation- BHP agreed to support the Renova Foundation and Samarco Mineração S.A financially and provided US$211 million until 31 December 2018. It confirmed that US$158 million will be used to fund the Renova Foundation to undertake the remediation and compensation programs identified under the Framework Agreement dated 2 March 2016 between Samarco, Vale S.A., BHP Brasil, and the Federal Government of Brazil, the States of Minas Gerais and Espirito Santo and other public authorities. Further, US$158 million will be offset against the Group’s provision for the Samarco dam failure. The Group decided to make US$53 million available as a short-term facility to Samarco to carry out ongoing repair works so that it can maintain Samarco’s facilities and support restart planning. These funds will be released to Samarco only as required, and subject to achievement of key milestones. In 2016, Samarco Mineração S.A. (Samarco), Vale S.A. (Vale), BHP Billiton Brasil Ltda (BHP Brasil) (the Companies), and the Federal Government of Brazil, the Brazilian states of Espirito Santo and Minas Gerais and other public authorities entered into a Framework Agreement that provided for the settlement of the BRL20 billion Civil Claim.

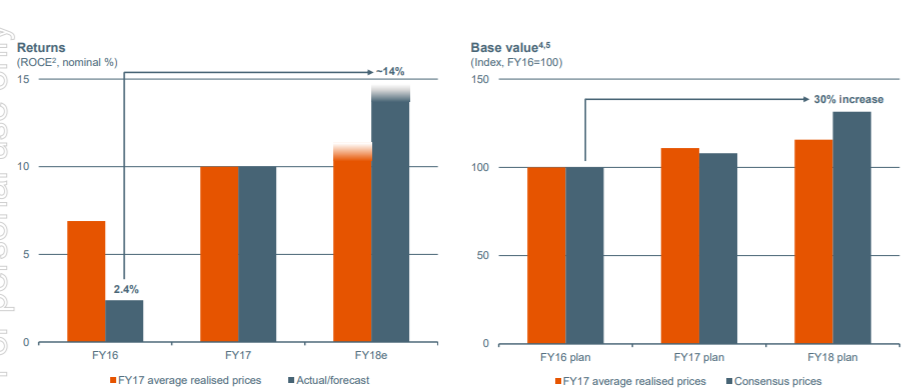

Return and Base Value Trend (Source: Company Reports)

Now under this Government Agreement, the parties have agreed to file a petition with the 12th Federal Court to dismiss the BRL20 billion Civil Claim and further agreed on a process to dismiss certain other public civil actions which covered the same claims as the BRL155 billion Civil Claim. This Government Agreement will provide for the suspension of the BRL155 billion Civil Claim for a period of two years and during these two periods of time the parties will work together to design a single process for the renegotiation of the Programs. The Company recently approved to spend US$ 2.9 Bn on the South Flank Iron Mine Project in the central Pilbara, Western Australia to replace its existing mines. On the financial front, the company recorded revenue at $21,779 Mn in 1HFY18 against $18,796 Mn in 1HFY17, marking a growth of 15.9 per cent on a year on year (YoY) basis at the back of product mix growth and pick up in commodity prices.

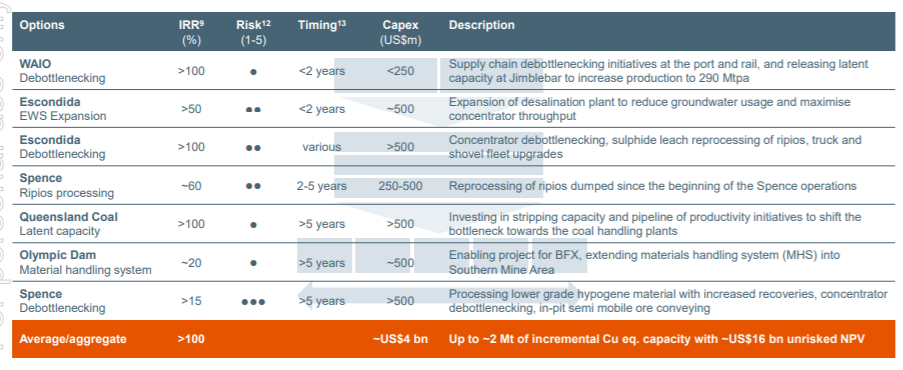

Capacity of the Company’s Projects (Source: Company Reports)

The stock price has been rising for one year and was up by 47.75 per cent as on 28 June 2018. The stock price has recovered significantly since the disaster that took place in November 2015. We maintain our “Hold” recommendation on the stock at the current market price of $ 33.91, considering that the full-year production guidance remains unchanged for Petroleum, Metallurgical Coal and Energy Coal along with other on-going developments, while the commodity environment looks favourable.

Telstra Corporation Limited (ASX:TLS)

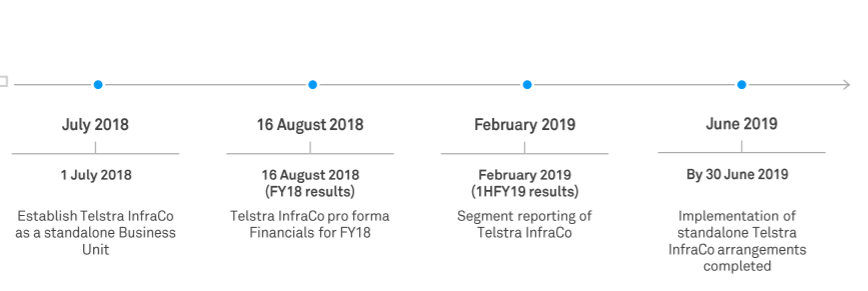

FY19 Dividend scenario yet to be unveiled - The Group has reiterated its FY18 total dividend to be 22 cents per share fully franked including the ordinary and special dividend. It is to be seen whether the group continues to maintain this guidance. The group also maintains a dividend policy to pay a fully franked dividend in the range of 70 per cent – 90 per cent of underlying earnings. Besides this, the group notified that its EBITDA (earnings before interest, tax, depreciation, and amortization) would come in at the bottom end of its guidance of between $10.1 billion and $10.6 billion after absorbing incremental restructuring costs for the same period. The market seems to be disappointed with the FY19 earnings projection along with uncertainty on dividends in the upcoming year. The group is on the cusp of creating a wholly owned standalone infrastructure business unit, called Telstra InfraCo, effective from July 01, 2018.

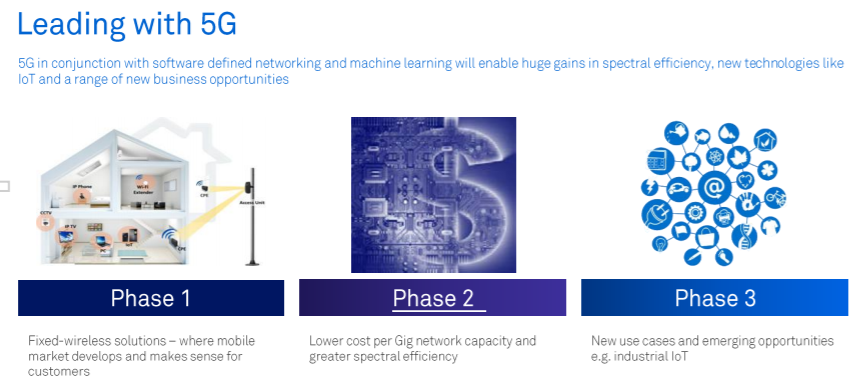

Company’s 5G Technology Overview (Source: Company Reports)

In another release on ASX, the group confirms that there is no change to its capital management framework and expects its Capex to sales ratio in the range of 16-18 per cent in FY19. Further, the group plans to reduce the number of consumers and small business plans from 1,800 to 20 with the objective of simplifying its product portfolio. It works on the strategy to lead the Australian market by simplifying its operations and product set, improving customer experience and reducing its cost base so accordingly the Company has set a target to do the net reduction of employees and contractors by around 8,000 workforces including removing one out of every four executives and middle management roles to flatten the structure. The stock price has been falling since last one year and was down by 39.30 per cent as on 28 June 2018.

Telstra’s InfraCo Timeline (Source: Company Reports)

Hence, we maintain our “Hold” recommendation on the stock at the current market price of $ 2.62, considering the intense competition within the industry and by looking at the initiatives it is taking to manage its shrinking market share within the competitive market while dividend scenario for FY19 is yet to be unveiled.

Macquarie Group Limited (ASX:MQG)

An increase in Debt- The Group announced that it will suspend its Capital Notes (ASX Code: MQGPA) from quotation at the close of trading on Monday, 28 May 2018. The Group announced that these suspensions of Capital Notes will be applicable only for Macquarie Group Capital Notes and not for any other quoted securities of the Company. Recently, it was confirmed that acquisition of Macquarie ordinary shares required for the 2018 profit share and promotion awards under the Macquarie Group Employee Retained Equity Plan (MEREP Awards) was completed and a total of approximately $A454 million of Macquarie ordinary shares were purchased. It is worth noting that the Net operating income of $A10,920 million for the year ended 31 March 2018 increased by 5 per cent from $A10,364 million in the prior year and on the other hand total operating expenses of $A7,456 million for the year ended 31 March 2018 increased by 3 per cent from $A7,260 million in the prior year.

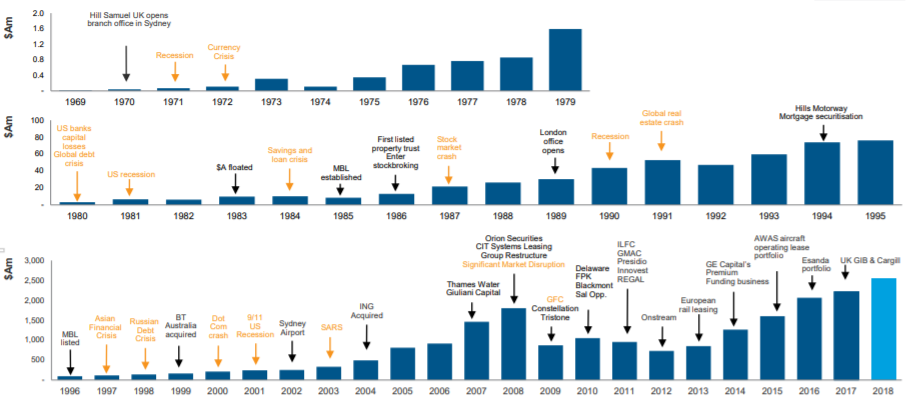

Trend of 49 Years of Profitability (Source: Company Reports)

Total fee and commission income of $A4,670 million for the year ended 31 March 2018 increased by 8 per cent from $A4,331 million in the prior year largely due to higher performance fees from MIRA-managed funds and assets outperforming their respective benchmarks. While net interest and trading income of $A1,182 million for the year ended 31 March 2018 increased 13 per cent from $A1,049 million in the prior year primarily due to a 6 per cent growth in average Australian loan portfolio volumes and a 7 per cent growth in average BFS deposits.Revenues were impacted by sustained low volatility and tighter credit spreads in interest rate and credit products. On the other hand, debt issued at amortised cost of $A53.7 billion at 31 March 2018 increased 6 per cent from $A50.8 billion at 31 March 2017 which was mainly driven by Treasury’s funding and liquidity management activities which included issuance of long-term debt and US commercial paper.

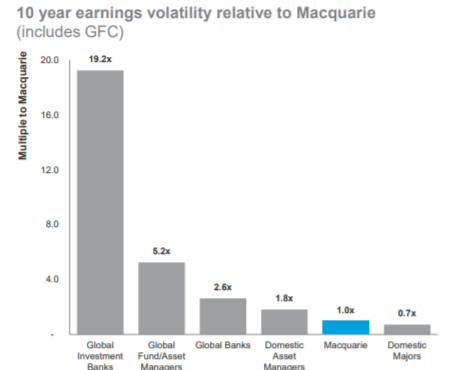

10 Year earnings volatility relative to Macquarie (Source: Company Reports)

Meanwhile, the stock price has been rising since one year but slipped by 2.40 per cent as on 29 June 2018 and closed at $123.65. As the stock is trading at higher levels, we maintain our “Expensive” recommendation at the aforementioned current price.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...