.png)

Stocks’ Details

Xref Limited

Successfully Raises $3.48 Mn via Share Placement:Xref Limited (ASX: XF1) is involved in developing human resources technology that automates the candidate reference process for employers. Recently, the company successfully completed its $3.48 Mn placement, via the issue of 10,533,333 fully paid ordinary shares to institutional and professional investors. The placement price was set at $0.33, with the condition that the new shares will be ranked pari passu with existing ordinary shares.The proceeds are expected to be utilized to support further growth of Xref, including additional sales and marketing capability, technology development and working capital requirements and other general corporate purposes. The company aims to reach cash flow break-even in 2020. In another update, Timothy Mahony resigned as a Non-Executive Director of the Company. He was also the Chairman of the Audit and Risk Committee and member of the Remuneration and Nomination Committee.

September’19 Quarter Key Highlights: For the first quarter of FY20, sales of the company increased by 23% to $2.46 Mn y-o-y. Credit usage stood at $2.24 Mn, up 32% on pcp. Cash receipts during the quarter stood at $3.53 Mn as compared to $2.7 Mn in the prior corresponding quarter. The company added several clients during the quarter like the Ministry of Social Development, New Zealand, Tourism Australia & Schneider Electric, Australia, to name a few. Cash and cash equivalents at the end of the quarter were reported at $5.25 Mn. Cash used in operations came in at $1.95 Mn.

.png)

September’19 Quarter Operating Cash Flow Statement (Source: Company Reports)

What to Expect: In the coming quarter, the company is expecting net cash outflow amounting to ~$5.3 Mn.

Stock Recommendation:Xref Limited’s shares generated a negative YTD return of 28.72%, and in the span of one year, posted a negative return of 30.21%. Its current ratio for FY19 was reported at 1.31x, better than FY18 result of 1.22x, which implies an improvement in the company’s liquidity position. Considering company’s growth trajectory throughout Q1FY20, direct sales growth, partnerships, acquisitions, recent capital raising and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $0.380 up 13.433% on December 18, 2019, on account of successful capital raise via placement.

Hansen Technologies Limited

HSN Structures Business Activities into Two Verticals:Hansen Technologies Limited (ASX: HSN) is involved in the development, integration and support of billing systems software for the utilities, energy, pay-TV and telecommunications sectors. Recently, Mawar Investment Management Ltd. ceased to be a substantial holder in the company with effect from December 16, 2019.

In another update, the company announced the formal structuring of its business activities around two industry verticals i.e., communications and utilities. In June 2019, the company acquired Sigma Systems, whose customers were mainly in the communication sector. Following the acquisition, group revenue is now equally balanced between the two verticals. Niv Fernando will be leading the utilities division as CEO, which comprises energy and water customers, whereas Simon Muderack will be leading the communications division which comprise telecommunications and pay-tv customers.

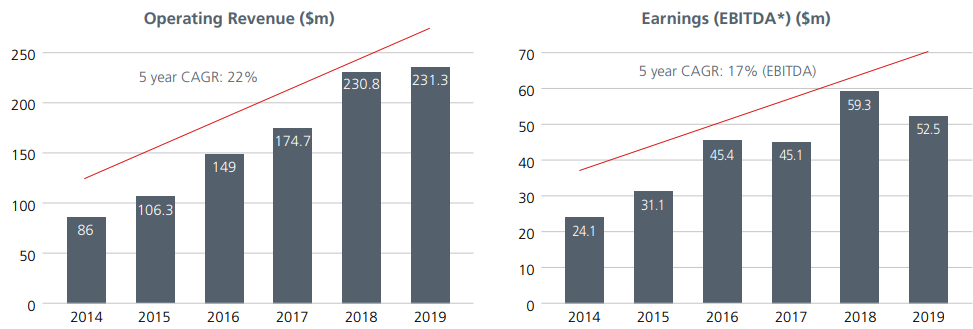

FY19 Key Highlights for the Period Ended June 30, 2019:The company reported revenue amounting to $231.3 Mn, up 0.2% on prior corresponding period. Underlying EBITDA for the year came in at $55.8 Mn, down 6.9% on the previous year. As a result, underlying EBITDA margin declined from 26.0% in FY18 to 24.1% in FY19. Underlying NPATA for the year stood at $33.7 Mn, down 12.8% on the prior corresponding year. Adjusted earnings per share came in at 17.1 cents, representing a decline of 13.5% on FY18 EPS of 19.8 cents.

Past Performance for Operating Revenue and EBITDA (Source: Company Reports)

What to Expect: As per the management’s guidance, operating revenue for FY20 is expected to be in the range of $305 million - $310 million. EBITDA for the period is expected to be between $70 million and $76 million.

Valuation Methodologies:

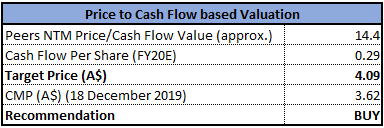

Method 1: Price to Cash Flow Multiple Approach

Price/Cash Flow Based Valuation (Source: Thomson Reuters)

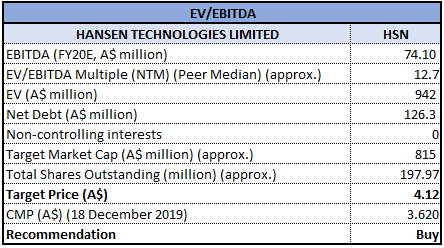

Method 2: Enterprise Value to EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated a positive YTD return of 4.00%, while in the span of three months it posted a return of 12.69%. Currently, the stock is trading above the 52-week high and low level of $4.290 and $2.850, respectively. Considering the operational performance in FY19 in terms of acquisitions, new contracts, product expansion, strong cash generation capacity, anticipated benefits from newly signed contracts and acquisitions, decent guidance for FY20 and current trading levels, we have valued the stock using two relative valuation methods, i.e., Price/Cash Flow multiple approach and EV/EBITDA multiple approach, and arrived at a target price with lower double-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $3.620, down 0.549% on December 18, 2019.

NEXTDC Limited

Product Launches & Acquisition Synergies: NEXTDC Limited (ASX: NXT) is a technology company that builds and operates independent data centres in Australia.

Shareholding Update: On 16th December 2019, the company issued an announcement stating that UniSuper Limited, which is a substantial holder of the company, has reduced its voting power from 9.64% to 8.47%.

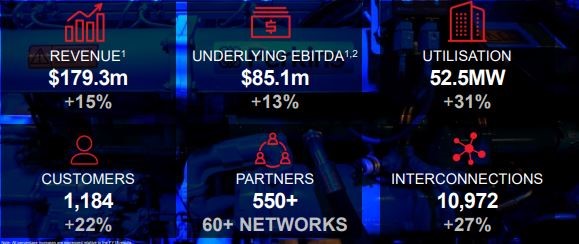

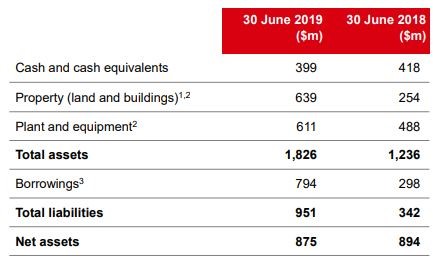

Financial Highlights for FY19 Period Ended 30 June 2019: The company reported revenues of $179.3 million, up 15% year over year. Underlying EBITDA for the period came in at $85.1 million, an increase of 13% on a year over year basis. Statutory net loss after tax was for the period was $9.8 million. Underlying capital expenditure stood at $378 million, as compared to $285 million in FY18. The company’s sale from contracted utilisation went up by 31% and reached 52.5MW during the period. Interconnections in FY19 increased by 27% to 10,972. Operating cash flows for the period came in at $39.4 million. The company exited the year with cash and cash equivalent of $399 million as compared to $418 million at the end of FY18.

Financial Highlights (Source: Company Reports)

Cash Details (Source: Company Reports)

Outlook: For FY20, the company expects revenues to be in the range of $200 million to $206 million.Underlying EBITDA is expected to be in the range of $100 million to $105 million. The company expects

capital expenditure to range between $280 million and $300 million.

Stock Recommendation: The stock is trading above the average of its 52-weeks low and high of $5.650 and $7.250, respectively. As on 18 December 2019, the company’s market capitalisation stands at ~$2.37 billion, with 345.39 million outstanding shares. The shares of the company have increased approximately 13% on a year-to-date basis. In FY19, the company also completed the acquisition of land and building, which led to annual rental savings of approximately $15 million. The company has set up a robust sales pipeline across its operating markets. The company also expects growth in cloud and mobile computing, along with growing internet traffic to favourably impact the business in near future. Further, the company’s strategies to launch new products is another key catalyst. Considering the above factors, we recommend a “Buy” rating on the stock at the closing price of $6.750 per share, down by 1.747% on December 18, 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...