Magellan Global Trust

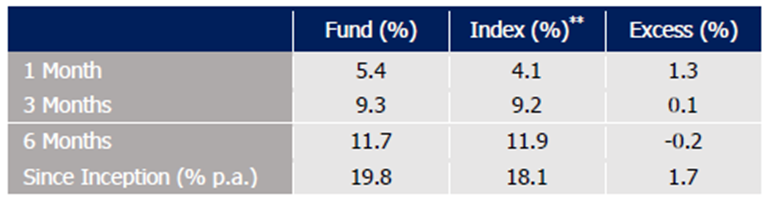

Outperformed the Benchmark in August 2018: Magellan Global Trust (ASX: MGG), a listed investment trust is an actively managed global equities fund comprising of internationally-listed quality growth shares. MGG’s portfolio comprises of stocks of Alphabet (Google), Apple, Facebook, HCA Healthcare, Kraft Heinz etc. They are all mostly blue chip companies. In August 2018, the fund has delivered a 5.4% growth in performance after fees, and has outperformed the MSCI World Net Total Return (AUD) by 1.3%. Since inception in October 2017, MGG’s portfolio has returned 19.8% after fees and has outperformed its benchmark by 1.7%. The fund has largest exposure in Internet & eCommerce sector (18%), followed by Consumer Defensive (17%) and Information Technology, (14%). The fund has also kept a healthy amount of cash on hand to balance the portfolio. At the end of August 2018, 20% of the portfolio was in cash. The fund has invested majorly in US stocks, which comprise 47% of the portfolio. As at 30th June 2018, the Fund had net assets of $1,691 million and a net asset value of $1.6091 per unit. The fund had started trading on 18 October 2017, after raising $1,575 million at $1.50 per unit through an initial public offering. MGG has paid total distributions of 6 cents per unit for the period since inception to 30 June 2018. MGG has delivered net profit of $176.6 million for the period since inception to 30 June 2018. Meanwhile, MGG stock has risen 8.20% in three months as on September 12, 2018 and is trading at a low P/E of 10.19x. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $ 1.735.

Fund Performance (Source: Company Reports)

Rural Funds Group

Decent Performance in FY 18: Rural Funds Group (ASX: RFF), owner of a diversified portfolio of high quality Australian agricultural assets, saw a stock fall of 1.37% on September 13, 2018 while it recently gave the update on RFM Almond Funds. In FY 18, the company experienced good growing conditions throughout the season mostly, but with the exception of rain towards the end of harvest. However, the yield had slightly reduced by lower kernel sizes and the almond price was impacted by large US crop. In FY 19, frost has impacted yield. A pruning program has been planned to reduce the future impact of biennial bearing. The group is identifying cost savings to reduce the effect of the shortfalls driven by low yields. FY18 returns are positive for AF06 and AF08 but AF07 is slightly affected due to quality downgrades. On the other hand, in FY 18, the company has delivered 26% growth in Adjusted funds from operations (AFFO) per unit to 12.7 cents. Earnings grew 29% to $44.0m in 2018. The company expects FY 19 AFFO per unit to increase by 4% to 13.2 cents on FY18 and FY19 forecast distributions per unit is of 10.43 cents, which is up 4% on FY18. Meanwhile, RFF stock has risen 6.72% in three months as on September 12, 2018 and is trading at a reasonable P/E of 15.50x. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 2.160 given its dividend distributions.

WAM Capital

Takeover bid for Wealth Defender Equities Ltd: WAM Capital Limited’s (ASX: WAM) stock rose 0.20% on September 13, 2018 after the company commenced the dispatch of the bidder statement and offer to the shareholders of Wealth Defender Equities Ltd. (WDE), which the company wants to accept soon. WAM’s offer is planned to close on 14 October 2018. WAM has made a conditional off-market takeover bid for WDE of 99¢ per share, which is a 3 per cent premium to the 96.12¢ net tangible asset value, and a 15 per cent premium to the last traded share price of 86.7¢ on 29 August 2018. The takeover offer is one WAM share for every 2.5 Wealth Defender shares. Wealth Defender had underperformed the market since its $125 million listing, and the unit price declined by about 12.6 per cent compared to a 12 per cent gain in the broader share market. If the offer is successful, WAM shareholders will get the benefit from realising all or part of WAM’s 16.27% holding of Wealth Defender shares, which were purchased at a discount to the pre-tax NTA. Further, the all-scrip offer will allow WAM shareholders to get benefit from new shares issued at a premium to the WAM pre-tax NTA. Meanwhile, WAM stock has risen 4.64% in three months as on September 12, 2018 and is trading at a reasonable P/E of 12.85x. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 2.470.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...