Stocks’ Details

Flight Centre Travel Group Limited

Decent Outlook but higher levels: Flight Centre Travel Group Limited (ASX: FLT) share price climbed up 3.8 per cent on July 11, 2018 at the back of positive market sentiments in relation to expecting better results for the full year, tentatively due on August 23, 2018. During the year, the company has completed several deals and events such as network consolidation which saw overall sales staff numbers decrease modestly, pointing to further productivity gains; the Transformation program that was initiated late in FY17 to ensure that the group achieves scalable profitable growth throughout the economic sale has started to gain momentum and the company made a solid progress towards its 7-2-100 targets in the first half, expanded international business, etc. Besides this, the court imposed a penalty of $12.5 Mn on the group in relation to the competition law test case, which was initiated by the ACCC in 2012. However, the management stated that this penalty will not affect FLT’s market guidance for FY18 on underlying profit before tax, thus revised the same upwardly in the range of $360 Mn-$385 Mn as compared to its initial target of $350 Mn-$380 Mn. Penalty will be included in the Group’s statutory results for the year. Meanwhile, it was seen that share price has increased in the past six months by 43.30 per cent (as at July 10, 2018). The stock is trading on a higher side and looks “Expensive” at the current market price of $ 64.610, which is inching towards the top end of its 52-week range.

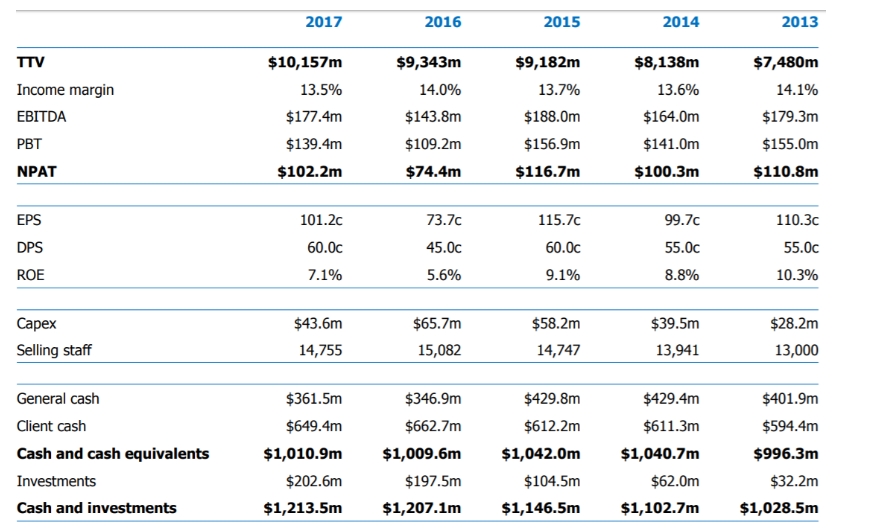

5-Year Historical Performance (Source: Company Reports)

Qantas Airways Limited

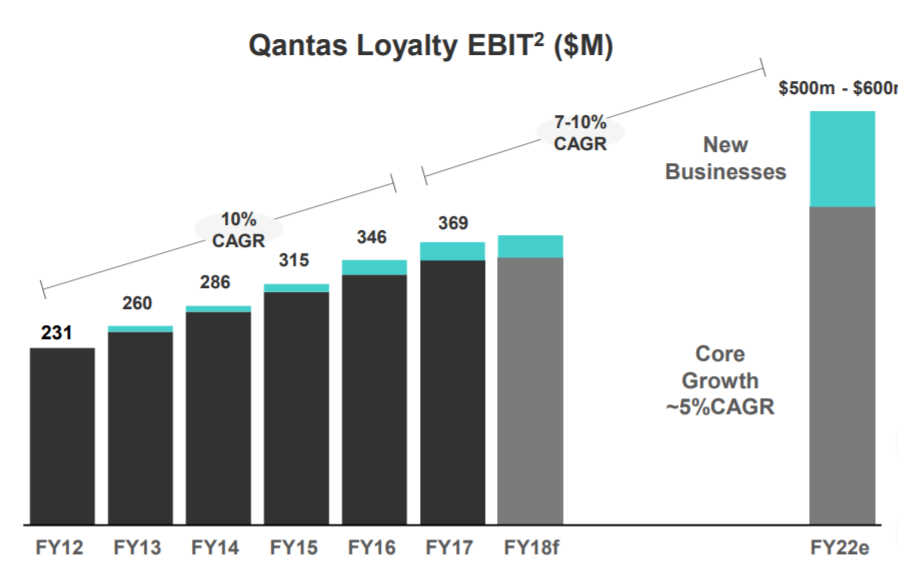

Positioned for Growth and Sustainable Returns: Qantas Airways Limited (ASX: QAN) is an iconic Australian company and one of the best-performing airline groups in the world. The Group recorded strong performance in its trading update for the third quarter of FY18 and confirmed that they are on track to record underlying profit before tax for the full-year. Revenue from the operation of the company grew by 7.5 per cent to $4.25 Bn versus prior corresponding period (pcp) while Group Unit revenue (RASK) increased by 6 per cent as compared to same period last year. In the late March, the company took several important decisions in relation to changing its international network, for instance, the start of the Perth-London route, the switch from Dubai to Singapore as the hub for the group’s second London services and renewed partnership with Emirates that has seen Qantas increase its Trans-Tasman flying – ensuring significant benefits to Qantas International’s performance from FY19 onwards. As at 31 March 2018, the company had completed almost 50% market share buy-back event. The company focuses on to do strategic investment to provide Qantas loyalty with a path to deliver 7-10% EBIT CAGR over FY17-22E.

Qantas Loyalty EBIT ($M) (Source: Company Reports)

As at April 2018, the company had hedged circa 70% of its expected fuel cost for FY19 and holds noteworthy participation to fall in oil price. Moreover, the ongoing transformation along with capacity and revenue management strategy will support to mitigate the impact of higher fuel costs going forward. Based on foregoing, the group expects a full year underlying profit before tax of between $1.55 Bn and $1.60 Bn. As of now, the stock is trading at a reasonable PE level i.e., 12.58x. Hence, we maintain our “Buy” recommendation on the stock at the current market price of $ 6.540 (down by 1.4 per cent on July 11, 2018), considering robust outlook and sustainable return based on strong fundamentals and other developments such as synergistic joint ventures, renewed codeshare deal with several partners.

Sydney Airport

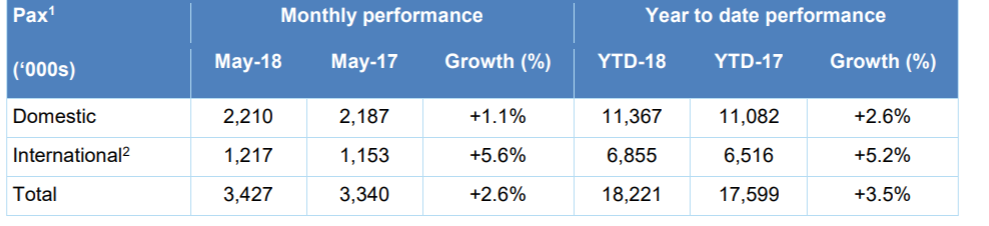

Improvement in Traffic Performance: Sydney Airport (ASX: SYD) disclosed its May month traffic performance in which total passenger traffic grew by 3.5% during the month of May compared to the prior corresponding period (pcp). This contains domestic traffic growth of 1.1% and international traffic growth of 5.6% on pcp basis. The domestic growth was mainly driven by a 0.9 per cent point improvement in load factors while it kept airline capacity as constant in the May month. Although, the group has experienced positive load factor and capacity due to increase in passengers traffic year on year across the globe wherein Vietnam, USA, India, China, and Hong Kong contributed to inbound passengers traffic (approximately 24.3%, 12.8%, 9.1%, 6.3%, and 6.3% respectively) in May’18. Moreover, International passenger growth was predominantly driven by the delivery of additional seat capacity. Further, the management expects that the same trend will be continued in 2018 and reaffirms its distribution guidance at 37.5 cents per securities for the full year. This represents a growth of 8.7% over 2017.

Sydney Airport Traffic Performance May 2018 (Source: Company Reports)

Besides this, the company has recently appointed Marianne Kopeinig to the Board as a co-company secretary of the company, effective from 28 May 2018. Meanwhile, the share price was up by 9.79 per cent in the past three months (as at July 10, 2018) but plunged 3.3% on July 11, 2018; and it is currently trading at high PE level reflecting to be slightly high in terms of the current price scenario. Hence, we maintain our “Expensive” recommendation on the stock at the current market price of $ 7.050.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...