.png)

Stocks’ Details

Appen Limited

Strong Performance by Core Business: Appen Limited (ASX: APX) is engaged in the provision of quality data solutions and services for machine learning and artificial intelligence applications. As per a recent announcement, the company updated that it has issued 7,033 new fully paid ordinary shares as a result of the vesting of performance rights.

1H19 Results Highlights: Revenue for the six months ended 30 June 2019 amounted to $245.1 million, up 60% in comparison to the prior corresponding period. In the first half, the company reported Underlying EBITDA of $46.3 million, up 81% on prior corresponding period. Underlying NPAT for the period increased by 67% on pcp at $29.6 million. Relevance revenue for the first half was reported at $193.7 million, rising 48% in comparison to the prior corresponding period.

.png)

Financial Summary (Source: Company Reports)

Acquisition Update: The company closed the acquisition of Figure Eight on 2 April 2019. The acquisition is helping the company to accelerate its technology roadmap, diversify its revenue, and expanding the market for its products.

FY19 Forecast: The company notified that its full-year underlying EBITDA, including the results of Figure Eight is trending to the upper end of the guidance range of $85 million - $90 million.

Stock Recommendation: The stock of the company generated negative returns of 3.99% and 9.45% over a period of 1 month and 3 months, respectively. The company reported strong performance in the first half with Speech & Image data growing 85% on prior corresponding period, relevance revenue increasing by 48% and underlying EBITDA margin expanding from 16.8% to 18.9%. Moreover, the acquisition of Figure Eight in April 2019 is delivering well on its strategic thesis. The company, through investments in technology, sales & marketing, government markets and China, is continuously strengthening its position in a high growth market. Considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $23.070, down 5.179% on 11 September 2019.

NEXTDC Limited

Period of Record Revenue and EBITDA: NEXTDC Limited (ASX: NXT) is engaged in the development and operation of independent data centres in Australia. The company recently announced the appointment of Jennifer Lambert as a non-executive director, with his tenure beginning on 01 October 2019.

Shareholding Updates: In the recent announcement, the company updated about an increase of voting power of Greencape Capital Pty Ltd. from 5.39% to 6.41%. As per another update, the company added Vanguard Group to the list of substantial shareholders with voting power of 5.015%.

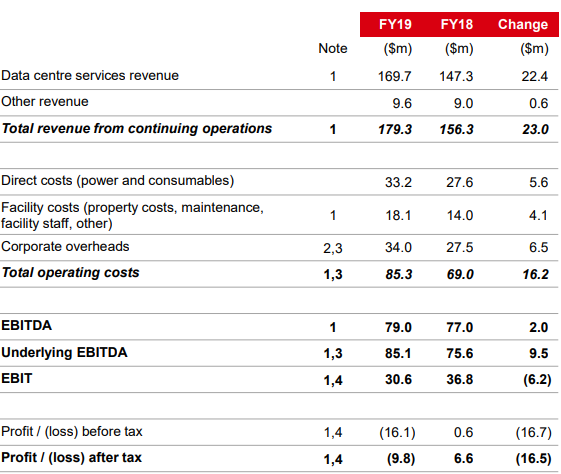

FY19 Results: In FY19, revenue amounted to $179.3 million, representing an increase of 15% on prior corresponding period revenue of $156.3 million. Underlying EBITDA for the period amounted to $85.1 million, up 13% on the prior corresponding period value of $75.6 million. During the year, the company incurredastatutory net loss, amounting to $9.8 million, as compared to the prior corresponding period loss of $6.6 million. Operating cash flow for the year was reported at $39.4 million, as compared to $33.4 million in pcp.

FY19 P&L Summary (Source: Company Reports)

FY20 Guidance: In FY20, capital expenditure is expected to be in the range of $280 million - $300 million. The company expects revenue to be in the range of $200 million - $206 million. FY20 Underlying EBITDA is anticipated to be in the range of $100 million - $105 million.

Stock Recommendation: The company’s stock generated negative returns of 1.89% and 9.86% over a period of 1 month and 3 months, respectively. During the year the company acquired land and buildings at S1, B1, M1 and P1, that helped deliver rental savings of approximately $15 million p.a. and strengthened the balance sheet. FY19 was another year of record revenue and EBITDA along with significant investment in the next generation of world-class Tier IV data centers. In FY19, the number of customers on the company’s platform increased by 22% while the company continued to experience strong demand for its premium data centre services. Based on the above-stated factors, we give a “Buy” recommendation on the stock at the current market price of $6.170, down 0.804% on 11 September 2019.

iSignthis Limited

Q2FY19 Deliver Positive EBIT and Cashflow:iSignthis Limited (ASX: ISX) engages in remote identity verification, payment authentication with deposit taking, transactional banking and payment processing capability.

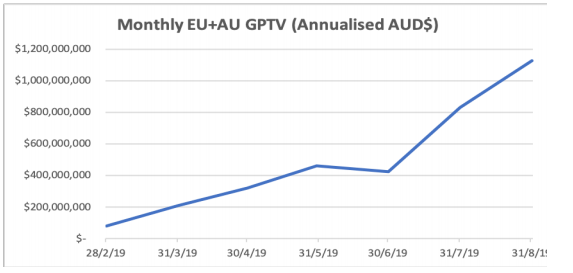

Operational Update: The company recently announced that as at 31 August 2019, its annualised monthly Gross Processed Turnover Volume (GPTV) exceeded A$1.1 billion, increasing 160% from 30 June 2019. Alongside, with new business customers onboarding, the actual processed transactional volumes within the Europe and Australia networks continue to grow in-line with expectations. Business customer approvals at the end of August increased by 28% to 270, as compared to 210 at 30 June 2019.

Annualised GPTV Growth (Source: Company Reports)

1H19 Performance: The company reported total audited operating revenue of A$7.5 million, representing a YoY growth of 49%. Total revenue, including other income, was reported at A$8.2 million, representing a YoY growth of 48%. During the half, statutory loss after tax amounted went down by 75% YoY to A$0.7 million. Cash balance at the end of the period stood at $9.9 million and client funds held at the end of the half were around A$34.0 million.

Guidance: EBIT for the full year ending 31 December 2019 is expected to be $10.7 million.

Stock Recommendation: Over a period of 1 year, the stock generated excellent returns of 867.65%. The share price raced towards its 52-week high level of $1.765 as a result of a 160% increase in GPTV. The company achieved a cash flow positive position in mid-May 2019 and reported both an EBIT and cash flow positive result for the 2QFY19. In August 2019, the company also revised the operating cost base to approximately $11.0 million p.a. annualised, for including additional new product initiatives and to capture further revenue-generating opportunities. Based on the high returns on stock and current trading level, we are of the view that most of the positives are factored in at the current juncture. Hence, we give an “Expensive” recommendation on the stock at the current market price of $1.410, down 14.286% on 11 September 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...