Stocks’ Details

WiseTech Global Limited

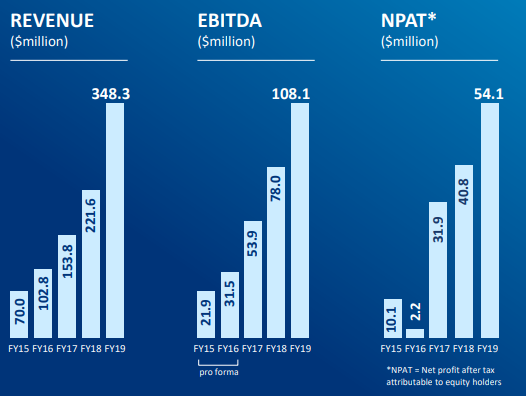

Decent Growth in Revenue and NPAT: WiseTech Global Limited (ASX: WTC) is a provider of software solutions to the logistics industry globally. As on 19 November 2019, market capitalisation of the company stood at ~$9.19 billion. In its recent annual general meeting, the top management of the company addressed the shareholders and stated that the business has experienced strong growth with revenues up by 57% to $348.3 million from $221.6 million in FY18. Net profit after tax (NPAT) attributable to equity holders increased to $54.1 million from $40.8 million in FY18.WTC declared a fully franked final dividend of 1.95 cents per share for FY19 and provided its shareholders with a total return of 77.1%.

Financial Performance (Source: Company Reports)

What to Expect: During the year, the company reported a healthy balance sheet, supported by net cash flows from operating activities of $112.5 million. WTC expects revenue for FY20 to be in the range of $440 million to $460 million, with growth in the range of 26% to 32%. It expects EBITDA growth (Earnings before Interest, Taxes, Depreciation and Amortization) to be between $145million to $153 million, representing growth in the range of 34% to 42%.

Stock Recommendation: As per the ASX, the stock of WTC gave a return of 28.08% in the past six months. Over a period of one year, the stock generated a return of 78.54%. At the current market price of $26.650, the stock is trading at a price to earnings multiple of 163.110x. EV/Sales multiple of the stock stands at 22.8x, which is higher than the industry median of 4.9x. Price to book multiple of the company stands at 12.0x, higher than the industry median of 3.4x. Given the backdrop of the above factors, decent outlook for FY20, higher valuations, and decent price movement in the last one year, we suggest investors to adopt a wait and watch stance on the stock at the current market price of $26.650, down by 7.69% on November 19, 2019, taking cues from the AGM 2019.

Link Administration Holdings Limited

Divestment of CPCS Business in FY19: Link Administration Holdings Limited (ASX: LNK) provides technology-enabled administration, securities registration and asset services, and pension and superannuation funds across the globe. The company has recently announced an on-market buy back of 75,000 shares for a total consideration of $442,380, taking total shares bought back to date to 1,075,595. In the recently held Annual General Meeting of LNK, the top management of the company addressed its shareholders and acknowledged that revenue for the 12 months ended 30 June 2019 increased by 17% to $1.4 billion, in comparison to the prior corresponding period and operating EBITDA went up by 6% on the prior year to $356 million.

During the year ended 30 June 2019, statutory NPAT increased by 123% and stood at $320 million. The company also declared a fully franked dividend of 12.5 cents per share, bringing the total dividend to 20.5 cents. Recently, the company has divested its CPCS business to Apex Group Limited for a consideration of $434 million.

Financial Performance (Source: Company Reports)

What to Expect: Looking forward, the company is executing on a series of initiatives to drive both short-term and medium-term shareholder value. The Global transformation program of the company is on track and it anticipates the one-off costs to be in the range of $50 million to $60 million over the next 3 years, which will produce sustainable cost reductions of at least $50 million per annum. A lower contribution from RSS will be offset by growth in other businesses. The company anticipates that operating EBITDA for the continuing business to be stronger in the second half. Revenue and operating EBITDA from the RSS business are expected to be in the range of $480m-$500m and $60m-$70m, respectively.

Stock Recommendation: As per the ASX, the stock has corrected 23.24% in the last six months but generated a positive return of 23.01% in the past three months. The stock is currently inclined towards its 52-week lower levels of $4.5. Over the period of FY15 to FY19, the company witnessed a CAGR growth of 24.28% in revenue and CAGR of over 200% in net income. Gross margin and net margin of the company stand at 92.2% and 22.8%, higher than the industry median of 76.2% and 17.8%, respectively. This indicates that the company is efficiently managing its cost. Considering the above-mentioned metrics, a modest outlook for FY20, and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $5.790, down by 1.531% on 19 November 2019.

Vista Group International Limited

Acquisition of Numero Limited: Vista Group International Limited (ASX: VGL) is in the business of sale, support and associated custom development of software for the cinema industry, online cinema ticketing website and online data analysis and marketing. The company announced that it has acquired the remaining 50% of Vista Group associate company Numero Limited from Stuyar Pty Limited in return for a consideration in cash and Vista Group shares. The final consideration was determined based on specific earnings and revenue targets being achieved by Numero Limited over the coming two years.

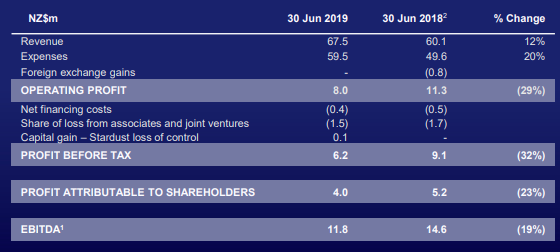

Financial Highlights for the Half Year ended 30 June 2019:For the half year, revenue for VGL went up by 12% to NZ$67.5 million, from NZ$60.1 million in FY18.During the year, the company witnessed a rise in expenses by 20%. This led the operating profit to decline by 29% to NZ$8 million from NZ$11.3 million in the previous year. EBITDA margin from Core businesses sustained as a result of higher revenues, but Vista Group profit and EBITDA was impacted by revenue reductions from Vista China and movieXchange, and adverse FX movement, witnessing a decline of 23% and 19%, respectively.

Financial Performance (Source: Company Reports)

What to Expect: The company plans to simplify its operations for 2020 with reseller relationships, limited to India and Pakistan. It also plans to increase its target market through new products, geographical expansion, etc. The company is on a constant drive to achieve its recurring revenue target of 80%+ in 2025. It expects a slower revenue growth in 2021-2022 before higher growth in future years.

Stock Recommendation: As per the ASX, the stock of VGL gave a negative return of 30.37% in the past 6 months and a positive return of 2.86% in the last one month. The stock of VGL is trading close to its 52-week low of $3.300. During the first half ended 30 June 2019, EBITDA margin of the company stood at 17.4% as compared to the industry median of 27.1%. Return on Equity stood at 2.7% in comparison to the industry median of 7.3%. The stock is currently trading at a price to earnings multiple of 54.380x. Considering the volatility in returns, lower EBITDA and ROE as compared to the industry and the long-term outlook, we have a wait and watch stance on the stock at the current market price of $3.620, up by 0.556% on November 19, 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...