.png)

Stocks’ Details

Vocus Group Limited

Period of Strong Cash Conversion and Improved Debt: Vocus Group Limited (ASX: VOC) is a vertically integrated telecommunications service provider, operating in the Australian and New Zealand markets.

Appointment of Company Secretary: The company recently updated that Simon Lewin, currently serving as the Deputy General Counsel, will be appointed as the Company Secretary in place of Ashe-lee Jegathesan.

Director’s Interest: In another recent update, the company notified that Robert Mansfield, one of the directors, acquired 47,000 ordinary shares of the company for a total consideration of $150,262.27.

FY19 Results: Revenue for the year ended 30 June 2019 stood at $1,892.3 million, up 0.4% on prior corresponding period revenue of $1,884.7 million. FY19 revenues were flat due to declines in Retail offsetting the growth across Vocus Networks Services and New Zealand. Underlying EBITDA for the period stood at $360.1 million, down 2% on pcp value of $366.7 million. During the year, the company reported underlying NPAT amounting to $105.5 million, down 17% on pcp NPAT of $127.6 million.

.png)

Financial Summary (Source: Company Reports)

Guidance: In FY20, the company is targeting underlying EBITDA in the range of $359 million - $379 million. Capex for the year is expected to be in the range of $200 million - $210 million. EBITDA growth of $20 million - $30 million in Vocus Network Services, is expected to be offset by a similar decline in Retail.

Stock Recommendation: The stock of the company generated a return of 19.10% over a period of 1 month. In FY19, the company hit the guidance provided with financial stability in a year of significant strategic and operational change and NBN. The period was marked by 100% cash conversion, improving debt and net leverage ratio profile. Strong cost reduction in the Retail segment improved the EBITDA margin, despite declining revenue. In FY20, the company is targeting a cash conversion between 90-95% and expects a strong performance in the second half of the year. Considering the above factors, we give a “Hold” recommendation on the stock at the current market price of $3.590, up 4.665% on 17 September 2019.

TPG Telecom Limited

Improvement in EBITDA Margin for the Corporate Segment:TPG Telecom Limited (ASX: TPM) is engaged in the provision of consumer, wholesale and corporate telecommunications services.

Dividend: The company recently announced that it will be paying a dividend of AUD 0.0200 per ordinary share on 19 November 2019.

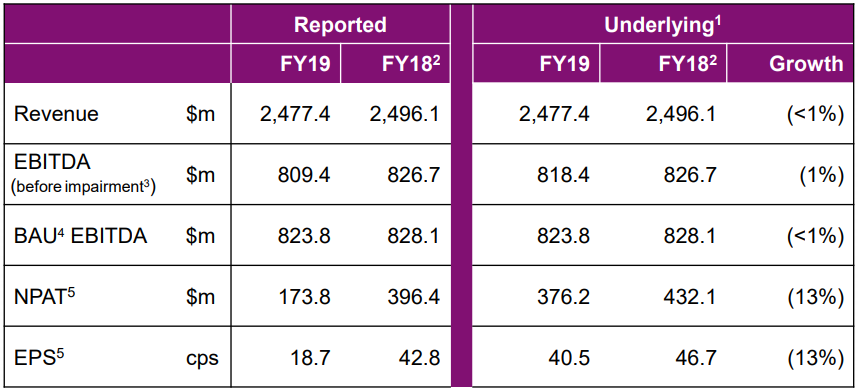

FY19 Results: During the financial year ended 31 July 2019, reported revenue amounted to $2,477.4 million, as compared to $2,496.1 million in FY18. Reported EBITDA for the year stood at $809.4 million, against prior corresponding period value of $826.7 million. Reported NPAT for the year stood at $173.8 million, as compared to $396.4 million in FY18. The company’s corporate segment witnessed an increase of $37.4 million in EBITDA due to contribution from the contract to provide fibre services to VHA. In FY19, EBITDA margin for the segment was 48%, as compared to 44% in FY18.

FY19 Performance (Source: Company Reports)

FY19 results were heavily impacted by the Group’s decision to cease the rollout of its Australian mobile network in January 2019, leading to an impairment expense of $236.8 million along with a significant increase in amortisation and interest expense relating to Australian spectrum licenses. Results for the year were also inclusive of one-off transaction costs of $9.0 million in relation to the planned merger with Vodafone Hutchison Australia.

Guidance: In FY20, the company is expecting to generate Business as Usual (BAU)EBITDA in the range of $735 - $750 million.

Stock Recommendation: The stock of the company generated returns of 6.97% and 6.31% over a period of 1 month and 3 months, respectively. In FY19, the company reported strong net operating cashflows of $836.3 million, exceeding the amount of EBITDA. The company continued to diversify its mobile network in Singapore with additional sites to increase capacity and deepen indoor coverage. In FY19, the company had an EBITDA margin of 33.4% as compared to the industry median of 30.8%. Moving ahead, the company expects to deliver savings on the back of operating cost efficiency programs and is looking forward to another year of growth for the Corporate Division. Based on the aforesaid factors, we give a “Buy” recommendation on the stock at the current market price of $7.070, up 2.315% on 17 September 2019.

Telstra Corporation Limited

Strong Progress on T22 Strategy: Telstra Corporation Limited (ASX: TLS) is engaged in provision of telecommunications and information services to domestic and international customers.

Change in Director’s Interest: The company recently updated that Roy H Chestnutt, one of the directors, acquired 27,000 ordinary shares for a consideration of $97,051.50.

Financial Highlights for FY19: Total Income on a reported basis for FY19 stood at $27.8 billion, down 3.6% on pcp. EBITIDA on reported basis stood at $8.0 billion, down 21.7% on pcp. NPAT on reported basis amounted to $2.1 billion, down 39.6% in comparison to prior corresponding year. During the year, the company added more than 378,000 net retail postpaid handheld mobile services. The company also added over 230,000 wholesale MVNO mobile prepaid and postpaid services & 107,000 net new fixed-line retail bundle and data services.

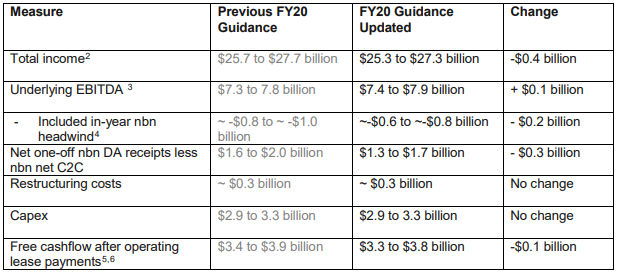

FY20 Guidance: As per NBN Co’s Corporate Plan 2020, the total number of premises forecast to be connected during FY20 went down to 1.5 million, from 2 million earlier. As a result, the guidance for total income was revised to a range of $25.3 - $27.3 million, as compared to the earlier range of $25.7 - $27.7 billion. Guidance range for underlying EBITDA was revised from $7.3 - $7.8 billion to $7.4 - $7.9 billion.

Revised Guidance (Source: Company Reports)

Stock Recommendation: Over a period of 6 months, the stock generated returns of 10.39% and has a market capitalisation of $42.46 billion. FY19 was marked by a strong progress on the company’s T22 strategy, with reduction of consumer & small business plans in market from 1800 to 20, commercial launch of 5G service and 7.7 million drop in calls to call centres. The company’s gross margin in FY19 stood at 63.8%, as compared to the industry median of 56.7%. In FY20, the company expects underlying EBITDA excluding in-year nbn headwind to grow by up to $500 million. Given the backdrop of the above factors, we give a “Hold” recommendation on the stock at the current market price of $3.570, with no change reported on previous trading price.

Daily Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...