.png)

Stocks’ Details

Australia and New Zealand Banking Group Limited

Robust operating profits: Australia and New Zealand Banking Group Limited (ASX: ANZ) has announced via a release that it has completed the sale of its One path Life (New Zealand) Limited to Cigna Corporation. This would be an end of the strategic alliance between the bank and the Cigna Corporation which was announced by the company on 30 May 2018. This sale of the business segment is in consistency with the bank’s strategy to simplify its business and to focus on its core operations.

Also, the company has declared that the shareholders shall be pursued for the approval of the grant of performance rights to the CEO of company, Mr. Shayne Elliott on the terms set out in the meeting itself. The number of performance rights shall be decided with the calculation of dividing the Face Value of tranche by the volume weighted average price of the company’s shares, which was determined to be $25.37. Hence 82774 rights shall be allocated under tranche 1 & 27591 for tranche 2 to Mr Elliott under this plan.

The FY18 operating income rose by 2% to reach at $19.83 Bn. This growth in income was achieved due to a healthy growth in the retail deposits and also the home lending and business lending portfolios. Also, performance looked sound on the back of higher other banking income. The company for the FY 2018, has achieved net cash profit of $6.5 Bn, down by 5% on YoY basis. This fall was witnessed on the back of the fact that there was a degrowth in the Net Interest Income. Consequently, the group’s NIM’s were lower for the FY2018 due to growth in lower margin liquid assets, unfavourable changes in product mix, introduction of major bank levy due to the implementation of recommendations of the royal commission and the impact of customer remediation.

The company has declared fully franked dividend of 160 cps for FY2018.

.png)

ANZ’s key financial metrics (Source: Company Reports)

Meanwhile, the stock price has fallen by 8.47% over the past three months as on December 05, 2018, thus providing an attractive opportunity for the investors. Hence, considering the strong operating profits and recent trading levels, we maintain our “Buy” recommendation on the stock at the current market price of $26.17.

National Storage REIT

Strong growth in AUM:National Storage REIT (ASX: NSR) declared its annual numbers as per which the Assets under management (AUM) have grown by 23% in FY18 to surpass $1.4 billion, cementing the company’s position as the largest storage owner-operator in Australasia. This growth was on account of the organic growth across the portfolio of over 25000 Square meters, via the acquisition of $155 Mn worth new storage centres.

The earnings and distributions have grown during the fiscal with EPS growing by 4.3% to reach at 9.6 cps. Total distributions paid to securityholders over the period from IPO to date has been 39.5 cps. This phenomenal performance is the result of achieving organic growth from the existing assets as well as acquiring EPS accretive assets.

.png)

NSR’s underlying EPS (Source: Company Reports)

On the financial metrics front, the stock has an ROIC of 18.7%, which is commendable when comparing the stock with other REIT players. The company is trading at a Price/cash flow of 14.2x while the Residential & commercial REIT industry trades at 15.2x. The stock price has risen by 11.40% over the past six months as on 4th December 2018. Hence, considering the strong growth in AUM and free cash flow while PE is quite high, we give a “Hold” recommendation on the stock at the current market price of $1.745 as on 5th December 2018.

Downer EDI Limited

Strong EBITDA growth coupled with healthy Order Pipeline:Downer EDI Limited (ASX: DOW) declared via its recent release that Robert Regan has been appointed as the group general council and the company secretary of the company. He will assume the position as from the 1st January 2019. Till that point of time, Peter Lyon will continue his term as the company secretary.

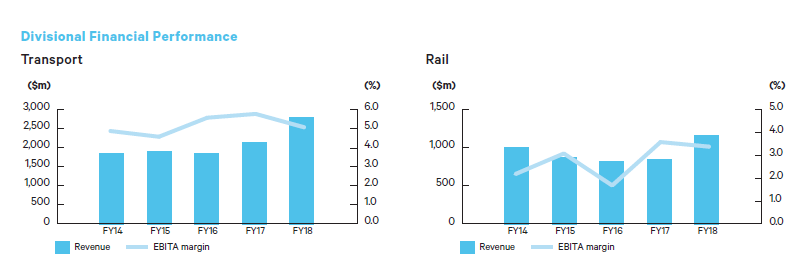

As regards the financial performance for the FY 2018, EBITDA for the year came in at $479.6 Mn, up by 68.2% on YoY basis, and this was achieved on the back of robust EBITDA contribution from the” Spotless” of $167.7 Mn. Also, there was an increase in EBITDA of the transport, utilities and the rail segments.

The firm has released it FY 19 guidance stating that the NPATA is expected to be ~$335 Mn, up by 13% on a YoY basis. This guidance is on the back of substantial amount of opportunity pipelines across the sectors and its market leading position.

DOW’s Segmental performance (Source: Company Reports)

On the financial metrics front, the stock has a dividend yield of 4.23%; however, this is still above the median for the construction and engineering industry. The company is trading at an EV/EBITDA of 6.2x while the construction and engineering industry trades at 6.7x, thus on this parameter the stock seems undervalued. The stock price has fallen by 7.27% over the past six months as on 4th December 2018. Hence, considering the strong growth in EBITDA and undervaluation, we maintain our “Buy” recommendation on the stock at the current market price of $6.29 as on 5th December 2018.

.PNG)

Stock Price Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...