Telstra Corporation Limited

5G Expected to Be Transformative for Revenue Growth: Telstra Corporation Ltd (ASX: TLS) has lately declared that it has priced a EUR 600 million bond issue (the Notes) under its Debt Issuance Program Offering circular dated 12 March 2019. The notes have a coupon of 1.375% and have matured on 26 March 2029. Telstra will use the proceeds from the notes for general corporate purposes. Thus, the number of securities issued or to be issued or the maximum number which may be issued would be 6,000 Notes with a minimum denomination of EUR 100,000. The issue price has been decided to be EUR 99.935 per EUR 100 of the principal amount.

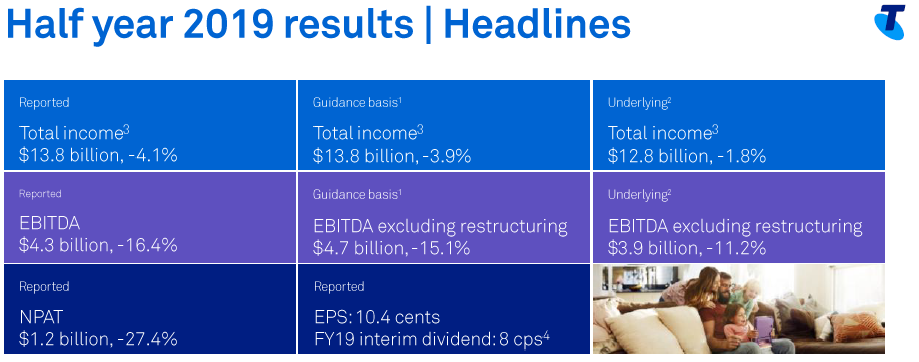

As regards the results for the half-year ended 31 December 2018, the total income on a reported basis was $13.8 billion, reflecting a fall of 4.1 per cent on PCP basis.The EBITDA on a reported basis was $4.3 billion which was down 16.4 per cent. While, the company’s NPAT was $1.2 billion, down 27.4 per cent on PCP basis. The financial results of the company got weighed by the further rollout of the nbn™ network.

TLS’s HY 2019 Financial highlights (Source: Company Reports)

The company has provided FY 2019 guidance. It expects to achieve a total income of $26.2 billion-$28.1 billion and EBITDA (excluding restructuring costs) of $8.7 billion to $9.4 billion in FY19. The company is expected to post free cash flow in the range of $3.1 and $3.6 billion. As regards the 5G technology, the management believes that the 5G will be transformative for the industry and will offer opportunities for revenue growth. They expect customers would be willing to pay more to access this new technology. Also, there are expectations that 5G would enable new revenue streams.

Meanwhile, the stock has risen by 3.49% in the past six months. Even though there are short-term challenges, the company’s management is positive about Telstra’s prospects for the future.

In the past three months, the company’s stock as delivered the return of 19.18%.

Considering the above factors, we maintain our “Hold” recommendation on the stock at the current market price of A$3.310 per share (up 1.223% on April 03, 2019).

Vocus Group Limited

Proposed 5G rollout & expansion opportunities: Vocus Group Ltd (ASX: VOC) has recently stated that one of its directors, Mr. David Stoddart Wiadrowski acquired 3,000 ordinary shares via on-market trade for a cash consideration of $11,040 as on 29 March 2019. Hence, after this development, Mr David Stoddart Wiadrowski holds 19,000 ordinary shares in his indirect capacity.

The company had earlier inked a five-year extension of its current Mobile Virtual Network Operator (“MVNO”) agreement with Optus Wholesale. This will involve access to the Optus 5G network and future technologies. The partnership is expected to drive growth & synergies for both the businesses and hence will provide a platform for Vocus to grow its mobile customer base.

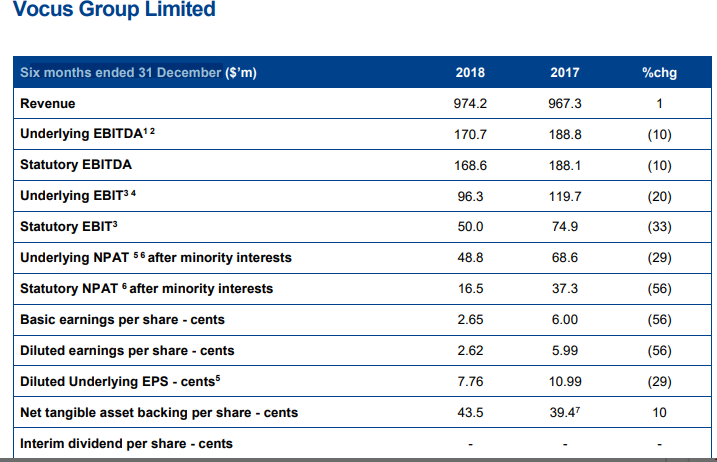

VOC’s Financial Highlights (Source: Company Reports)

The revenue for the six months ended 31 December 2018 increased slightly on the previous corresponding period (pcp) to $974.2 million, up by 1% on the pcp. This marginal growth was witnessed on the back of growth in Vocus Networks but offset by declining revenues in Vocus Retail. The company had been managing capex tightly and the focus is towards growth opportunities, digital enablement and network capacity.

What to Expect From VOC: As regards the outlook, the management believes that with the new leadership team in place, the company will continue to build momentum. The management has reiterated the expectations for FY19 Underlying EBITDA to be between $350 million - $370 million.

Also, the company has significant opportunities going forward in terms of real brand equity, new Optus MVNO opportunity, including 5G and significant customer base (in complementary segments).

Meanwhile, the stock price has risen over the past six months by 8.79% and is trading slightly towards to 52-week high level of $3.890. Hence, considering the recent five-year extension of its current Mobile Virtual Network Operator (“MVNO”) agreement with Optus Wholesale coupled with the significant customer base, we maintain our “Hold” rating on the stock at the current price of A$3.600 per share.

TPG Telecom Limited

Key Highlights of 1H FY 2019 Results: TPG Telecom Limited (ASX: TPM) had made an announcement of the results for half-year ended January 31, 2019 in which it posted EBITDA before impairment of $420.0 million. During the same period (i.e. 1H FY 2019), the company posted NPAT amounting to $46.9 million and its EPS stood at 5.1 cents per share. The company also stated that it is necessary to recognise an impairment expense amounting to $227.4 million in 1H FY 2019 which was the result of decision to cease rollout of the Australian mobile network. The company’s underlying EBITDA got adversely impacted by a loss of margin as DSL and home phone customers migrated to the low margin NBN services, however, TPG Telecom managed to offset these headwinds in 1H FY 2019.

.png)

Bridge between underlying 1H FY 2018 and 1H FY 2019 EBITDA (Source: Company Reports)

The company had made an announcement of interim FY19 dividend of 2.0 cents per share (fully franked) which is in line with last year and would be payable on May 21, 2019 to the shareholders who will register on or before April 16, 2019.

What to Expect from TPG Telecom: The company had reaffirmed the guidance which was given in September 2018 and stated that BAU (or Business as usual) EBITDA for FY19 is anticipated to be between $800 million-$820 million and BAU capex might be between $180 million-$220 million. As at January 31, 2019, the company incurred capital expenditure of around $100 million towards design, planning, acquisition and construction costs with respect to its Australian mobile network. The substantial component of the capital expenditure is related to the acquisition and installation of Huawei equipment. The company had reassessed the carrying value of the mobile network assets and key factors which were considered in the fair value assessment were the fact that the Huawei equipment has been banned from use in any 5G networks in Australia, the limited alternative uses of Huawei equipment as well as the alternative uses of non-Huawei assets.

Stock Recommendation: On the YTD basis, the stock of TPG Telecom had delivered a 7% return. From the valuations perspective, the company’s P/B ratio stood at 2.23x as compared to peer median of 2.68x which reflects that the company’s stock is, more or less, fairly valued. Also, the company’s top line had witnessed the CAGR of 26.61% over the span of five years to FY 2018 (i.e. from FY 2014-FY 2018).

Considering the decent business outlook coupled with the decent CAGR growth over the span of five years to FY 2018 (as mentioned) in its top line, we maintain our “Hold” rating on the stock at the current price of A$6.820 per share (up 1.337% on 3 April 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...