.png)

Stocks’ Details

Scentre Group

Q1FY20 Highlights: Scentre Group (ASX: SCG) is the owner and operator of pre-eminent portfolio of living centres in Australia. The market capitalisation of the company stood at $11.37 billion as on 2nd June 2020. Recently, the company released its results for Q1 FY20, wherein it stated that all its 42 Westfield Living Centres were open and trading throughout the quarter with the highest level of health and safety standards. The company experienced strong operating performance in January and February 2020. SCG executed numerous initiatives targeting a reduction of more than 25% in operating expenses during the COVID-19 pandemic period. The company added that the retailer in-store sales continued to grow during January and February 2020. Comparable specialty in-store sales went down by 7.1% for the quarter to March 2020.

The company has decided that it will not pay an interim distribution for the 1H FY20 in light of the uncertainty regarding the pandemic, its duration, the economic impact, and the timing of operating cash flows for the Group. The company’s annual dividend yield currently stands at 10.32%, which is higher than the industry average (Residential & Commercial REITs) of 6.2% on TTM basis.

.png)

Comparable in-store Sales (Source: Company Reports)

Suspension of Guidance: Considering the impact of COVID-19 and volatility in markets globally, the company has withdrawn its guidance for FY20.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: SCG believes that the decision for not paying distribution for 1H FY20 would further cement its financial position and ability to deliver long term returns to its securityholders. The company has recently priced a US$1.5 billion debt issue in the United States market. SCG would use these proceeds to repay existing indebtedness including borrowings under the Group’s revolving bank facilities. In April 2020, the Group increased its liquidity to $3.1 billion. Over the span of four years, i.e. 2016-2019, the company reported a CAGR of 5.04% in free cash flow. This implies that the company is effectively using its working capital.We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of lower double-digit (in percentage terms).

Therefore, considering the strong operating performance during January and February 2020, increased liquidity, steps taken to strengthen the financial position, we give a “Buy” recommendation on the stock at the current market price of $2.310 per share, up by 5.479% on 2nd June 2020.

Suncorp Group Limited

Impact of COVID-19: Suncorp Group Limited (ASX: SUN) is engaged in the provisioning of banking, insurance, wealth and other financial solutions to the retail, corporate and commercial sectors. The company entered the uncertain period of COVID-19 in a decent financial position with group Excess Common Equity Tier 1 of $682 million as at 31 March 2020. The company added that the COVID-19 has had numerous impacts across the Insurance (Australia) business portfolio. There has been a significant negative impact from mark-to-market adjustments due to recent volatility in investment markets. COVID-19 would also have a significant impact on consumer motor claims frequency and landlord loss of rent claims.

During 1H FY20, the company declared ordinary interim dividend of 26 cents per share, reflecting a payout ratio of 89.5% of cash earnings. Over the span of four years (2016-2019), the group has maintained an average dividend yield of 5.22%

.png)

Group Excess CET1 (Source: Company Reports)

Outlook: For FY20, the company expects the cost base to be slightly above $2.7 billion. SUN will be focused on maintaining a robust capital position. Moreover, SUN would consider final ordinary dividend during the normal process of preparing the year-end accounts.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As of now, the Group is well capitalised, with capital levels in excess of what is required to cover the expected deterioration as a result of COVID-19. The company is focused on building the long-term sustainability of the organisation with the acceleration of digital strategy to meet changing customer demands. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of lower double-digit (in percentage terms).

Hence, in light of decent financial position, well-capitalised business, and focus on building the long-term sustainability of the organisation, we give a “Buy” recommendation on the stock at the current market price of $9.300 per share, up by 1.197% on 2nd June 2020.

SkyCity Entertainment Group Limited

Reopening of Casinos: SkyCity Entertainment Group Limited (ASX: SKC) is in the gaming entertainment business. The market capitalisation of the company stood at $1.61 billion as on 2nd June 2020. Following the announcement made by the government of New Zealand that COVID-19 has been moved down to level 2 from level 4, the company has decided to reopen its casinos in New Zealand, entertainment and accommodation facilities in Auckland, Hamilton and Queensland. However, the company would reopen its New Zealand properties in a staged manner with reduced operating hours initially based on expected customer demand. During 1H FY20, the normalised and reported EBITDA of the company stood at $153.3 million and $407.5 million, respectively. This was driven by positive performance from domestic NZ businesses on an LFL basis.

During 1H FY20, the company declared a fully imputed interim dividend of 10 cents per share, which was in line with its policy. Moreover, it maintained an attractive dividend yield (1H FY13- 1H FY20) in the low- interest rate environment.

.png)

DPS and Cash Dividend Yield (Source: Company Reports)

Guidance Suspension: As per the release dated 23rd March 2020, the company has suspended its earnings guidance for the year ending 30 June 2020 considering the closure of Adelaide Casino.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Net margin of the company stood at 21.1% in 1H FY20 as compared to the industry median of 7.8%. This implies that SKC has decent capabilities to convert its topline into the bottom line against the peer group. Return on equity of the company stood at 6.8% against the industry median of 5.4%. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Crown Resorts Ltd (ASX: CWN), Tabcorp Holdings Ltd (ASX: TAH) and Aristocrat Leisure Ltd (ASX: ALL).

Hence, considering the reopening of casino in New Zealand, attractive dividend yield during 1H FY13- 1H FY20, and positive performance from domestic NZ businesses, we give a “Speculative Buy” recommendation on the stock at the current market price of $2.390 per share, down by 0.83% on 2nd June 2020.

Alumina Limited

Decent Returns Paid to Shareholders: Alumina Limited (ASX: AWC) makes investment in bauxite mining and alumina refining through its joint venture with Alcoa World Alumina & Chemicals (AWAC). During FY19, the company reported a statutory net profit after tax amounting to US$214.0 million as compared to US$635.4 million in FY18. However, the company believes that these numbers are still strong.

AWC declared a total dividend of US$8 cents per share during FY19. Over the span of the last three years, the company has paid $1.3 billion in the form of dividends. The company’s annual dividend yield currently stands at 7.97% as compared to the industry average (Metals & Mining) of 4.4% on TTM basis. The company maintained three years (2017-2019) average dividend yield of 8.6%.

.png)

Dividend (Source: Company Reports)

Focus for FY20: During FY20, the company expects growth in demand and production of Aluminium. The company is also focused on good options to grow low cash cost alumina production in order to meet expected future market demand growth.

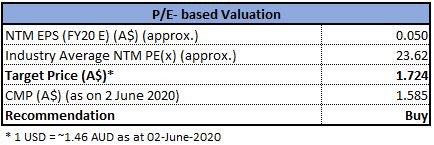

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company has a strong balance sheet with a low gearing of 3.0%. AWC possesses a proven business model with investment in the world’s largest third-party producer of alumina. We have valued the stock using a Price-to-Earnings multiple based illustrative relative valuation method, and for the purpose, we have taken peers such as South32 Ltd (ASX: S32), BlueScope Steel Ltd (ASX: BSL), Sims Ltd (ASX: SGM), Rio Tinto Ltd (ASX: RIO), etc. As a result, we have arrived at a target of high single-digit upside (in percentage terms). The stock of AWC has corrected 21.91% and 34.70% during the span of three months and six months, respectively and is inclined towards its 52-week low levels of $1.295, offering decent opportunities to accumulate. Hence, it can be said that the stock of AWC is undervalued at current trading levels.

Thus, considering the strong balance sheet, proven business model, decent returns to shareholders, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $1.585 per share, up by 4.62% on 2nd June 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...