EML Payments Limited

.png)

EML Details

Sales Revenue up 37% in FY19: EML Payments Limited (ASX: EML) offers prepaid payment services in Australia, Europe and North America. It creates instant and secure payment solutions that help customers to connect with each other anytime and anywhere. On 11 December 2019, David Liddy, Director of the company, acquired 160,000 ordinary fully paid shares for a total consideration of $568,000, taking the final holdings to 960,000 ordinary shares.

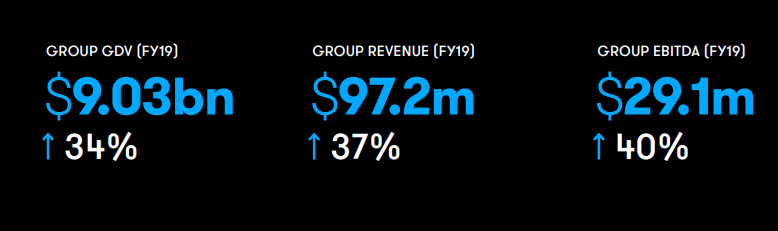

Key Highlights of FY19 for the Period Ended June 30, 2019: The Group’s gross domestic value (GDV) in FY19 came in at $9.03 billion, up 34% year over year. The company reported revenue of $97.2 million, up 37% year over year. EBITDA for the period stood at $29.1 million, up 40% year over year. NPAT for FY19 came in at $8.45 million, representing a substantial increase of 283% year over year.

FY19 Financial Highlights (Source: Company Reports)

Cash flow Highlights: Cash flow from operating activities came in at $29.16 million as compared to $6.37 million in FY18. Cash used in investing activities and cash inflow from financing activities came in at $49.82 million and $15.01 million, respectively, in FY19.

Outlook: The company anticipates revenue, EBITDA and NPATA for FY20 to be in the band of $116 million - $132 million, $38.5 million - $42.5 million and $26.2 million - $29.4 million, respectively.

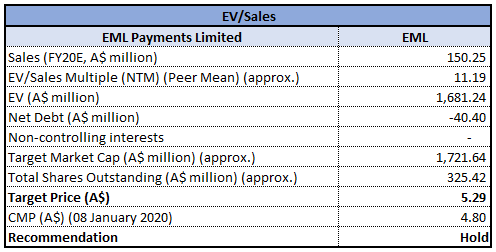

Valuation Methodology:EV/Sales Multiple Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:As per ASX, the stock gained 215.9% in the past one year. As on 08 January 2020, the company’s market capitalisation stands at ~$1.51 billion, with 325.42 million outstanding shares. Its debt to equity ratio for FY19 stood at 0.10x, better than the industry median of 0.56x. Considering the performance in FY19, decent outlook, and financial stability, we have valued the stock using EV/Sales based relative valuation method and for the purpose, have taken the peer group - NEXTDC Ltd (ASX: NXT), Megaport Ltd (ASX: MP1) and Codan Ltd (ASX: CDA). Therefore, we have arrived at a target price with an upside of lower double-digit (in % terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $4.80 per share, up 3.226% as on 08 January 2020.

EML Daily Technical Chart (Source: Thomson Reuters)

NEXTDC Limited

NXT Details

FY19 Revenue Growth at 15%:NEXTDC Limited (ASX: NXT) is a technology company, involved in building, developingand operating independent data centre facilities in Australia.

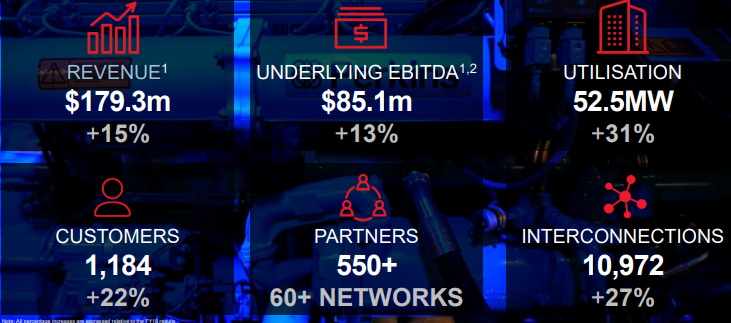

FY19 Highlights for the Period Ended June 30, 2019: The company’s revenue went up by 15% year over year and came in at $179.3 million. Underlying EBITDA increased 13% on a yearly basis and stood at $85.1 million. Underlying capital expenditure stood at $378 million, up from $285 million in FY18. The company’s sale from contracted utilisation reached 52.5MW in FY19, representing an increase of 31% on FY18. Interconnections in FY19 stood at 10,972, up 27% on pcp. The company exited FY19 with cash and cash equivalents of $399 million.

FY19 Key Highlights (Source: Company Reports)

Outlook:For FY20, the company expects revenue, underlying EBITDA and capital expenditure to be in the range of $200 million - $206 million, $100 million - $105 million and $280 million - $300 million, respectively.

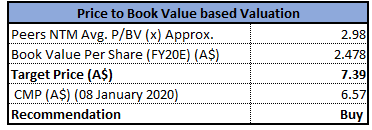

Valuation Methodology:Price to Book Value Multiple Approach

Price to BookBased Valuation (Source: Thomson Reuters)

Note: All the forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

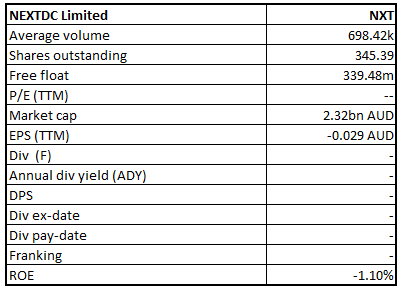

Stock Recommendation: As per ASX, the stock gave a return of 8.2% in the one year.Currently, the stock is trading above the average of its 52-week high and low of $7.250 and $5.71, respectively. As on 08 January 2020, the company’s market capitalisation stands at ~$2.32 billion, with 345.39 million outstanding shares.In FY19, EBITDA margin of the company stood at 52.4%, higher than the industry median of 28.4%. Current ratio of the company was 7.04x as compared to the industry median of 2.81x, which implies a better liquidity position of the company.Considering the above scenario, we have valued the stock using price to book value based relative valuation method and for the purpose, have taken the peer group - EML Payments Ltd (ASX: EML), WiseTech Global Ltd (ASX: WTC), Over the Wire Holdings Ltd (ASX: OTW), etc. Therefore, we have arrived at a target price with an upside of lower double-digit (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $6.570 per share, down 2.377% as on 08 January 2020.

.jpg)

NXT Daily Technical Chart (Source: Thomson Reuters)

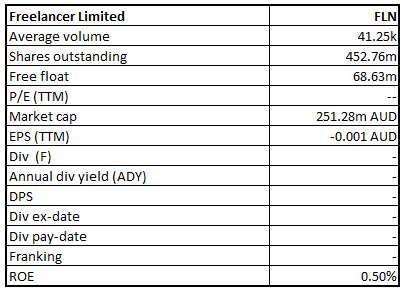

Freelancer Limited

FLN Details

Cash Receipts Soared 9.4% in Third Quarter:Freelancer Limited (ASX: FLN) provides an online outsourcing marketplace and escrow payment services. On 20 December 2019, Simon Clausen, director of the company, acquired 157,866ordinary fully paid shares for a consideration of $0.597 per share.

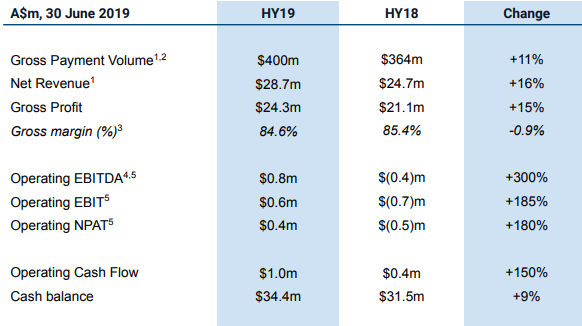

Key Highlights of 3QFY19:In the third quarter ended 30 September 2019, the company reported cash receipts of $14.3 million, an increase of 9.4% year over year. The company reported Freelancer Group Gross Payment Volume (GPV) of $197.8 million, which increased 5.4% year over year. Gross Payment Volume increased 7% to $45.7 million during the quarter. Escrow segment reported a GPV of $152.1 million, up 4.9% year over year. Net operating cash outflow for the quarter came in at $1.5 million. The company exited the quarter with cash and cash equivalents of $33.8 million.

1HFY19 reported a record GPV and net revenue of $400 million and $28.7 million, respectively, representing an increase of 11% and 16% on prior corresponding period.

1HFY19 Highlights (Source: Company Reports)

Stock Recommendation: As on 08 January 2020, the company’s market capitalisation stands at ~$251.28 million, with 452.76 million outstanding shares.Over a period of one month, the stock generated negative returns of 9.76%. For the coming quarter, Escrow remains optimistic about the money transmission licenses to be approved in two more states. Considering the performance in 1HFY19 and 3QFY19, decent growth in cash receipts and Escrow segment outlook, we recommend a “Speculative Buy” rating on the stock at the closing price of $0.555 per share as on 08 January 2020.

FLN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...