Ramsay Health Care Limited

.png)

RHC Details

Long-Term Player: Ramsay Health Care Limited’s (ASX: RHC) stock edged up 0.48 per cent on August 01, 2018 backed by positive market sentiments related to recent takeover deal with Capio in Europe and this strategic deal can improve the operational efficiency of the business and deliver high-quality and innovative care to the patients in the region which will be resulting to volume growth ahead. At present, the group has 221 hospitals across the globe. Gross margin expanded by 30 bps to 74.2% in 1HFY18 against the previous six months, showing higher margin within the industry median (43.7%). RoE also slightly jumped up 10 bps and recorded 10.7% in 1HFY18. Current ratio and quick ratio stood at 1.0x and 0.88x, respectively in 1HY18 while debt-to-equity was slightly higher than the industry median as the company focuses on growing inorganically via several acquisitions. This strategy could lead to short-term pressure into bottom-line but will provide long-term gain in terms of overall growth.

.png)

Leverage and Cash Management (Source: Company Reports)

It looks to be a good time to enter the market as the share price is under pressure, and we believe that the business has a lot of potential to grow further. Meanwhile, the share price was down by 17.72 per cent in the past six months but up by 5.65 per cent in the past one month (as at July 31, 2018) owing to the several positive updates. Hence, we give a “Buy” recommendation on the stock at the current market price of $56.51 (as it traded near its 52-week low price, that is $53.010) by looking at the group’s potential with upcoming reporting season update and outlook of the healthcare sector ahead.

.png)

RHC Daily Chart (Source: Thomson Reuters)

Greencross Limited

.png)

GXL Details

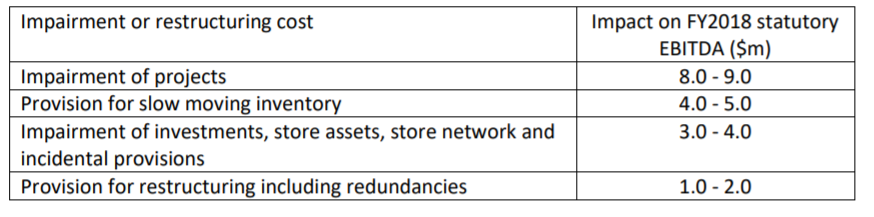

Downgraded its Earnings Guidance for FY18: Greencross Limited (ASX: GXL) is Australia’s largest pet care company, with over 150 veterinary practices and has more than 240 pet specialty retail stores in Australia and New Zealand. GXL is a small-cap company with the market capitalization of circa $511.09 Mn as of August 01, 2018. It offers various services such as vaccination, dentistry, microchip identification, parasite prevention, surgical procedure, laboratory/pathology testing, radiology, ultrasound, and weight loss program services. Recently, the group has downgraded its profit guidance about 9 per cent for the full year due to lower visit numbers in both, GP clinics and in-store clinics. As of now, the group anticipates FY18 EBITDA in the range of $97 Mn to $100 Mn owing to non-cash impairments. However, the group is in line to increase feet into the clinics by introducing retails cross referral programs, focusing on HPP (Healthy Pet Plus) membership, new partnership arrangement with the NSW and Victorian police associations, and senior campaigns and digital marketing activity. Despite some short-term headwinds, the management is confident about its integrated pet-care business model and expects to get back earnings growth in FY19 and thereafter.

Non-Cash Impairment impact for Full year (Source: Company Reports)

Besides this, Wilson Asset Management Group became the substantial holder of the Group by holding 5.20 per cent of the voting power since 22 June 2018. Meanwhile, the share price has fallen 33.02 per cent in the past six months but was up by 1.67 per cent in the past one week as on July 31, 2018. The stock experienced a short interest of 9.78 per cent (as per the ASIC report of 26 July 2018). Based on foregoing, we maintain our “Hold” recommendation on the stock at the current market price of $ 4.280, as the group is in progressing stage while full-year result is expected around 20 August 2018.

.png)

GXL Daily Chart (Source: Thomson Reuters)

Orocobre Limited

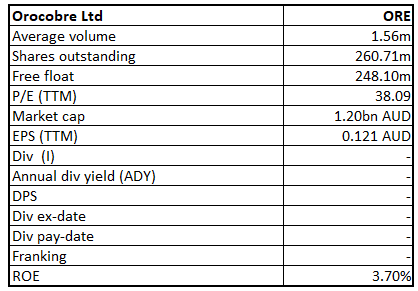

ORE Details

Production in-line and Better Cost Optimization incurred during June Quarter: Orocobre Limited (ASX: ORE) has reported decent update for June quarter in which the production was significantly higher than the previous quarter with both the lithium carbonate plant and the pond system operating well. Resultantly, it demonstrated the improved pond management and harvesting practices despite lower than average evaporation rates through the half. On the financial front, the group achieved realized average price of US$13,653/tonne on a free-on-board basis (FOB) while cash costs for the quarter decreased by 13% on Q-o-Q basis and recorded US$3,800/tonne due to rise in production and sales volumes. In addition, the group reported for US$ 316.6 Mn in cash reserve as at June 30, 2018. Meanwhile, the stock was down by 17.50 per cent in the past three months and by 1.515 per cent on August 01, 2018. Looking at the recent share price underperformance which appears to be related to short selling of around 13.63 per cent (as at 26 July 2018) and volatility in lithium carbonate prices, we maintain our “Hold” recommendation on the stock at the current market price of $ 4.550.

.png)

ORE Daily Chart (Source: Thomson Reuters)

Bellamy's Australia Limited

BAL Details

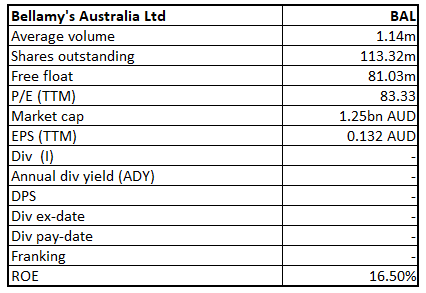

Rising Competition and other challenges: Bellamy's Australia Limited (ASX: BAL) is a small-cap company with the market capitalization of circa $1.25 Bn as of August 01, 2018. It offers various range of organic food and formula products for babies, toddlers, and young children. The group achieved robust performance in first half and recorded revenue growth of 43.7 per cent on Y-o-Y basis due to strong volume growth and a small contribution from the acquisition of the Camperdown Powder manufacturer business. EBITDA margin expanded by 389 bps and recorded 20% in 1HFY18 against 16.1% in 1HFY17. Based on topline growth and cost optimization strategy, the group recorded NPAT growth of 69.7% in 1HFY18 on a Y-o-Y basis.

Despite the robust first half year performance, the company has more challenges such as rising competition (like, challenges due to introduction Nestle’s new a2-protein only infant formula), delays in regulatory approval for the company's China-labelled products, and so forth that could impact the earnings in years ahead. Meanwhile, BAL stock is trading at a very high P/E (83.33x), post a rise of 56.03% in last one year, and many positives are already factored in the stock price. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price of $ 11.19.

.png)

BAL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...